How do I manage cash flow in the early stages of a business?

Complete cash flow guide • Financial planning

Cash Flow Management:

Show Cash Flow CalculatorCash flow management is critical for early-stage businesses as it ensures sufficient liquidity to meet operational expenses, pay employees, and handle unexpected costs. Proper cash flow management helps avoid the common pitfall of profitable businesses failing due to insufficient cash on hand.

Effective cash flow management involves forecasting incoming and outgoing funds, monitoring payment terms, optimizing receivables and payables, and maintaining adequate reserves. This practice is essential for business sustainability and growth.

Key cash flow elements:

- Inflows: Revenue, loans, investments, grants

- Outflows: Operating expenses, payroll, taxes, inventory

- Timing: When money enters and exits the business

- Forecasting: Predicting future cash needs

Modern businesses use cash flow management tools and software to track and optimize their financial position, ensuring they can meet obligations while pursuing growth opportunities.

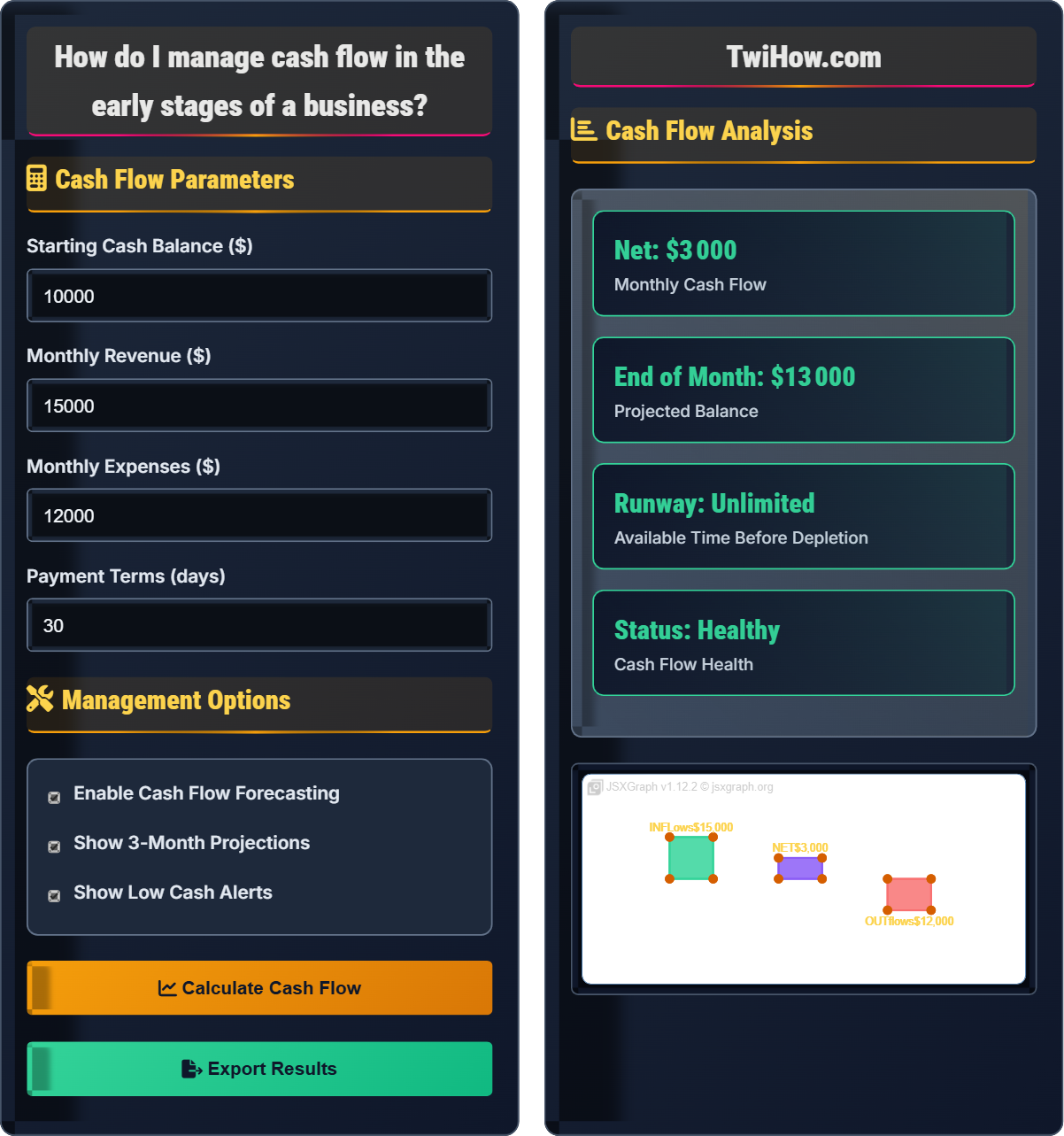

Cash Flow Parameters

Management Options

Cash Flow Analysis

| Category | Amount | Percentage | Status |

|---|---|---|---|

| Revenue | $15,000 | 100% | Positive |

| Expenses | $12,000 | 80% | Controlled |

| Net Flow | $3,000 | 20% | Surplus |

| Reserve | $2,000 | 13% | Adequate |

$15,000

$12,000

$3,000

Cash Flow Management in Early-Stage Businesses

Cash flow management is the process of monitoring, analyzing, and optimizing the amount of cash that enters and leaves a business. It involves tracking cash inflows (revenue, loans, investments) and outflows (expenses, payroll, taxes) to ensure sufficient liquidity for operations.

The fundamental cash flow equation for early-stage businesses:

Where:

- Beginning Cash: Cash available at the start of the period

- Cash Inflows: Money coming into the business (sales, loans, investments)

- Cash Outflows: Money leaving the business (expenses, payments, taxes)

