How to Improve Credit Score Effectively

Step-by-step guide • Actionable strategies

Credit Score Fundamentals:

Predict Score ImprovementYour credit score is a three-digit number that represents your creditworthiness to lenders. It ranges from 300 to 850, with higher scores indicating better credit health. Improving your credit score requires understanding the five key factors that influence it: payment history (35%), credit utilization (30%), length of credit history (15%), credit mix (10%), and new credit inquiries (10%).

Payment History (35%): Making payments on time is the most important factor.

Credit Utilization (30%): Keep balances below 30% of credit limits, ideally below 10%.

Key improvement strategies:

- Pay Bills on Time: Set up automatic payments or reminders

- Reduce Credit Card Balances: Pay down existing debt

- Don't Close Old Accounts: Maintain credit history length

- Monitor Your Credit Report: Check for errors and dispute inaccuracies

- Limit New Credit Applications: Too many inquiries can hurt your score

Improving your credit score takes time and consistent effort. Most people see noticeable improvements within 3-6 months of implementing positive habits, with significant improvements possible within 12-24 months.

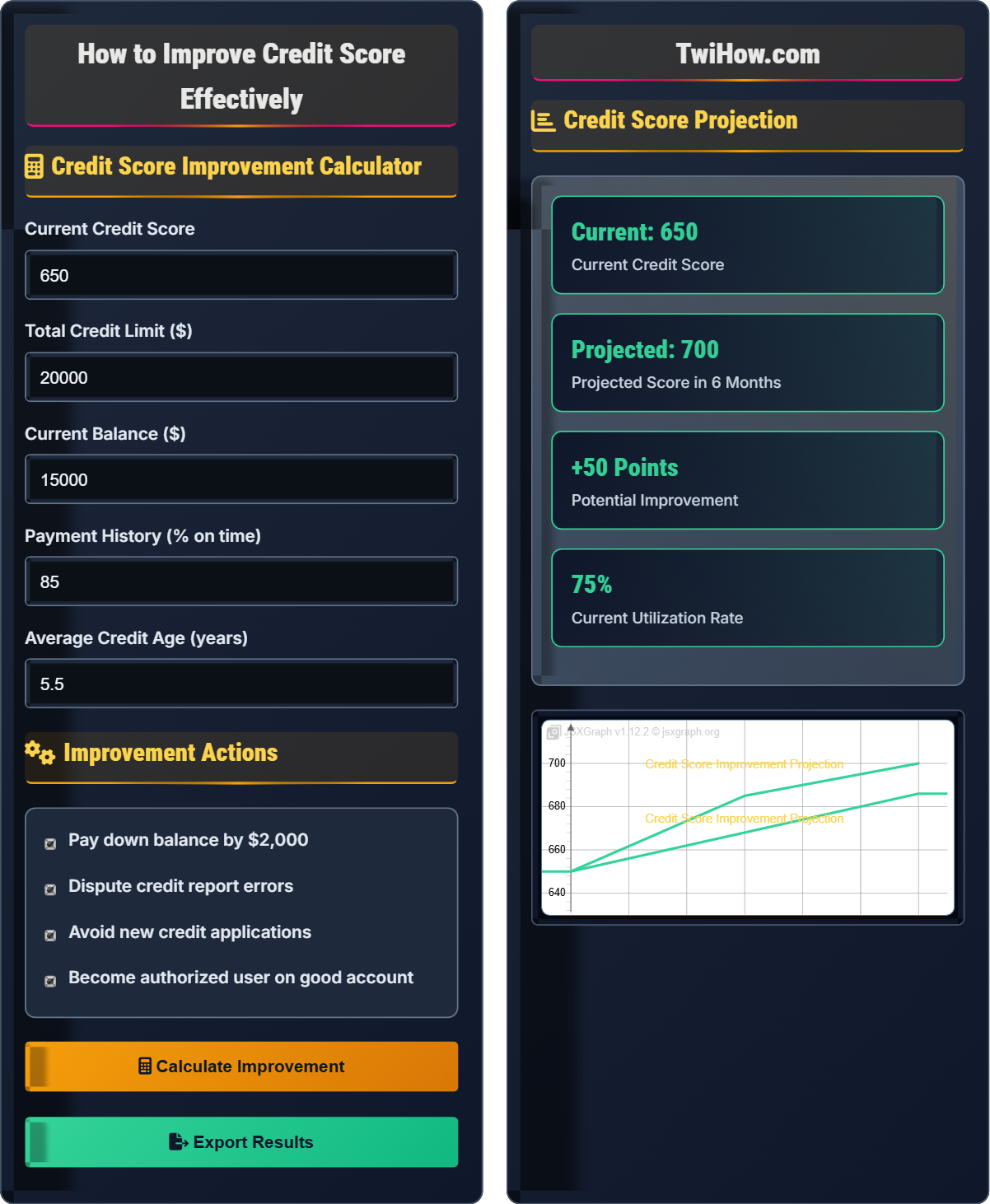

Credit Score Improvement Calculator

Improvement Actions

Credit Score Projection

| Action | Timeline | Potential Impact |

|---|---|---|

| Pay down balances | 1-3 months | +10 to +25 points |

| Fix credit report errors | 1-6 months | +10 to +50 points |

| Make on-time payments | Ongoing | +5 to +15 points |

| Keep old accounts open | Ongoing | +5 to +10 points |

| Add positive tradelines | 3-12 months | +5 to +20 points |

Your credit utilization is the percentage of your available credit that you're using. Aim to keep it below 30%, ideally below 10%. Paying down balances will have the most immediate impact on your score.

Payment history accounts for 35% of your credit score. Setting up automatic payments or calendar reminders can help ensure you never miss a payment.

Understanding Credit Score Factors

Your credit score is calculated based on five main factors, each weighted differently:

Where each factor is scored based on your credit behaviors and reported data.

The FICO scoring model uses these weightings:

- Payment History (35%): Whether you pay on time

- Credit Utilization (30%): Amount owed vs. credit limits

- Length of Credit History (15%): How long you've had credit

