First Steps to Becoming Debt-Free

Step-by-step guide • Debt payoff strategies

Debt Elimination Fundamentals:

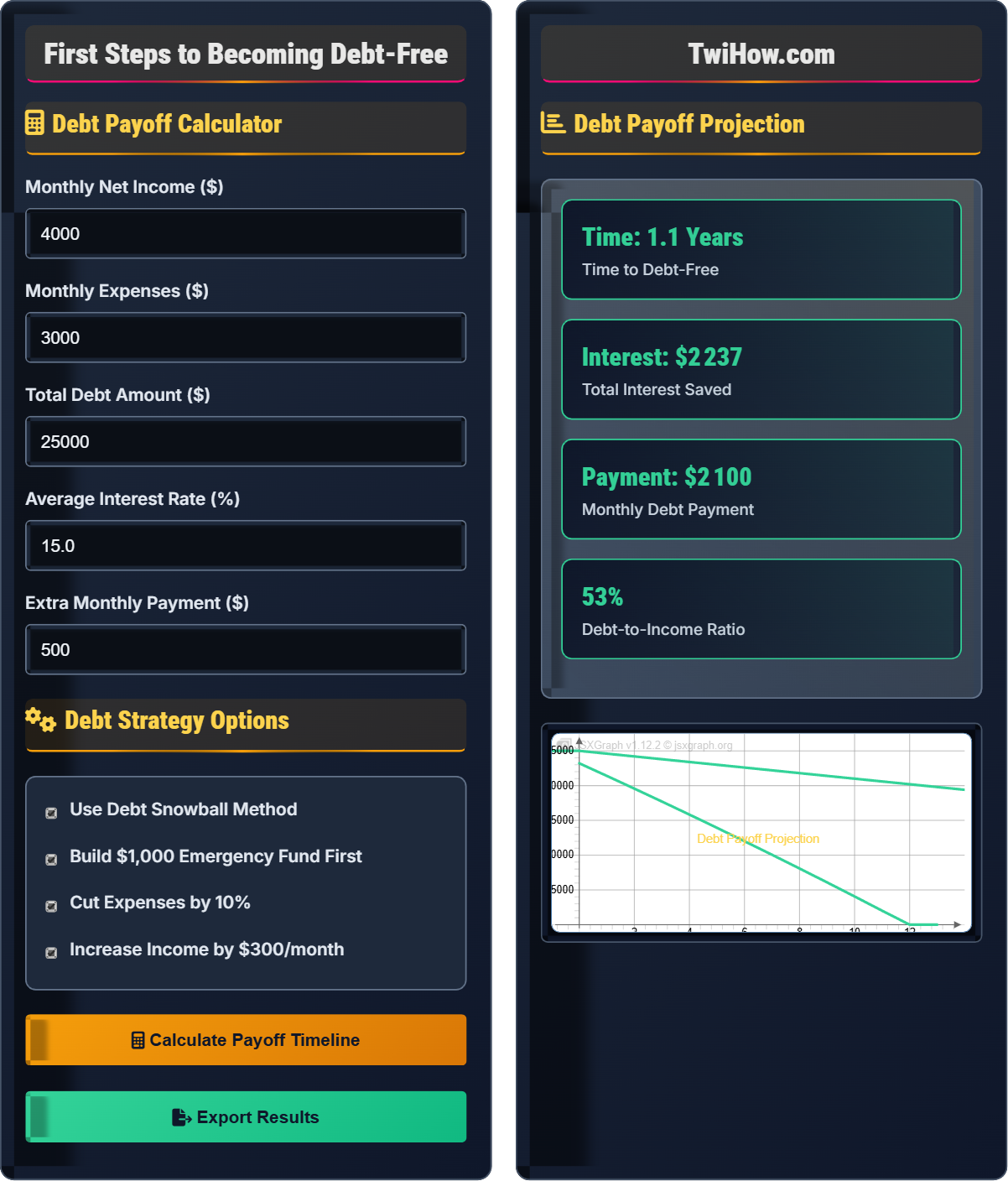

Calculate Payoff TimelineBecoming debt-free is a journey that starts with understanding your current financial position and taking concrete steps toward debt elimination. The path to financial freedom involves creating a comprehensive debt payoff plan, choosing the right strategy for your situation, and maintaining discipline throughout the process.

