How Do I Choose Between Different Bank Accounts and Fees?

Complete guide • Step-by-step banking comparisons

Bank Account Selection Fundamentals:

Show Fee ComparisonChoosing the right bank account involves comparing features, fees, and services to match your financial needs. Key considerations include monthly maintenance fees, minimum balance requirements, ATM fees, overdraft policies, interest rates, and accessibility. The goal is to minimize costs while maximizing benefits.

Account types and features:

- Checking Accounts: Daily transactions, bill payments, debit cards

- Savings Accounts: Interest earnings, limited withdrawals, emergency funds

- Money Market Accounts: Higher interest, check-writing privileges

- Certificates of Deposit: Fixed-term deposits with higher interest

Smart banking decisions involve analyzing your spending patterns, transaction frequency, and financial goals to select accounts that align with your lifestyle while minimizing unnecessary fees.

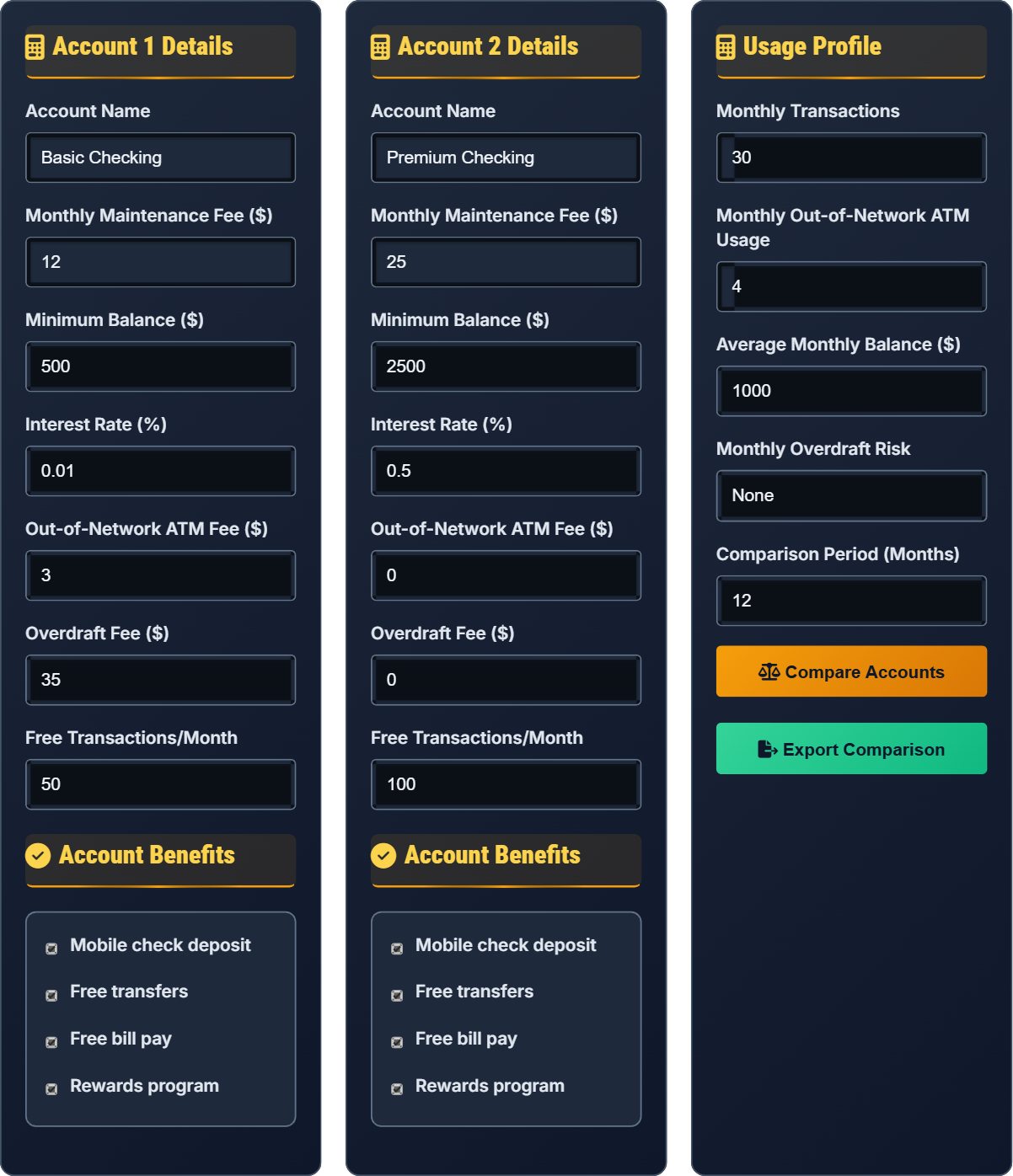

Account 1 Details

Account Benefits

Account 2 Details

Account Benefits

Usage Profile

Account Comparison Results

| Feature | Basic Checking | Premium Checking | Winner |

|---|---|---|---|

| Monthly Fee | $12 | $25 | Basic |

| Minimum Balance | $500 | $2,500 | Basic |

| Interest Rate | 0.01% | 0.50% | Premium |

| ATM Fees | $3 | $0 | Premium |

| Overdraft Fees | $35 | $0 | Premium |

Fee Breakdown for 12 Months

- Basic Checking: $144 total ($12/mo fee + $48 ATM fees)

- Premium Checking: $300 total ($25/mo fee + $0 ATM fees)

- Interest Earned: $0.60 (Basic) vs $6.00 (Premium)

- Net Cost: $143.40 (Basic) vs $294.00 (Premium)

Analysis & Recommendations

- Basic checking is $156 cheaper annually for your usage pattern

- Only consider premium if you frequently use out-of-network ATMs

- Interest earned doesn't offset higher fees for current balance

- Basic account meets your transaction needs with free tier

Bank Account Selection Explained

Banking fees are charges imposed by financial institutions for various services and account maintenance. Understanding these fees is crucial for selecting accounts that align with your financial habits and minimizing unnecessary costs. Common fees include monthly maintenance fees, ATM fees, overdraft fees, and minimum balance penalties.

