How Do I Evaluate Financial Advice and Avoid Bad Recommendations?

Complete guide • Step-by-step evaluation strategies

Financial Advice Evaluation Fundamentals:

Show Advisor CheckerEvaluating financial advice is crucial for making informed decisions that align with your financial goals. Quality financial advice should be based on your individual circumstances, risk tolerance, and objectives. Good advisors will provide clear explanations, disclose conflicts of interest, and offer evidence-based recommendations.

Red flags to watch for:

- Guaranteed Returns: No investment is without risk

- High-Pressure Sales: Legitimate advice doesn't require immediate decisions

- Unrealistic Promises: Claims of extraordinary returns

- Lack of Credentials: Unverified licenses or certifications

- Conflict of Interest: Not disclosing how they're compensated

Always verify credentials, understand fee structures, and seek multiple opinions before making significant financial decisions.

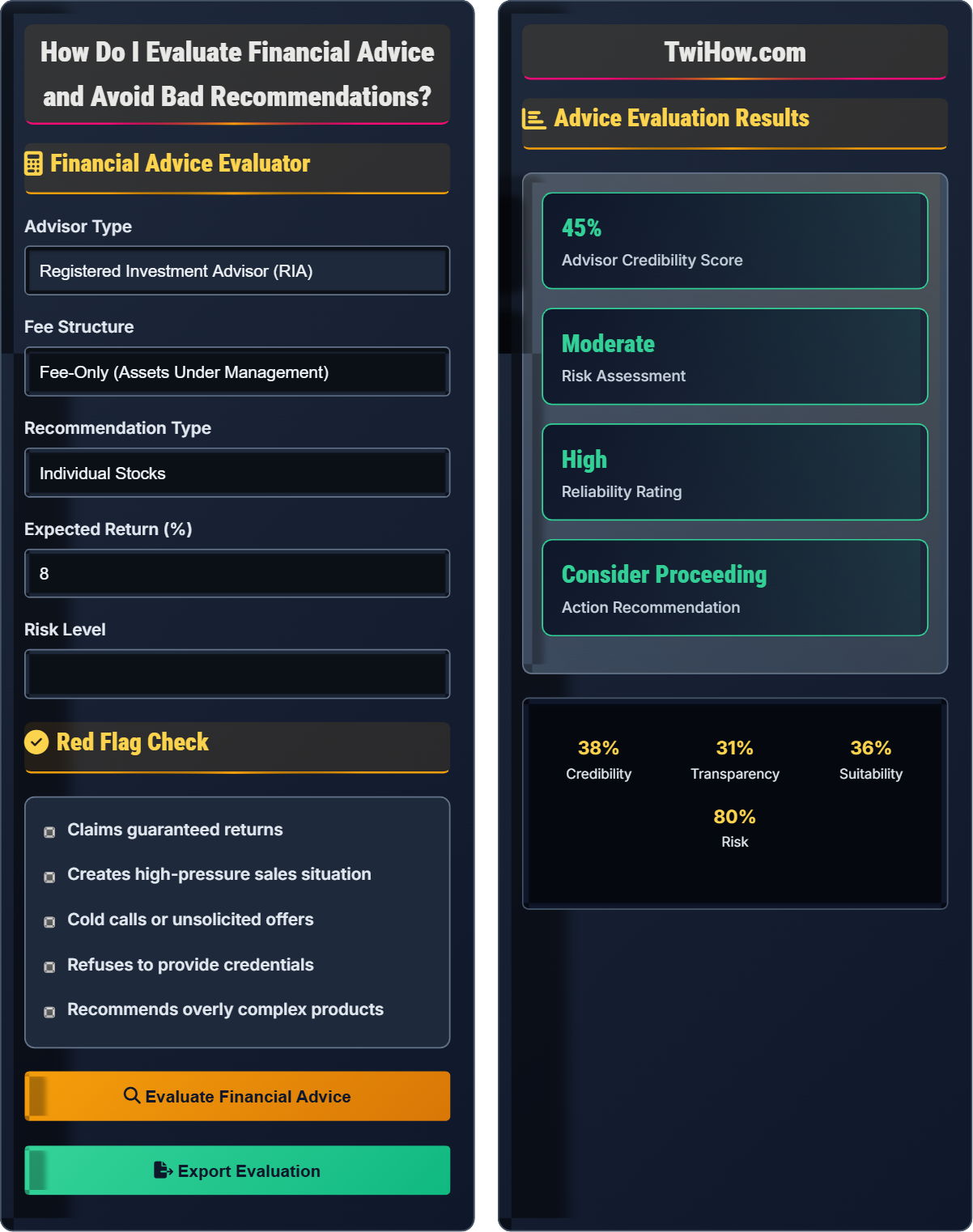

Financial Advice Evaluator

Red Flag Check

Advice Evaluation Results

| Factor | Score | Weight | Impact |

|---|---|---|---|

| Advisor Credentials | Good | 25% | High |

| Fee Transparency | Good | 20% | High |

| Product Suitability | Acceptable | 25% | High |

| Return Expectations | Acceptable | 15% | Moderate |

| Red Flag Indicators | Low | 15% | High |

Verification Checklist

- Check FINRA BrokerCheck: Verify advisor's license and disciplinary history

- Verify Firm Registration: Confirm firm is registered with appropriate regulators

- Check Background: Look for criminal or regulatory violations

- Read Client Reviews: Look for consistent patterns in feedback

- Verify Insurance: Ensure advisor carries professional liability insurance

Action Plan

- Research First: Verify credentials and background

- Ask Questions: Request detailed explanations

- Get It In Writing: All recommendations should be documented

- Seek Second Opinion: Consult another advisor if unsure

- Take Your Time: Don't rush into decisions

Financial Advice Evaluation Explained