Debt Snowball Method: Pay smallest debts first for psychological wins

Debt Avalanche Method: Pay highest interest debts first for maximum savings

Key steps to becoming debt-free:

- Assess Your Debt: List all debts with balances, interest rates, and minimum payments

- Create a Budget: Track income and expenses to find money for debt payments

- Choose a Strategy: Select the debt payoff method that fits your personality

- Build an Emergency Fund: Prevent new debt from unexpected expenses

- Stay Motivated: Celebrate milestones and visualize debt-free life

With dedication and the right strategy, most people can become debt-free within 2-5 years. The key is consistency and commitment to your debt elimination plan.

Debt Payoff Calculator

Debt Strategy Options

Debt Payoff Projection

| Method | Pros | Cons | Best For |

|---|---|---|---|

| Debt Snowball | Motivational wins, momentum building | Pays more interest overall | Psychological motivation |

| Debt Avalanche | Minimizes interest paid | Slower initial progress | Mathematical efficiency |

| Debt Consolidation | Lower interest rate, single payment | Requires good credit, potential fees | Multiple high-interest debts |

Focus on creating a detailed budget, cutting unnecessary expenses, and building a small emergency fund. Start making extra debt payments immediately.

Apply all extra income toward debt payments. Consider side hustles or selling unused items to generate additional cash for debt elimination.

With smaller debts eliminated, focus all resources on the largest remaining debt. Celebrate milestones and stay motivated for the finish line.

Understanding Debt Payoff Strategies

The time to pay off debt can be calculated using the compound interest formula:

Where Payment is monthly payment amount, Principal is debt amount, and Rate is monthly interest rate.

Debt-to-income ratio is calculated as:

A DTI below 36% is considered healthy, with 20% being ideal for debt elimination.

Effective approaches to accelerate debt elimination:

- Debt Snowball: Pay smallest debts first for motivational wins

- Debt Avalanche: Pay highest interest debts first to save money

- Budget Optimization: Find extra money by cutting expenses

- Side Income: Generate additional income for debt payments

- Debt Consolidation: Combine multiple debts into one lower-rate loan

- Balance Transfer: Move high-rate debt to low-rate cards

Debt Elimination Fundamentals

Debt snowball, debt avalanche, debt-to-income ratio, compound interest, budgeting, emergency fund.

Time = log(Payment/(Payment - Principal×Rate)) / log(1 + Rate)

Where Payment = monthly payment, Principal = debt amount, Rate = monthly interest rate.

- Always make minimum payments on all debts

- Apply extra money to one debt at a time

- Don't take on new debt while eliminating existing debt

Payoff Strategies

Debt snowball, debt avalanche, debt consolidation, balance transfers, income optimization.

- Debt Snowball: Smallest debts first for motivation

- Debt Avalanche: Highest interest debts first for savings

- Debt Consolidation: Combine debts to lower interest

- Balance Transfer: Move to lower-rate accounts

- Choose strategy that matches your personality

- Consider both psychological and financial factors

- Build emergency fund to prevent new debt

- Stay consistent with your chosen approach

Debt Elimination Learning Quiz

Which debt payoff strategy focuses on paying off the smallest debts first regardless of interest rate?

The Debt Snowball method focuses on paying off the smallest debts first, regardless of their interest rates. This approach provides psychological wins as debts are eliminated quickly, which can motivate people to continue their debt elimination journey. While it may not be mathematically optimal (since higher-interest debts accumulate more interest), the motivation gained from early wins can lead to greater success in becoming debt-free.

The answer is B) Debt Snowball.

The Debt Snowball method leverages behavioral psychology by providing quick wins that build momentum. As each small debt is paid off, the payment amount can be applied to the next smallest debt, creating a "snowball" effect. This approach is particularly effective for people who need visible progress to stay motivated. The psychological benefit of seeing debts disappear can be more powerful than the mathematical savings of the avalanche method.

