How Do I Prepare Financially for Career Changes or Unemployment?

Complete guide • Step-by-step transition strategies

Career Transition Financial Planning:

Show Transition PlannerPreparing financially for career changes or unemployment is crucial for maintaining financial stability during uncertain times. This involves building an emergency fund, reducing debt, developing transferable skills, and creating a financial safety net. The key is to prepare before you need it, as financial stress during transitions can limit your options.

Essential preparation strategies:

- Emergency Fund: 3-6 months of living expenses in liquid savings

- Debt Reduction: Pay down high-interest debt to reduce monthly obligations

- Skills Development: Continuously update marketable skills

- Insurance Coverage: Maintain health and disability insurance

- Network Building: Cultivate professional relationships for opportunities

Having a financial cushion provides peace of mind and allows you to be more selective during your job search, potentially leading to better career outcomes.

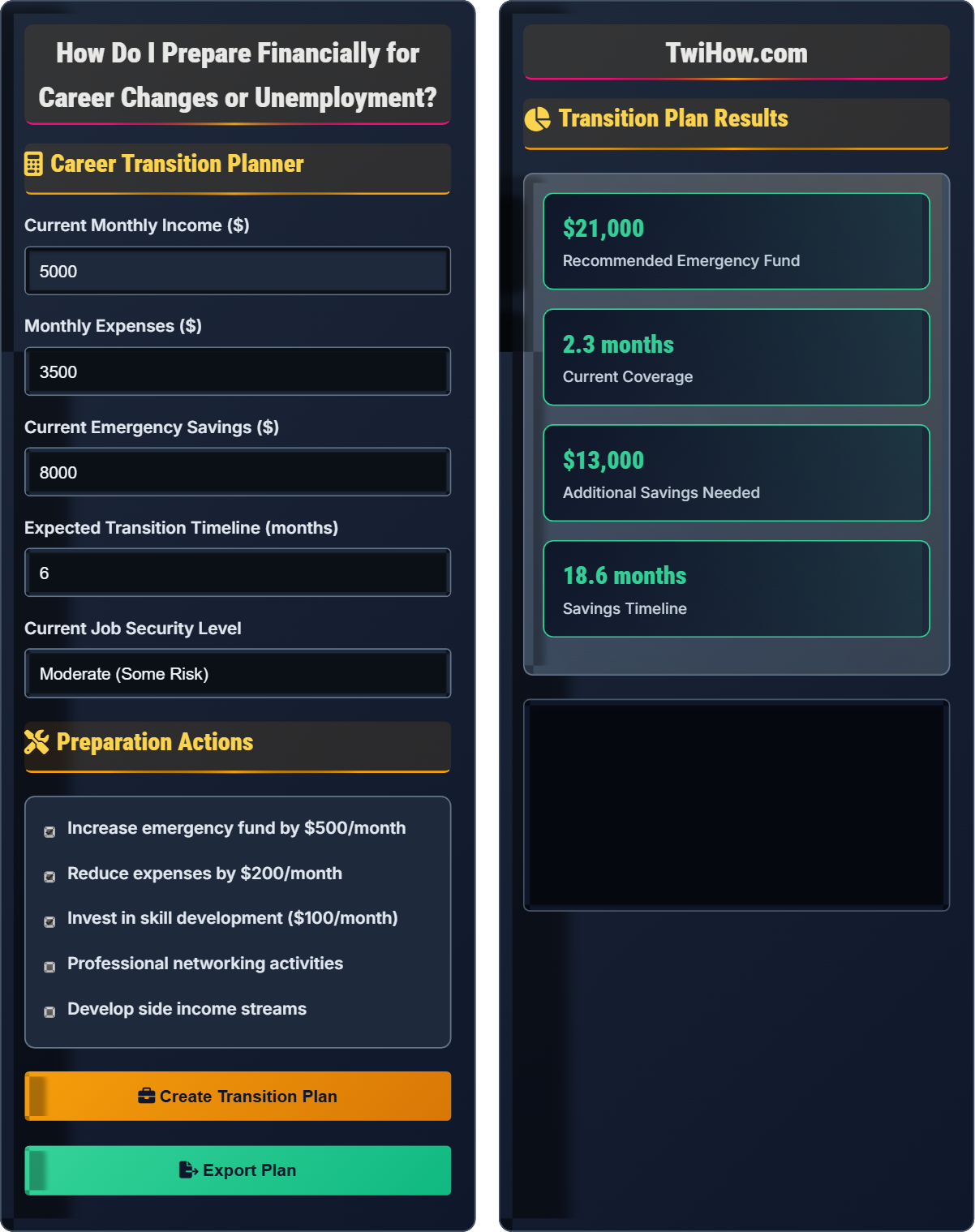

Career Transition Planner

Preparation Actions

Transition Plan Results

| Item | Current | Recommended | Gap |

|---|---|---|---|

| Monthly Expenses | $3,500 | $3,500 | $0 |

| Emergency Fund | $8,000 | $21,000 | $13,000 |

| Months Covered | 2.3 | 6.0 | 3.7 |

| Monthly Savings | $0 | $500 | $500 |

Immediate Actions

- Start building emergency fund if you haven't already

- Reduce non-essential expenses immediately

- Update resume and LinkedIn profile

- Reach out to professional network

- Research unemployment benefits in your area

Preparation Timeline

- Month 1-2: Build initial emergency fund to 3 months coverage

- Month 3-4: Reduce expenses and increase savings rate

- Month 5-6: Complete skill development and networking

- Month 7+: Achieve full 6-month emergency fund

- Ongoing: Maintain fund and update skills regularly

Career Transition Financial Planning Explained

Career transition planning is the process of preparing financially for potential job changes, layoffs, or career shifts. This involves building an emergency fund, reducing financial obligations, developing marketable skills, and creating a financial safety net. The goal is to maintain financial stability during periods of uncertainty while preserving career options.

The recommended emergency fund calculation:

Where:

- Monthly Expenses: Total monthly living costs (housing, food, utilities, etc.)

- Months of Coverage: Typically 3-6 months (more for higher job insecurity)

Essential elements of career transition preparation:

- Emergency Fund: Liquid savings for 3-6 months of expenses

- Debt Management: Reduce high-interest obligations

- Insurance Coverage: Maintain health and disability protection

- Skills Portfolio: Marketable abilities and certifications

- Professional Network: Contacts for opportunities and referrals

- Job Search Resources: Resume, portfolio, and references

- Start Early: Begin preparation before facing immediate risk

- Automate Savings: Set up automatic transfers to emergency fund

- Monitor Expenses: Track spending to identify reduction opportunities

- Continuous Learning: Regularly update skills and certifications

- Network Actively: Maintain professional relationships year-round

Transition Planning Fundamentals

Emergency fund, job security, career transition, unemployment planning, financial safety net.

Emergency Fund = Monthly Expenses × Months of Coverage

Where monthly expenses include all essential living costs.

- Always aim for 3-6 months of expenses in reserve

- Keep emergency funds in liquid accounts

- Build fund gradually but consistently

Real-World Examples

Industry changes, company restructuring, career pivots, economic downturns.

- Calculate monthly expenses including all obligations