Financial advice evaluation is the process of critically assessing the quality, credibility, and appropriateness of financial recommendations before making decisions. This involves examining the advisor's credentials, understanding fee structures, verifying claims, and ensuring recommendations align with your personal financial situation and goals.

Comprehensive evaluation includes multiple factors:

Where factors include:

- Credentials: Licenses, certifications, and professional standing

- Experience: Years in industry and relevant expertise

- Transparency: Clear disclosure of fees and conflicts

- Track Record: Historical performance and client satisfaction

- Suitability: Alignment with your financial goals and risk tolerance

Essential criteria for evaluating financial advice:

- Credentials: Proper licensing and certifications (CFP, CFA, etc.)

- Transparency: Clear disclosure of fees, conflicts, and methodologies

- Objectivity: Recommendations based on your needs, not product sales

- Experience: Proven track record in relevant areas

- Communication: Ability to explain complex concepts clearly

- Guaranteed Returns: No investment is without risk

- Pressure Tactics: Creating urgency to make quick decisions

- Complex Products: Recommending unnecessarily complicated solutions

- Unrealistic Claims: Promising extraordinarily high returns

- Lack of Disclosure: Not revealing how they're compensated

Evaluation Fundamentals

Financial advice evaluation, advisor credentials, fiduciary duty, conflict of interest, due diligence.

Quality = Σ(Factor score × Weight)

Where factors include credentials, transparency, suitability, and objectivity.

- Always verify credentials independently

- Understand how your advisor is compensated

- Be wary of guaranteed return promises

Real-World Examples

Investment scams, insurance fraud, pension scams, cryptocurrency promotions.

- Research advisor background and credentials

- Verify firm registration with regulators

- Check for disciplinary actions or complaints

- Understand the compensation structure

- Validate the investment opportunity

- Take time to make decisions

- Get everything in writing

- Seek second opinions

- Verify information independently

Financial Advice Evaluation Quiz

Which of the following credentials indicates that an advisor is held to a fiduciary standard?