Debt Snowball: Pay smallest debts first for psychological wins

Debt Avalanche: Pay highest interest debts first for maximum savings

Psychological Momentum: Motivation gained from visible progress

• Debt snowball focuses on balance size, not interest rate

• Provides quick wins for motivation

• May cost more in total interest

• List debts from smallest to largest balance

• Make minimum payments on all debts

• Apply extra money to smallest debt first

• Confusing snowball with avalanche method

• Not making minimum payments on all debts

• Taking on new debt while eliminating old debt

Explain what debt-to-income ratio is, why it's important for becoming debt-free, and provide a calculation example. What is considered a healthy ratio for debt elimination?

Debt-to-Income Ratio Definition: DTI is calculated by dividing your total monthly debt payments by your gross monthly income and multiplying by 100%. It represents the percentage of your income that goes toward debt payments.

Formula: DTI = (Total Monthly Debt Payments ÷ Gross Monthly Income) × 100%

Example: If your monthly debt payments total $1,500 and your gross monthly income is $5,000, your DTI would be (1,500 ÷ 5,000) × 100% = 30%.

Importance: DTI is crucial for debt elimination because it indicates how much of your income is tied up in debt. A lower DTI means more money is available for debt repayment. Lenders also use DTI to assess creditworthiness.

Healthy Ratio: For debt elimination, a DTI below 20% is ideal. Ratios between 20-36% are manageable but indicate significant debt burden. Ratios above 40% are considered dangerous and require immediate attention.

DTI is a critical metric because it reveals your financial capacity to take on additional debt or, conversely, your ability to eliminate existing debt. A high DTI means most of your income is already committed to debt payments, leaving little room for extra payments. Monitoring DTI during your debt elimination journey helps track progress and ensures you're moving toward financial health.

Debt-to-Income Ratio (DTI): Percentage of income going to debt payments

Gross Monthly Income: Income before taxes and deductions

Healthy DTI: Below 20% for debt elimination

• DTI should be below 20% for effective debt elimination

• Calculate using gross, not net income

• Include all monthly debt payments

• Track DTI monthly during debt elimination

• Aim to reduce DTI below 20% as quickly as possible

• Use DTI to measure progress

• Calculating with net instead of gross income

• Forgetting to include all debt payments

• Not tracking DTI over time

Sarah has $30,000 in debt consisting of a $10,000 credit card at 18% interest, a $15,000 car loan at 6% interest, and a $5,000 personal loan at 12% interest. Her monthly income is $4,500, and expenses are $3,200. She can allocate $800 per month to debt payments. Which payoff strategy should Sarah choose, and what would her estimated timeline be to become debt-free?

Debt Analysis: Sarah has three debts with different balances and interest rates. Her disposable income is $1,300 ($4,500 - $3,200), with $800 allocated to debt payments.

Strategy Recommendation: For Sarah, the Debt Avalanche method would be more financially efficient since she has a high-interest credit card (18%) that costs more in interest than the other debts combined.

Avalanche Approach: Pay the credit card first (highest interest), then the personal loan (12%), then the car loan (6%). This minimizes total interest paid.

Timeline Estimate: Using the avalanche method with $800 monthly payments, Sarah could eliminate her debt in approximately 3.5-4 years, saving thousands in interest compared to the snowball method.

Alternative: If Sarah prefers psychological wins, she could use the snowball method (pay $5,000 personal loan first), but this would cost more in interest.

This example illustrates the trade-off between mathematical efficiency and psychological motivation. Sarah's situation shows how the avalanche method can save significant money in interest payments. However, if Sarah struggles with motivation, the snowball method might be more effective despite the higher interest costs. The key is choosing a strategy that matches both the financial situation and the person's behavioral tendencies.