- Credit Mix (10%): Different types of credit accounts

- New Credit (10%): Recent credit inquiries and accounts

Effective approaches to boost your credit score:

- Pay Bills on Time: Set up autopay or calendar alerts to never miss a payment

- Reduce Credit Utilization: Pay down balances or request credit limit increases

- Don't Close Old Accounts: Maintain length of credit history

- Limit Hard Inquiries: Only apply for credit when necessary

- Become an Authorized User: Get added to someone else's good-standing account

- Pay More Than Minimum: Reduce balances faster to improve utilization

Credit Score Fundamentals

Credit score, FICO score, credit utilization, payment history, credit mix, length of credit history, credit inquiries.

Total Credit Card Balances ÷ Total Credit Limits = Credit Utilization Ratio

Example: $3,000 in balances ÷ $10,000 in limits = 30% utilization

- Payment history is the most important factor

- Keep utilization below 30%, ideally below 10%

- Never close old accounts unnecessarily

Improvement Strategies

Payment management, debt reduction, credit monitoring, error correction, authorized user benefits.

- Immediate (1-3 months): Pay down balances, fix errors

- Short-term (3-6 months): Establish payment history, manage utilization

- Long-term (6-24 months): Build credit history, optimize mix

- Improvements take time and consistency

- Recent negative events have more impact

- Positive actions take 1-3 months to appear

- Monitoring is essential for success

Credit Score Learning Quiz

Which factor has the greatest impact on your credit score?

Payment history accounts for 35% of your FICO credit score, making it the most important factor. Consistently making on-time payments demonstrates responsible credit management and builds trust with lenders. Even one late payment can significantly impact your score, especially if you have a shorter credit history. Payment history includes mortgage, auto loans, credit cards, and other installment loans.

The answer is B) Payment history.

Understanding the weight of each credit factor is crucial for prioritizing improvement efforts. Since payment history has the largest impact, establishing a perfect payment record should be your top priority. This means setting up automatic payments, calendar reminders, or other systems to ensure you never miss a due date. The impact of payment history is so significant that even with high credit utilization, a perfect payment record can maintain a decent score.