Early-stage cash flow management in action:

- Subscription Model: Monthly recurring revenue provides predictable cash flow

- Seasonal Business: Planning cash reserves during peak seasons for off-season operations

- Project-Based: Managing cash flow between project payments and expenses

- Retail: Balancing inventory purchases with sales receipts

- Accelerate Collections: Offer discounts for early payments

- Delay Payments: Negotiate favorable payment terms with suppliers

- Forecast Accurately: Use historical data and market trends

- Monitor Burn Rate: Track monthly cash consumption

- Build Safety Net: Maintain 3-6 months of operating expenses

Cash Flow Fundamentals

Cash flow, liquidity, burn rate, runway, working capital, accounts receivable, accounts payable.

Ending Cash = Beginning Cash + Inflows - Outflows

Where Ending Cash = available funds, Beginning Cash = starting balance, Inflows = money received, Outflows = money spent.

- Always track cash separately from profit

- Plan for seasonal fluctuations

- Build reserves before you need them

Applications

Startups, small businesses, freelancers, contractors, online businesses.

- Track all cash movements

- Create monthly forecasts

- Optimize payment terms

- Build cash reserves

- Monitor key metrics

- Industry-specific timing patterns

- Seasonal business variations

- Growth investment needs

- Emergency fund requirements

Cash Flow Learning Quiz

What is the primary difference between cash flow and profit in early-stage businesses?

The correct answer is C) Cash flow considers timing of cash movements, profit doesn't. Cash flow tracks when money actually comes in and goes out, while profit is calculated based on accounting principles that may recognize revenue and expenses at different times than when cash exchanges hands. This is critical for early-stage businesses because you can be profitable on paper but run out of cash to pay bills.

For example, a business might sell $10,000 worth of products but not receive payment for 30 days, creating a cash flow gap even though the sale appears as revenue.