- Set up dedicated emergency fund account

- Automate monthly savings transfers

- Reduce discretionary spending

- Invest in skill development

- Build and maintain professional network

- Start building emergency fund immediately

- Keep fund separate from regular savings

- Only use for true emergencies

- Replenish after any use

Career Transition Planning Quiz

How many months of expenses should you ideally have in an emergency fund for career transition preparedness?

The ideal emergency fund size for career transition preparedness is 3-6 months of expenses. This provides sufficient time to find a new position while maintaining financial stability. The exact amount depends on your job security, industry stability, and personal circumstances. For higher-risk situations, you might consider extending to 6-12 months.

The answer is B) 3-6 months.

The 3-6 month rule balances practicality with security. Too little provides insufficient protection, while too much ties up funds that could be invested. The average job search takes 3-6 months, making this timeframe reasonable. Consider your specific situation - if you're in a volatile industry or have dependents, lean toward the higher end of the range.

Emergency Fund: Liquid savings reserved for unexpected expenses

Job Security: Stability of current employment position

Financial Safety Net: Resources available during income disruptions

• Match fund size to risk level

• Keep funds liquid and accessible

• Reassess regularly based on circumstances

• Start with 1 month and build gradually

• Use high-yield savings accounts

• Keep separate from other savings goals

• Having no emergency fund

• Investing emergency funds in risky assets

• Using fund for non-emergencies

If your monthly expenses are $4,200 and you want to prepare for a potential career transition lasting 5 months, how much should your emergency fund be?

Emergency Fund = Monthly Expenses × Months of Coverage

Emergency Fund = $4,200 × 5 = $21,000

Your emergency fund should be $21,000 to cover 5 months of expenses during a career transition. This provides financial security while searching for new employment.

This calculation demonstrates the straightforward arithmetic behind emergency fund planning. The key is to include all essential expenses - housing, food, utilities, insurance, minimum debt payments, and other necessities. Avoid including discretionary spending like entertainment or dining out in your emergency fund calculation.

Essential Expenses: Necessary costs for basic living

Discretionary Expenses: Optional spending for non-necessities

Financial Security: Stability provided by adequate reserves

• Include all essential expenses

• Exclude discretionary spending

• Adjust for your specific situation

• Track expenses for 3 months to get average

• Include seasonal expenses in average

• Add 10% buffer for unexpected costs

• Underestimating actual expenses

• Including non-essential costs

• Not adjusting for personal circumstances

You're in a declining industry with high job insecurity. Your monthly expenses are $3,800 and you currently have $10,000 in savings. You can save $600 per month. How long will it take to build an adequate emergency fund for your situation, and what additional strategies should you consider?

Recommended Emergency Fund: For high job insecurity, aim for 6 months of expenses: $3,800 × 6 = $22,800

Current Savings: $10,000

Amount Needed: $22,800 - $10,000 = $12,800

Time to Goal: $12,800 ÷ $600/month = 21.3 months

Additional Strategies:

• Reduce monthly expenses to increase savings rate

• Develop additional income streams

• Invest in skills that are in demand

• Expand professional network actively

• Consider temporary contract work to bridge gaps

Given the high risk, you should also explore opportunities in more stable industries.