Payment History: Record of whether you pay your bills on time

35% Weight: Largest factor in FICO scoring model

On-Time Payments: Payments made by the due date

• Payment history is worth 35% of your score

• Late payments can stay on your report for 7 years

• One missed payment can drop your score significantly

• Set up automatic payments for all accounts

• Use calendar alerts as backup reminders

• Contact creditors immediately if facing hardship

• Thinking small late fees don't matter

• Not realizing how much impact payment history has

• Not setting up systems to ensure on-time payments

Explain credit utilization and why it's important for your credit score. Provide specific strategies to optimize your utilization ratio.

Credit Utilization Definition: The percentage of your available credit that you're currently using. It's calculated by dividing your total credit card balances by your total credit limits.

Importance: Credit utilization accounts for 30% of your credit score, making it the second most important factor. It indicates to lenders how dependent you are on credit and whether you're managing your debt responsibly.

Optimization Strategies:

1. Pay Down Balances: Focus on reducing existing credit card debt

2. Request Credit Limit Increases: Ask for higher limits without increasing spending

3. Pay Mid-Billing Cycle: Reduce balances before statements post

4. Spread Purchases Across Cards: Keep individual card utilization low

5. Keep Utilization Below 30%: Ideally aim for under 10% for maximum benefit

Credit utilization is a critical factor because it demonstrates your ability to live within your means. Lenders view high utilization as a sign of financial stress or over-reliance on credit. The relationship between utilization and credit scores is exponential - the higher your utilization goes above 30%, the more dramatically it can hurt your score. This makes it one of the most impactful factors to address quickly.

Credit Utilization: Percentage of available credit currently in use

Formula: Total Balances ÷ Total Credit Limits

Target Range: Below 30%, ideally below 10%

• Credit utilization is worth 30% of your score

• Lower utilization is always better

• Scores can improve within 1-3 months of reducing utilization

• Pay twice per month to keep balances low

• Don't close credit cards after paying them off

• Monitor utilization before making large purchases

• Carrying high balances thinking they'll pay them off later

• Closing credit cards after paying them off

• Not understanding that utilization matters for individual cards

Jennifer has a credit score of 620 with $8,000 in credit card debt on a $10,000 limit across two cards. She pays her bills on time but has never had a loan. Her oldest credit card is 2 years old. She wants to buy a house in 12 months and needs a score of 720+. What specific steps should Jennifer take to improve her score, and what is the realistic timeline for achieving her goal?

Current Issues: Jennifer's credit utilization is 80% ($8,000/$10,000), which is extremely high and hurting her score significantly. Her short credit history (2 years) and limited credit mix (only credit cards) are also holding back her score.

Recommended Steps:

1. Pay Down Debt Immediately: Target reducing balances to under $3,000 (30% utilization) within 2-3 months

2. Open an Installment Loan: Consider a credit-builder loan or small personal loan to add to credit mix

3. Continue On-Time Payments: Maintain perfect payment history

4. Keep Accounts Open: Don't close any existing accounts

5. Monitor Progress: Check score monthly to track improvements

Realistic Timeline: With aggressive action, Jennifer could realistically achieve a score of 680-700 within 6 months and potentially reach 720+ within 12 months. The biggest improvement will come from reducing her utilization from 80% to under 30%.

This example demonstrates how addressing the most impactful factors first can yield significant improvements. Jennifer's high utilization is the primary drag on her score, so paying down debt will have the most immediate impact. Adding an installment loan will improve her credit mix, which accounts for 10% of her score. The combination of these actions, along with maintaining her good payment history, positions her well to reach her goal.

Credit Utilization: Currently 80% ($8,000/$10,000), needs to be under 30%

Credit Mix: Currently only revolving credit (credit cards), needs installment loan

Perfect Payment History: Positive factor in her favor

• High utilization is the primary issue to address

• Payment history is already strong

• Adding credit mix can help over time

• Pay down to under 30% utilization immediately

• Consider credit-builder loans from credit unions

• Don't apply for multiple new accounts at once

• Not realizing how much high utilization impacts scores

• Closing old accounts while trying to improve credit

• Applying for multiple new accounts to build credit

David discovered his credit report contains a $2,000 charge-off that he believes is incorrect. The account is listed as being 180 days past due and was sold to collections. His current score is 610. Explain the credit dispute process and estimate the potential impact on David's score if the item is successfully removed.

