Benefits of Automating Savings and Investments

Systematic investing • Compound growth • Wealth building

Automated Investing Fundamentals:

Calculate Automation BenefitsAutomating your savings and investments is one of the most powerful wealth-building strategies. By setting up automatic transfers, you take advantage of dollar-cost averaging, compound interest, and behavioral finance principles. Automation removes the decision-making process that often leads to inconsistent saving habits.

Key Benefits: Consistency, discipline, dollar-cost averaging, compound growth, reduced emotional investing.

Essential components of automated investing:

- Automatic Transfers: Set up recurring transfers from checking to savings/investment accounts

- Payroll Deduction: Contribute directly through your employer's benefits system

- App-Based Automation: Use fintech apps to round up purchases or invest spare change

- Robo-Advisors: Automated portfolio management and rebalancing

- Target-Date Funds: Automatically adjusts allocation as you age

Studies show that people who automate their savings save 2-3 times more than those who rely on manual transfers. The key is to make saving and investing as effortless as possible.

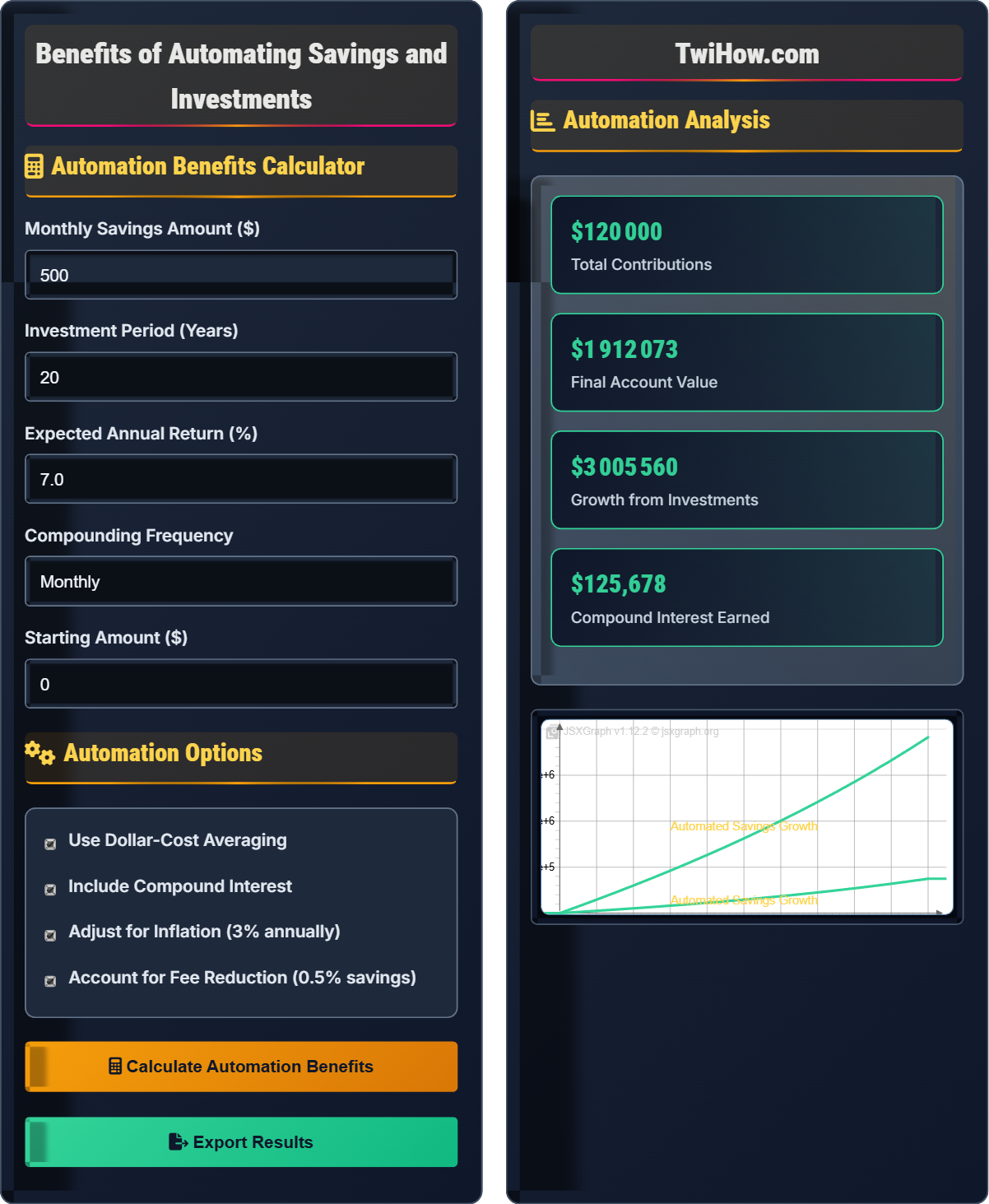

Automation Benefits Calculator

Automation Options

Automation Analysis

| Benefit | Description | Impact |

|---|---|---|

| Consistency | Regular contributions regardless of market conditions | Higher savings rate |

| Discipline | Removes emotional decision-making | Reduced timing risk |

| Dollar-Cost Averaging | Buying more when prices are low, less when high | Smoothing returns |

| Compound Growth | Investment returns generate their own returns | Exponential growth |

| Fee Reduction | Lower management fees with index funds | Higher net returns |

Set up automatic deductions through your employer's benefits system. This ensures contributions are made before you have a chance to spend the money.

Automate transfers from checking to savings/investment accounts on payday. This ensures consistent contributions regardless of your willpower.

Use fintech apps that round up purchases to the nearest dollar and invest the spare change. This makes saving effortless and painless.

Understanding Automated Investment Benefits

The future value of automated savings with regular contributions is calculated as:

Where FV = Future Value, PV = Present Value, r = periodic return rate, n = number of periods, PMT = periodic payment.