This example shows how risk level affects preparation strategy. Higher job insecurity requires larger emergency funds and more aggressive preparation. The time calculation helps set realistic expectations for preparation. The additional strategies demonstrate that financial preparation is only one component of career transition planning.

Job Insecurity: Uncertainty about employment stability

Risk-Adjusted Planning: Preparation scaled to actual risk levelIncome Diversification: Multiple revenue sources for security

• Adjust fund size to risk level

• Consider timeline for building fund

• Combine financial and career strategies

• Increase savings rate during good times

• Build skills during employment for later

• Maintain network even when employed

• Using same fund size for all risk levels

• Not considering preparation timeline

• Focusing only on financial preparation

You work in retail where automation is reducing jobs. You want to transition to tech but need 8 months to gain necessary skills. Your current monthly expenses are $3,200. How should you structure your financial preparation for this transition, considering you'll have reduced income during training?

Extended Emergency Fund Needed: For an 8-month transition with potential reduced income, prepare for 10-12 months of expenses: $3,200 × 12 = $38,400

Preparation Strategy:

• Build fund before starting transition (2+ years of saving)

• Consider part-time training while working

• Look into income during training (teaching assistant, internships)

• Reduce expenses before beginning transition

• Explore accelerated training programs to reduce timeline

• Maintain current job while training when possible

This approach provides security while pursuing career advancement.

This scenario demonstrates how career transitions requiring education or training need extended financial preparation. The key insight is that you need to fund both the transition period and potentially reduced income during skill development. The solution shows how to adjust the standard emergency fund formula for extended transitions.

Career Transition: Shift to a different field or role

Skills Gap: Difference between current and required abilities

Extended Emergency Fund: Larger reserve for prolonged transitions

• Extend fund for longer transitions

• Plan for reduced income during training

• Start preparation well in advance

• Pursue training part-time while working

• Look for employer-sponsored education

• Consider related fields that require less retraining

• Not extending fund for training periods

• Quitting job before securing new income

• Underestimating transition timeframes

What should you do regarding unemployment benefits when preparing for a potential job loss?

The best approach is to research unemployment benefits but not depend on them. Unemployment benefits are helpful but often cover only a portion of your salary, have time limits, and require specific eligibility criteria. They should supplement, not replace, your emergency fund. Research the application process, benefit amounts, and duration in your state in advance.

The answer is B) Research benefits but don't depend on them.

Unemployment benefits provide temporary assistance but shouldn't be the foundation of your transition planning. They typically replace only 40-50% of your salary and have duration limits (usually 26 weeks). Eligibility requirements can be restrictive, and benefits may not be available if you quit voluntarily. Your emergency fund should cover your full expenses for the expected transition period.

Unemployment Benefits: Government assistance for jobless workers

Eligibility Requirements: Conditions for receiving unemployment

Benefit Replacement Rate: Percentage of salary replaced

• Research benefits in advance

• Don't rely on benefits as primary support

• Understand eligibility requirements

• Know your state's benefit rules

• Understand the application timeline

• Prepare documentation in advance

• Assuming benefits will cover all expenses

• Not understanding eligibility criteria

• Delaying application process

FAQ

Q: I'm a recent graduate with student loans. How do I build an emergency fund while paying debt?

A: For recent graduates with student loans:

1. Start Small: Build a mini-emergency fund of $1,000-$2,000 first

2. Parallel Approach: Make minimum loan payments while saving small amounts

3. Automate: Set up automatic transfers to both savings and loan payments

4. Income Growth: As your income increases, boost emergency fund contributions

5. Prioritize: Focus on high-interest debt while maintaining emergency fund

6. Side Income: Use additional income to accelerate both savings and debt repayment

Once you have a mini-emergency fund, you can focus more heavily on debt while continuing to build the fund to 3-6 months of expenses.

Q: How do I balance saving for retirement with building an emergency fund?

A: The priority order:

• Step 1: Build mini-emergency fund ($1,000-$2,500)

• Step 2: Maximize employer 401(k) match (free money)

• Step 3: Complete emergency fund (3-6 months expenses)

• Step 4: Continue retirement contributions

• Step 5: Additional emergency fund if desired

This approach captures employer benefits while building financial security. The emergency fund protects your retirement savings from being raided during crises, which would disrupt long-term growth.

After establishing both, you can contribute to both simultaneously based on your financial capacity.

Q: How do I prepare for career changes when I have dependents?

A: For families with dependents:

• Larger Emergency Fund: Consider 6-12 months of expenses due to higher responsibilities

• Spousal Employment: If applicable, coordinate with partner's career stability

• Insurance: Maintain adequate life and disability insurance

• Childcare: Plan for potential changes in childcare arrangements during transitions

• Education: Consider impact on children's education funding

• Communication: Discuss financial plans with family members appropriately

• Flexibility: Consider remote work or consulting to maintain income during transitions

The goal is to provide maximum security for your family while maintaining career flexibility.

Consider involving your spouse in career planning discussions to coordinate financial strategies.