Understanding the difference between cash flow and profit is fundamental to business success. Profit is an accounting measure that shows the difference between revenues and expenses over a period. Cash flow shows the actual movement of money in and out of the business. A business can be profitable but still fail if it runs out of cash to pay its obligations. This distinction is particularly important for early-stage businesses that often have irregular cash flows.

Cash Flow: Actual money moving in and out of business

Profit: Revenue minus expenses (accounting measure)

Accrual Accounting: Recording transactions when they occur

• Track cash separately from profit

• Pay attention to timing differences

• Plan for cash flow gaps

• Use cash basis accounting initially

• Monitor accounts receivable aging

• Negotiate favorable payment terms

• Confusing profit with cash flow

• Ignoring payment timing

• Not planning for cash gaps

Explain the importance of cash flow forecasting for early-stage businesses and describe the key components of an effective forecast.

Importance of Cash Flow Forecasting: Cash flow forecasting is critical for early-stage businesses because it helps predict when the business will run out of cash, allowing for proactive measures. It helps with:

- Planning for seasonal variations in cash flow

- Determining when to seek additional funding

- Identifying potential cash shortfalls before they occur

- Optimizing working capital management

Key Components of an Effective Forecast:

Revenue Projections: Based on sales history, market research, and growth assumptions.

Expense Predictions: Fixed costs (rent, salaries) and variable costs (materials, utilities).

Payment Timing: When customers will pay and when suppliers need to be paid.

One-Time Events: Equipment purchases, loan payments, tax obligations.

Effective forecasts typically cover 3-12 months and are updated monthly.

Cash flow forecasting is like looking ahead with a financial crystal ball. It allows businesses to anticipate cash needs and make informed decisions. For early-stage businesses, this is particularly important because they often have limited cash reserves and less predictable revenue streams. Regular forecasting helps identify potential problems before they become crises and allows for strategic planning of growth investments.

Cash Flow Forecast: Prediction of future cash movements

Working Capital: Current assets minus current liabilities

Runway: Time before cash runs out at current burn rate• Update forecasts monthly

• Plan for 3-12 months

• Include worst-case scenarios

• Use historical data as baseline

• Consider seasonality factors

• Include buffer for unexpected events

• Being overly optimistic

• Not updating regularly

• Ignoring seasonality

You run a consulting business where clients pay 30 days after receiving invoices. Your monthly expenses total $8,000, and you bill $12,000 per month. Currently, you have $5,000 in the bank. You just landed a big contract worth $30,000 that starts next month but won't be paid until the following month. How would you manage your cash flow to ensure you can continue operating while waiting for the payment?

Current Month: $5,000 starting balance + $12,000 (previous month's invoice) - $8,000 expenses = $9,000 ending balance

Next Month: $9,000 starting balance + $12,000 (current month's invoice) - $8,000 expenses = $13,000 ending balance

Following Month: $13,000 starting balance + $42,000 ($12,000 regular + $30,000 big contract) - $8,000 expenses = $47,000 ending balance

Management Strategy: The business can operate normally since it will have sufficient cash throughout. However, to be more conservative:

1) Negotiate partial payment upfront for the big contract

2) Consider a small line of credit for emergencies

3) Monitor accounts receivable closely

4) Accelerate collections on the big contract if possible

This scenario demonstrates the importance of cash flow timing. Even though the business is profitable, the timing mismatch between billing and payment can create temporary cash shortages. The key is to plan ahead and ensure that cash is available when expenses are due, regardless of when revenue is recognized. This example shows why cash flow forecasting is essential for businesses with payment delays.

Accounts Receivable: Money owed by customers

Payment Terms: Agreed time frame for payments

Cash Gap: Period between expense and receipt

• Always plan for payment delays

• Maintain safety reserves

• Negotiate favorable terms

• Offer early payment discounts

• Use factoring for large invoices

• Monitor aging reports

• Not accounting for payment delays

• Ignoring seasonal variations

• Underestimating expenses

Your e-commerce business has steady sales of $20,000 per month but struggles with cash flow because customers pay 60 days after purchase. Meanwhile, you must pay suppliers within 30 days. Your monthly expenses are $15,000. What strategies would you implement to improve your cash flow position?