Annual cost calculation for bank accounts:

Where:

- Monthly Fee: Recurring charge for account maintenance

- Transaction Fees: Charges for exceeding free transaction limits

- Other Fees: ATM fees, overdraft fees, wire transfer fees

- Interest Earned: Earnings from account balance

Different account types serve different purposes:

- Checking Accounts: For daily transactions, bill payments, and easy access to funds

- Savings Accounts: For storing money safely with modest interest earnings

- Money Market Accounts: Higher interest rates with limited transaction capabilities

- Certificates of Deposit: Fixed-term deposits with higher interest rates for locked funds

- Meet Minimum Balance Requirements: Avoid monthly fees by maintaining required balances

- Use In-Network ATMs: Prevent ATM fees by using your bank's network

- Opt-Out of Overdraft Protection: Decline transactions instead of incurring fees

- Consolidate Accounts: Manage fewer accounts to reduce fees

- Negotiate with Banks: Ask for fee waivers based on loyalty or relationship

Banking Fundamentals

Banking fees, account types, minimum balances, interest rates, transaction limits.

Annual cost = (Monthly fee × 12) + Additional fees - Interest earned

Where fees are based on actual usage patterns and account requirements.

- Always read the fine print for hidden fees

- Consider your actual usage patterns

- Factor in opportunity cost of minimum balances

Real-World Examples

Student accounts, business accounts, high-net-worth accounts, international banking.

- Estimate annual usage patterns

- List all potential fees for each account

- Calculate total annual costs

- Compare benefits and features

- Factor in interest earnings

- Track spending for 3 months before switching

- Consider online banks for lower fees

- Look for accounts with easy fee waivers

- Review accounts annually

Bank Account Selection Quiz

Which of the following is typically the easiest way to waive monthly maintenance fees on checking accounts?

Most banks offer monthly maintenance fee waivers if you maintain a minimum average daily balance in your account. This is typically the most common and straightforward way to avoid monthly fees. The minimum balance required varies by institution, commonly ranging from $500 to $2,500.

The answer is B) Maintain a minimum average daily balance.