Compound interest accelerates wealth building over time:

Where A = final amount, P = principal, r = annual interest rate, n = number of times interest is compounded per year, t = time in years.

Effective approaches to maximize automated savings benefits:

- Payroll Deduction: Contribute directly through your employer's system

- Round-Up Services: Use apps that invest spare change from purchases

- Robo-Advisors: Automated portfolio management and rebalancing

- Target-Date Funds: Automatically adjusts allocation over time

- Auto-Increase: Set up automatic contribution increases

- Separate Accounts: Keep investment accounts separate from spending accounts

Automation Fundamentals

Automated savings, dollar-cost averaging, compound interest, systematic investing, behavioral finance, auto-enrollment.

FV = PV(1+r)^n + PMT[((1+r)^n - 1)/r]

Where FV = Future Value, PV = Present Value, r = rate of return, n = number of periods, PMT = periodic payment.

- Set up automatic transfers on payday

- Choose low-cost index funds

- Review and rebalance annually

Investment Strategies

Payroll deduction, bank transfers, round-up apps, robo-advisors, target-date funds, auto-increase.

- Start with payroll deduction if available

- Supplement with bank transfers

- Use round-up apps for spare change

- Consider robo-advisors for management

- Set up auto-increase features

- Choose accounts with low fees

- Ensure sufficient liquidity

- Align investments with goals

- Monitor performance regularly

Automation Learning Quiz

What is the primary benefit of dollar-cost averaging through automated investing?

The primary benefit of dollar-cost averaging is reducing timing risk and smoothing returns. By investing fixed amounts regularly, you buy more shares when prices are low and fewer when prices are high, which averages out your purchase price over time. This removes the pressure of trying to time the market and helps smooth out market volatility.

The answer is C) Reducing timing risk and smoothing returns.

Dollar-cost averaging is a disciplined investment strategy that works by removing emotion from investment timing decisions. When you invest regularly regardless of market conditions, you naturally take advantage of market volatility. This strategy is particularly effective when combined with automation, as it ensures consistency in your investment approach.