Credit Dispute Process:

1. Obtain Credit Reports: Get copies from all three bureaus (Experian, Equifax, TransUnion)

2. Identify Inaccuracies: Document the specific error with dates and details

3. File Disputes: Submit disputes online, by phone, or in writing to each bureau

4. Provide Documentation: Include any evidence supporting your claim

5. Follow Up: Bureaus have 30 days to investigate and respond

6. Verify Changes: Request updated reports after resolution

Estimated Impact: Removing a charged-off account could improve David's score by 25-50 points, depending on other factors. Charged-off accounts are among the most damaging items on credit reports. The improvement would likely be realized within 1-2 months of removal.

Regular credit monitoring is essential for identifying and correcting errors. Many people unknowingly carry incorrect negative information on their reports for years. The credit dispute process is legally protected under the Fair Credit Reporting Act, which requires bureaus to investigate disputed items. Successful disputes can provide quick improvements to credit scores, especially when dealing with serious delinquencies.

Charge-Off: Creditor writes off debt as unlikely to be collected

Collection Account: Debt sold to third-party collection agency

Fair Credit Reporting Act: Federal law governing credit reporting practices

• Bureaus must investigate disputes within 30 days

• Information must be accurate or removed

• Disputes can be filed free of charge

• Check credit reports annually at AnnualCreditReport.com

• Dispute all three bureaus separately

• Keep records of all correspondence

• Not monitoring credit reports regularly

• Not disputing errors when found

• Hiring expensive credit repair companies unnecessarily

Which strategy would be MOST effective for someone with no credit history looking to establish credit?

Opening a secured credit card and using it responsibly is the most effective approach for building credit from scratch. Secured cards require a cash deposit that becomes your credit limit, making approval nearly guaranteed. When used properly (small purchases paid in full monthly), they establish a positive payment history and demonstrate responsible credit management. This addresses both payment history (35%) and credit utilization (30%) factors simultaneously.

The answer is C) Open a secured credit card and use it responsibly.

Building credit from scratch requires starting with accessible credit products and demonstrating responsible behavior over time. Secured credit cards are specifically designed for this purpose, offering a safe way for lenders to extend credit while allowing consumers to build history. The key is consistent, responsible use over 6-12 months, which establishes the foundation for accessing unsecured credit later.

Secured Credit Card: Requires cash deposit as collateral

Authorized User: Someone added to another person's account

Payment History: Most important factor in credit scoring

• Start with secured credit cards when building credit

• Make small purchases and pay in full monthly

• Avoid applying for multiple accounts at once

• Look for secured cards that report to all three bureaus

• Use 10-20% of available credit responsibly

• Set up automatic payments to avoid missed payments

• Applying for multiple cards at once

• Not understanding the importance of payment history

• Closing accounts after paying them off

FAQ

Q: How long does it take to see improvements in my credit score after I start making changes?

A: The timeline for credit score improvements varies depending on the changes you make. Some improvements can be seen relatively quickly:

• Paying down credit card balances: 1-3 months

• Fixing credit report errors: 1-6 months

• Establishing payment history: 3-6 months

• Building credit history length: 12+ months

Generally, you can expect to see modest improvements within 3-6 months of implementing positive habits, with more significant improvements possible within 12-24 months. The most dramatic improvements often come from reducing high credit utilization ratios.

Q: Is it better to close old credit card accounts I'm not using, or keep them open?

A: Generally, it's better to keep old credit card accounts open, especially if they have no annual fee. Here's why:

1. Length of Credit History (15% of score): Older accounts increase your average account age

2. Credit Utilization: Closing accounts reduces your total available credit, potentially increasing your utilization ratio

3. Credit Mix: Maintaining different types of credit accounts helps your score

The only exception might be if an account has a high annual fee that outweighs the benefits. Otherwise, keeping old accounts open, even if inactive, helps your credit profile. Just use them occasionally for small purchases and pay them off immediately to keep them active.