A Certified Financial Planner (CFP) is held to a fiduciary standard, meaning they must act in their clients' best interests. The CFP Board requires its certificants to act as fiduciaries when providing financial planning services. Other credentials like Series 7 or insurance licenses may not require fiduciary duties.

The answer is B) Certified Financial Planner (CFP).

Understanding the difference between fiduciary and suitability standards is crucial. Fiduciary advisors must put clients' interests first, while suitability standard advisors only need to recommend investments that are suitable for the client. This fundamental difference affects the quality and objectivity of advice received. Always ask if your advisor acts as a fiduciary.

Fiduciary Standard: Obligation to act in client's best interest

Suitability Standard: Recommend investments suitable for client

Certified Financial Planner (CFP): Professional with comprehensive certification

• Ask if your advisor is a fiduciary

• Verify credentials independently

• Understand the standard of care

• Look for CFP, CFA, or RIA designations

• Check for fiduciary oaths

• Verify through professional boards

• Assuming all advisors are fiduciaries

• Not verifying credentials

• Confusing licenses with standards

Which fee structure creates the most potential for conflicts of interest?

Commission-based fee structures create the most potential for conflicts of interest because advisors earn more by selling more products. This creates an incentive to recommend products that generate higher commissions rather than those that are best for the client. Fee-only advisors (charging a percentage of assets under management) align their interests with clients' success.

Commission-based advisors may recommend more expensive products with higher fees or push products they can sell quickly rather than those that suit your long-term needs.

Understanding how advisors are compensated is crucial for evaluating their recommendations. When advisors earn commissions, they have an incentive to sell products that pay them more, regardless of whether those products are best for you. Fee-only advisors are paid based on the assets they manage, creating an incentive to grow your portfolio. Fee-based advisors combine both, which can create mixed incentives.

Fee-Only: Paid only by client fees, no commissions

Commission-Based: Paid by product sales commissions

Fee-Based: Combination of fees and commissions

• Understand how your advisor is paid

• Ask about all potential conflicts

• Consider fee structures when evaluating advice

• Prefer fee-only advisors when possible

• Ask for complete fee disclosure

• Understand all costs involved

• Not asking about fee structures

• Assuming all advisors have same incentives

• Overlooking hidden fees

You receive a call from someone claiming to be a financial advisor who says they've identified an investment opportunity with guaranteed 15% annual returns and no risk. They want you to wire money immediately because the opportunity is only available for 24 hours. What should you do?

Do not proceed! This is a classic scam with multiple red flags:

• "Guaranteed" returns: No investment is without risk

• No risk claim: Higher returns require accepting higher risk

• Immediate action pressure: Legitimate opportunities don't require instant decisions

• Wire transfer request: Often associated with scams

• Unsolicited contact: Reputable advisors don't cold-call with exclusive deals

Correct action: Hang up immediately, report to authorities, and never give personal financial information to unsolicited callers.

This scenario demonstrates multiple classic red flags that indicate fraudulent activity. Legitimate financial advisors don't make unsolicited calls with guaranteed return offers. The pressure for immediate action is designed to prevent you from researching the opportunity or seeking advice from trusted sources. Understanding these patterns helps protect against financial scams.

Red Flags: Warning signs indicating potential fraud

Pressure Tactics: Creating artificial urgency to make quick decisions

Guaranteed Returns: False promise of profits without risk

• Never wire money to strangers

• No investment is without risk

• Legitimate opportunities don't expire in 24 hours

• Verify caller's identity independently

• Research the company separately

• Report suspicious calls to authorities

• Being swayed by pressure tactics

• Not researching before investing

• Sending money to strangers

Your advisor recommends a specific mutual fund that pays them a 5% commission, while a similar fund with the same performance record has no commission. What should you consider when evaluating this recommendation?