Dollar-Cost Averaging: Investing fixed amounts at regular intervals

Timing Risk: Risk of investing at market peaks

Market Volatility: Fluctuations in investment prices

• Doesn't guarantee profits

• Works best with long-term investing

• Reduces timing risk

• Combine with automated transfers

• Use during volatile market periods

• Maintain consistency over time

• Expecting guaranteed returns

• Confusing with market timing

• Stopping during market downturns

Explain the behavioral finance benefits of automating savings and investments, and how automation helps overcome common psychological barriers to saving.

Behavioral Finance Benefits: Automation addresses several psychological barriers to saving:

Loss Aversion: People feel losses more strongly than gains. Manual transfers feel like losses, while automated transfers are invisible, reducing this psychological barrier.

Procrastination: Automation removes the need to make a decision each month, preventing delays in saving.

Present Bias: Humans prefer immediate rewards over future benefits. Automation makes saving automatic, bypassing the temptation to spend now.

Decision Fatigue: Making constant financial decisions depletes mental energy. Automation conserves this energy for other important decisions.

Self-Control Problems: Automated transfers prevent impulsive spending of money intended for savings.

Research shows: People who automate their savings save 2-3 times more than those who rely on manual transfers, demonstrating the power of removing psychological barriers.

Understanding the psychological barriers to saving is crucial for long-term success. Our brains are wired to prioritize immediate gratification, making it difficult to consistently save for the future. Automation works by restructuring our environment to make saving the default option, which aligns with how our decision-making processes actually work.

Behavioral Finance: Study of psychology in financial decisions

Loss Aversion: Feeling losses more strongly than gains

Present Bias: Preference for immediate rewards

• Automation removes decision fatigue

• Makes saving the default option

• Bypasses psychological barriers

• Set up automation on payday

• Make it harder to cancel than to start

• Use separate accounts for investments

• Not considering psychological barriers

• Underestimating the power of defaults

• Focusing only on rational factors

Sarah earns $5,000 monthly and wants to save $500 each month for retirement. She's considering two approaches: 1) Manual transfers when she remembers, or 2) Automated payroll deduction of $500 monthly. Based on behavioral finance principles, analyze which approach would be more effective and estimate the likely difference in savings over 10 years.

Analysis: The automated payroll deduction approach will be significantly more effective due to behavioral finance principles:

Manual Transfers: Subject to procrastination, decision fatigue, and competing priorities. Studies show people only follow through on about 60-70% of manual savings intentions.

Automated Deductions: Removes decision-making, operates as a "default" option, and feels less like a loss since the money is never in the checking account.

10-Year Projection:

Manual: $500 × 12 × 10 × 0.65 = $39,000 (65% compliance rate)

Automated: $500 × 12 × 10 = $60,000 (100% compliance)

Difference: $21,000 in contributions alone

With 7% annual return, the automated approach could result in nearly $40,000 more in account value after 10 years.

Recommendation: Sarah should definitely choose the automated payroll deduction approach to maximize her retirement savings.

This example demonstrates how behavioral factors can have a dramatic impact on financial outcomes. The difference between manual and automated approaches isn't just about discipline—it's about understanding how our brains work and designing systems that work with our psychology rather than against it. The compound effect of consistent savings creates substantial differences over time.

Default Option: The choice that occurs if no action is taken

Compliance Rate: Percentage of intended actions actually performed

Behavioral Nudges: Designing choices to influence behavior

• Defaults have powerful influence on behavior

• Manual approaches suffer from low compliance

• Automation maintains 100% compliance

• Use payroll deduction when available

• Make cancellation harder than enrollment

• Set up automation on payday

• Underestimating the impact of behavioral factors

• Assuming discipline will overcome psychology

• Not considering the compounding effect of consistency

Compare two investors: Alex saves $200 monthly for 30 years starting at age 25, while Ben saves $400 monthly for 20 years starting at age 35. Both earn 7% annually. Calculate the final amounts and explain why Alex ends up with more despite saving less total money.