Understanding fee waiver requirements is crucial for minimizing banking costs. Banks profit from fees when customers don't meet requirements, so knowing how to qualify for waivers can save hundreds of dollars annually. Other common fee waivers include having direct deposit, making a certain number of debit card transactions, or maintaining combined balances across multiple accounts.

Minimum Balance: Lowest average balance required to avoid fees

Fee Waiver: Condition that eliminates recurring account fees

Average Daily Balance: Average of daily balances over a statement period

• Read fee schedules carefully

• Track balance requirements

• Understand calculation methods

• Set up balance alerts to avoid falling below minimums

• Consider multiple fee waiver options

• Negotiate with banks for waivers

• Not understanding how average balance is calculated

• Forgetting about quarterly or annual fees

• Missing fee waiver opportunities

If you have a checking account with a $15 monthly fee, $2.50 out-of-network ATM fees, and you use out-of-network ATMs 8 times per month, what is your total annual cost? Assume no fee waivers apply.

Monthly Calculation:

• Monthly maintenance fee: $15

• ATM fees: 8 × $2.50 = $20

• Total monthly cost: $15 + $20 = $35

Annual Calculation:

• Total annual cost: $35 × 12 = $420

This example demonstrates how seemingly small fees can accumulate significantly over time.

Annual cost calculation reveals the true expense of banking relationships. Small monthly fees and transaction charges compound over time, often totaling more than expected. This emphasizes the importance of comparing accounts based on your actual usage patterns rather than just advertised features. The compounding effect of fees can easily exceed hundreds of dollars annually.

Compounding Effect: Accumulation of fees over time

Annual Percentage Rate (APR): Total cost expressed annuallyOpportunity Cost: Value of money lost to fees

• Always calculate annual costs

• Factor in all potential fees

• Consider your actual usage patterns

• Use online calculators for fee projections

• Track your actual usage for accuracy

• Consider online banks with lower fees

• Only considering monthly fees

• Underestimating transaction costs

• Not projecting annual totals

Jane is comparing two checking accounts: Account A has a $12 monthly fee but no minimum balance requirement, while Account B has no monthly fee but requires a $2,000 minimum balance. Jane typically maintains $1,500 in her account. She uses out-of-network ATMs twice per month. Which account would be more cost-effective for her over a year?

Account A Analysis:

• Monthly fee: $12 × 12 = $144

• ATM fees: 2/month × $3 × 12 = $72

• Total annual cost: $144 + $72 = $216

Account B Analysis:

• Monthly fee: $0

• Minimum balance: Jane falls short by $500, so she'd incur fees (assuming $25/month penalty)

• Penalty fees: $25 × 12 = $300

• ATM fees: 2/month × $3 × 12 = $72

• Total annual cost: $0 + $300 + $72 = $372

Conclusion: Account A is more cost-effective at $216 vs $372 for Account B.

This example demonstrates why matching account features to personal financial habits is crucial. While Account B appears attractive with no monthly fee, Jane's inability to meet the minimum balance requirement makes it significantly more expensive. The lesson is to evaluate accounts based on your actual financial situation, not just advertised features. Hidden penalties can make "free" accounts more costly than paid alternatives.

Minimum Balance Requirement: Average balance needed to avoid fees

Penalty Fees: Charges for not meeting account requirements

Personal Financial Alignment: Matching products to individual needs

• Match account features to your habits

• Consider all potential fees

• Evaluate based on actual usage

• Track your balance for 3 months before choosing

• Consider your ATM usage patterns

• Look for accounts that match your behavior

• Choosing accounts based on advertising alone

• Not considering minimum balance requirements

• Ignoring penalty fees

Mark is deciding between a traditional brick-and-mortar bank and an online bank. The traditional bank offers local branch access but charges $15/month and $3 out-of-network ATM fees. The online bank has no monthly fees but charges $2.50 for out-of-network ATM fees. Mark uses ATMs 10 times per month. What are the pros and cons of each option, and which is better financially?

Traditional Bank:

• Monthly fees: $15 × 12 = $180

• ATM fees: 10/month × $3 × 12 = $360

• Total annual cost: $540

Online Bank:

• Monthly fees: $0

• ATM fees: 10/month × $2.50 × 12 = $300

• Total annual cost: $300

Pros/Cons: Online bank is $240 cheaper annually, but Mark loses physical branch access. Online banks typically offer higher interest rates and lower fees due to reduced overhead costs.