Key considerations:

• Conflict of interest: Advisor has financial incentive to recommend the commissioned fund

• Cost comparison: The commissioned fund likely has higher fees that reduce your returns

• Transparency: Did advisor disclose the commission arrangement?

• Alternative options: Why wasn't the no-commission option discussed?

Appropriate response: Ask for a complete explanation of why the commissioned fund is recommended despite higher costs, request disclosure of all compensation, and consider whether the recommendation truly serves your best interests.

This scenario illustrates how compensation structures can create conflicts of interest. Advisors may recommend products that generate higher commissions rather than those that maximize client returns. The 5% commission is likely embedded in the fund's fees, reducing your net returns. Understanding these dynamics helps you evaluate recommendations more critically and ask better questions.

Conflict of Interest: Situation where advisor's interests conflict with client's

Embedded Fees: Costs built into investment products

Net Returns: Returns after all fees and expenses

• Always ask about advisor compensation

• Demand full disclosure

• Request fee-only recommendations

• Compare multiple similar products

• Calculate true cost impact

• Not asking about compensation

• Assuming all advisors have same incentives

• Not calculating true costs

What is the most reliable source for verifying a financial advisor's credentials and disciplinary history?

FINRA's BrokerCheck database is the most reliable source for verifying an advisor's credentials, employment history, and any disciplinary actions. It's maintained by the Financial Industry Regulatory Authority and contains comprehensive, verified information about registered brokers and firms. This database is specifically designed for investor protection and verification.

Other sources may be outdated, incomplete, or self-reported without verification.

The answer is B) FINRA BrokerCheck database.

Verification through official regulatory databases is essential for protecting yourself from unqualified or unethical advisors. FINRA's BrokerCheck provides verified, current information that advisors cannot manipulate. This official source is specifically designed for investor protection and contains comprehensive records of licensing, employment, and any regulatory actions taken against advisors.

FINRA: Financial Industry Regulatory Authority

BrokerCheck: Public database of broker and firm information

Regulatory Database: Official record maintained by regulators

• Use official regulatory databases

• Don't rely on self-reported information

• Verify independently of advisor

• Check multiple verification sources

• Look for disciplinary actions

• Verify current registration status

• Accepting self-reported credentials

• Not verifying through official sources

• Assuming all advisors are registered

FAQ

Q: How do I know if an advisor is really acting in my best interest?

A: Look for these indicators:

1. Fiduciary Duty: They are legally required to act in your best interest

2. Fee Structure: Fee-only advisors align their interests with yours

3. Transparency: They clearly explain all fees and potential conflicts

4. Questions About You: They spend more time understanding your situation than promoting products

5. Education: They explain concepts and help you understand decisions

6. Documentation: All recommendations are put in writing with rationale

Ask directly: "Are you a fiduciary?" and "How are you paid?" Legitimate advisors will be happy to answer.

Q: What's the difference between a financial advisor and a financial planner?

A: The main differences:

Financial Advisor:

• Broader term for anyone giving financial advice

• May focus on specific products or services

• Could be commission-based or fee-based

• May not have comprehensive planning training

Financial Planner:

• More specialized in comprehensive financial planning

• Usually has formal education in financial planning

• Typically certified (like CFP) with ongoing education requirements

• Focuses on holistic approach covering all financial aspects

Not all financial advisors are financial planners, but all financial planners are financial advisors.

Q: How often should I review my financial plan and advisor's performance?

A: Regular reviews are essential:

• Annual Reviews: Comprehensive plan review and goal assessment

• Quarterly Check-ins: Performance monitoring and minor adjustments

• Life Events: Immediately after major changes (marriage, job, health)

• Market Volatility: During significant market movements

• Advisor Performance: Annually assess if they're meeting expectations

During reviews, examine portfolio performance, fee structures, goal progress, and whether the advisor continues to meet your needs. If performance is consistently below benchmarks or communication is poor, consider finding a new advisor.

Also verify that your advisor maintains current licenses and certifications.