Calculations:

Alex: $200/month × 360 months = $72,000 contributed over 30 years

Future Value: $200 × [((1.07/12)^(30×12) - 1) / (0.07/12)] ≈ $244,000

Ben: $400/month × 240 months = $96,000 contributed over 20 years

Future Value: $400 × [((1.07/12)^(20×12) - 1) / (0.07/12)] ≈ $204,000

Explanation: Alex's money has 10 additional years to compound. The power of compound interest means that money invested earlier grows exponentially more than money invested later. Even though Alex contributed $24,000 less, the additional 10 years of compounding resulted in a final balance $40,000 higher.

Key Insight: Time is more important than the amount saved when it comes to compound interest. This demonstrates why starting early and maintaining consistency is crucial for wealth building.

This example illustrates the exponential nature of compound interest. The earlier you start investing, the more dramatic the effect of compounding becomes. This is why automation is so powerful—it helps you start early and stay consistent, maximizing the time your money has to grow. The mathematical advantage of early investment is substantial.

Compound Interest: Interest earned on both principal and previous interest

Time Value of Money: Money available now is worth more than later

Exponential Growth: Growth that accelerates over time

• Time is more valuable than money in compound growth

• Early investment has exponential advantages

• Consistency maximizes compounding effects

• Start investing as early as possible

• Maintain consistent contributions

• Let compound interest work over time

• Underestimating the power of compound interest

• Delaying investment initiation

• Not appreciating the exponential nature of growth

Which of the following is the MOST effective method for automating retirement savings?

Setting up payroll deduction through your employer is the most effective method. Payroll deductions are taken directly from your paycheck before you have a chance to spend the money, making it the most reliable form of automation. This approach ensures 100% compliance, removes decision-making, and takes advantage of employer matching programs when available. The money never enters your checking account, eliminating the temptation to spend it.

The answer is C) Setting up payroll deduction through your employer.

Payroll deduction is the gold standard for automation because it operates at the source of your income. By taking money out before it reaches your account, you eliminate the psychological barrier of having to "send" money to savings. This approach is also typically integrated with employer benefits, potentially including matching contributions that provide immediate returns on your investment.

Payroll Deduction: Automatic deduction from paycheck

Source Deduction: Taking money at the source of income

Employer Matching: Company contribution to retirement plan

• Source deductions are most effective

• Employer matching is free money

• Early automation prevents spending temptation

• Maximize employer matching first

• Set up deductions on payday

• Use multiple automation methods

• Not taking advantage of employer matching

• Choosing methods with lower compliance

• Not starting automation early enough

FAQ

Q: What if I need to access my automated savings? Won't automation lock my money away?

A: Automation doesn't lock your money away - it simply moves it to the appropriate account type where you can access it when needed. Here's how to maintain flexibility:

1. Emergency Fund: Keep 3-6 months of expenses in a high-yield savings account that's easily accessible

2. Account Types: Use taxable brokerage accounts for medium-term goals (accessible anytime) and retirement accounts for long-term goals

3. Transfer Flexibility: Most automated systems allow you to pause or redirect transfers

4. Time Horizons: Match account types to your time horizons - short-term goals in liquid accounts, long-term in investments

The key is having a balanced approach where you automate for different purposes and time horizons while maintaining adequate liquidity for emergencies.

Q: How much should I automate? Is there a rule of thumb for the percentage of income to save automatically?

A: The general recommendation is to save 10-20% of your gross income for retirement and long-term goals:

• 20s: Start with 10-12%, increase as income grows

• 30s-40s: Aim for 15-18% to catch up

• 50s+: Try to save 20% or more for retirement catch-up

Practical approach:

1. Start with whatever you can afford (even 3-5%)

2. Increase by 1% each year or with raises

3. Maximize employer matching first

4. Automate the increases so they happen without decision-making

Remember that these are targets - start where you can and build up gradually. The most important thing is to start the habit of consistent saving.