This comparison highlights the trade-offs between convenience and cost. Online banks can offer significant savings due to lower operational costs, but may not suit everyone's preferences. The key is evaluating whether the cost savings justify the change in banking experience. Many consumers find the digital-first approach convenient and cost-effective, especially with expanded ATM networks.

Operational Efficiency: Cost savings from reduced physical infrastructure

Trade-off Analysis: Balancing cost savings against convenience factors

Digital Banking: Online and mobile-first banking services

• Consider both cost and convenience

• Evaluate ATM network coverage

• Assess customer service options

• Look for online banks with reimbursement programs

• Check if employer offers banking partnerships

• Consider hybrid approaches

• Ignoring convenience factors

• Not considering ATM network access

• Overlooking customer service quality

When comparing bank accounts, how should interest rates factor into your decision?

Interest rates should be evaluated after accounting for fees and features. While higher interest is beneficial, it rarely offsets high fees. For example, earning 1% interest on a $1,000 balance yields $10 annually, which doesn't compensate for $200 in fees. The priority should be minimizing fees and finding suitable features, then optimizing interest earnings.

The answer is C) Factor in interest after evaluating fees and features.

Interest rates are often overemphasized in banking decisions. The reality is that checking account interest rates are typically very low (often 0.01%), making fees the dominant cost factor. Higher interest rates usually come with higher minimum balance requirements or fees. The strategic approach is to minimize costs first, then optimize for earnings within that constraint.

Opportunity Cost: Value of money lost to fees vs potential earnings

Fee Priority Principle: Minimize costs before maximizing earnings

Interest Rate Reality: Typically minimal impact on checking accounts

• Prioritize fee minimization

• Consider interest as secondary factor

• Look at net cost after interest

• Use separate high-yield savings for earnings

• Focus on checking account features

• Consider CDs for higher interest

• Chasing high interest in checking accounts

• Ignoring the impact of fees

• Not separating checking and savings strategies

FAQ

Q: As a student, what type of checking account should I choose?

A: For students:

1. Student Checking Accounts: Look for accounts specifically designed for students with no minimum balance requirements

2. Low or No Monthly Fees: Many banks offer fee waivers for students with proof of enrollment

3. ATM Network Access: Choose a bank with ATMs near campus to avoid fees

4. Mobile Banking Features: Essential for managing finances on-the-go

5. Direct Deposit: For financial aid refunds, part-time job paychecks

6. Overdraft Protection: Consider opting out to avoid fees, or choose accounts with low overdraft fees

Focus on convenience and low fees rather than interest rates since balances are typically low.

Q: How do I avoid overdraft fees?

A: To avoid overdraft fees:

1. Opt-Out of Overdraft Protection: Choose to decline transactions that exceed your balance

2. Link to Savings Account: Some banks offer free overdraft protection by linking to savings

3. Use Alerts: Set up low balance notifications to stay aware of your balance

4. Keep Buffer Amount: Maintain $100-200 above zero to prevent accidental overdrafts

5. Track Spending: Use banking apps to monitor transactions in real-time

6. Choose Accounts with No Overdraft Fees: Some banks and credit unions offer accounts with no overdraft fees

7. Budget Carefully: Plan expenses to ensure sufficient funds are available

Remember that overdraft fees can be substantial ($35+ per occurrence), making prevention crucial.

Q: What features should I look for in a business checking account?

A: For business checking accounts:

• Transaction Limits: Higher number of free transactions per month

• Online Banking: Robust digital tools for managing business finances

• Integration Capabilities: Compatibility with accounting software (QuickBooks, etc.)

• Deposit Services: Mobile check deposit and remote deposit capture

• Debit Cards: Business debit cards for employees

• ACH Processing: Automated clearing house for recurring payments

• Customer Service: Dedicated business banking support

• Fee Structure: Volume discounts for higher transaction counts

Consider credit unions for competitive business banking with lower fees than traditional banks.

Separate business and personal accounts for legal and tax purposes.