Immediate Actions:

1) Negotiate Payment Terms: Try to extend supplier payment terms to 45-60 days to match customer payment cycles.

2) Offer Early Payment Discounts: Provide incentives for customers to pay within 15 days (e.g., 2% discount).

3) Require Deposits: Ask for 50% deposits on larger orders to improve cash flow timing.

Medium-term Strategies:

4) Invoice Financing: Sell outstanding invoices to a factoring company for immediate cash.

5) Line of Credit: Establish a revolving credit facility to bridge cash flow gaps.

6) Inventory Optimization: Reduce inventory levels to free up cash.

These strategies would help align your cash inflows and outflows, reducing the timing gap that creates cash flow stress.

This scenario illustrates the classic cash conversion cycle challenge where businesses must pay suppliers before receiving payment from customers. The solution involves managing both sides of the equation: accelerating inflows and optimizing outflows. The key is to find the right balance that maintains good relationships with both customers and suppliers while improving cash position. This often requires creative financing solutions and careful negotiation.

Cash Conversion Cycle: Time from paying suppliers to receiving customer payment

Factoring: Selling receivables for immediate cash

Working Capital: Short-term assets minus short-term liabilities

• Align payment cycles when possible

• Maintain good vendor relationships

• Consider financing options

• Automate invoicing and reminders

• Use digital payment methods

• Monitor DSO (Days Sales Outstanding)

• Ignoring payment timing differences

• Not negotiating terms

• Over-investing in inventory

Which of the following is the most critical cash flow metric for an early-stage business?

The correct answer is B) Monthly burn rate. The burn rate tells you exactly how much cash the business is spending each month, which is critical for determining how long the business can operate before needing additional funding or becoming cash flow positive. While other metrics are important, burn rate directly impacts survival in the early stages.

Burn rate = Total monthly expenses - Monthly cash inflows (or negative net cash flow if inflows exceed outflows).

For early-stage businesses, survival is the primary concern, making burn rate the most critical metric. It directly answers the question: "How long can we continue operating?" This metric drives all other strategic decisions, from hiring to marketing spend. Once a business understands its burn rate, it can calculate its runway (cash reserves divided by burn rate) and plan accordingly. Other metrics become more important as the business matures and stabilizes.

Burn Rate: Monthly cash consumption rate

Runway: Months of operation remaining

Liquidity: Ability to meet short-term obligations

• Monitor burn rate daily

• Plan for 6+ months runway

• Control expenses carefully

• Track burn rate weekly

• Set alerts for threshold levels

• Plan fundraising before running low

• Not tracking burn rate

• Underestimating expenses

• Delaying fundraising efforts

FAQ

Q: How much cash reserve should I maintain for my early-stage business?

A: For early-stage businesses, I recommend maintaining 3-6 months of operating expenses as cash reserves. This provides a safety net for unexpected events and seasonal variations. The exact amount depends on your business model: service businesses with predictable revenue might need closer to 3 months, while product businesses with inventory or seasonal sales might need 6+ months. Calculate your monthly burn rate (total expenses) and multiply by your desired runway length. Remember to also factor in growth investments and any upcoming large expenses.

Q: What cash flow metrics do investors focus on when evaluating early-stage companies?

A: As an investor, I focus on several key metrics: 1) Monthly burn rate and runway remaining, 2) Unit economics showing cash flow per customer, 3) Days Sales Outstanding (DSO) for receivables management, 4) Cash conversion cycle efficiency, and 5) Trend of cash flow metrics over time. I want to see management actively monitoring these metrics and taking corrective action when needed. A company that doesn't track cash flow carefully is a red flag. I also look for evidence that management understands the relationship between growth investments and cash flow, and has a clear plan for achieving cash flow positivity.