Debt Avalanche: Pay highest interest rate debts first

Debt Snowball: Pay smallest balance debts firstDisposable Income: Income after essential expenses

• Choose strategy based on both finances and personality

• Avalanche saves more money in interest

• Snowball provides psychological wins

• List all debts with balances and interest rates

• Calculate potential interest savings

• Choose method that fits your personality

• Not considering both financial and psychological factors

• Choosing a strategy that doesn't match your personality

• Forgetting to account for all debts and their terms

Mark has $20,000 in credit card debt at 19% interest and $3,000 in savings. He's considering using his savings to pay down debt but is worried about emergencies. What should Mark do, and what is the recommended approach for balancing debt elimination with emergency preparedness?

Recommended Approach: Mark should keep $1,000-$2,000 as a starter emergency fund while aggressively paying down the high-interest credit card debt. Here's why:

Rationale: With 19% interest on credit card debt, Mark is losing money quickly. However, having no emergency fund risks creating new debt if unexpected expenses arise. The balanced approach is:

1. Keep $1,000-2,000 in savings: Covers minor emergencies without derailing debt progress

2. Pay minimums on other debts: Avoid penalties and negative credit impact

3. Apply all extra money to high-interest debt: Eliminate the most expensive debt first

4. Build full emergency fund after debt elimination: Once debt-free, build 3-6 months of expenses

This approach prevents the debt cycle that occurs when emergencies force new borrowing.

This scenario highlights the balance between urgency (high-interest debt) and preparedness (emergency fund). The key insight is that debt elimination is not just about math—it's about building sustainable financial habits. Having a small emergency fund prevents derailment of debt elimination plans when unexpected expenses occur. This is why financial experts often recommend a starter emergency fund even while paying down debt.

Starter Emergency Fund: Small amount (typically $1,000-2,000) for minor emergencies

Full Emergency Fund: 3-6 months of expenses for major emergencies

Debt Cycle: Pattern of accumulating debt to handle emergencies

• Maintain starter emergency fund while paying debt

• Prioritize high-interest debt elimination

• Build full emergency fund after becoming debt-free

• Start with $1,000 emergency fund while paying debt

• Focus on highest interest debt first

• Increase emergency fund after debt elimination

• Going to extremes (either no emergency fund or full fund while in debt)

• Using emergency fund for non-emergencies

• Not rebuilding emergency fund after debt elimination

Which of the following is the MOST effective approach for generating extra income to accelerate debt elimination?

Selling unused items and starting a small side business is the most effective approach. This strategy provides immediate cash from selling items that aren't needed and creates a sustainable source of additional income. Unlike gambling, borrowing, or asking friends, this approach generates real money without creating additional financial risk. Side businesses like freelancing, tutoring, or gig economy work can provide steady income that can be directed toward debt elimination.

The answer is B) Selling unused items and starting a small side business.

Generating extra income for debt elimination requires reliable, sustainable methods that don't create additional financial risk. Selling unused items provides immediate cash while decluttering, and starting a side business creates ongoing income. Both approaches align with the principle of living below your means while generating extra money for debt elimination. Risky approaches like gambling or borrowing money can worsen the debt situation.

Side Income: Additional earnings beyond primary employment

Sustainable Income: Reliable source of additional money

Financial Risk: Possibility of worsening financial situation

• Choose income methods that don't create additional debt

• Focus on reliable, sustainable income sources

• Direct all extra income toward debt elimination

• Sell items you haven't used in 6+ months

• Leverage skills for freelance work

• Use gig economy platforms for flexible income

• Pursuing risky income methods

• Not directing extra income toward debt

• Creating additional debt while trying to eliminate debt

FAQ

Q: How long does it typically take to become debt-free using these strategies?

A: The time to become debt-free varies greatly depending on the amount of debt, interest rates, and how much extra money you can put toward debt payments. However, most people following a disciplined debt elimination plan can become debt-free within 2-5 years. The key factors are:

• Amount of debt: Larger amounts take longer

• Interest rates: Higher rates slow progress

• Monthly payments: More money accelerates payoff

• Strategy chosen: Avalanche method may be faster

Many people see significant progress within the first year, with complete debt elimination occurring within 2-5 years. The most important factor is consistency and commitment to the plan.

Q: Should I stop contributing to retirement accounts while paying off debt?

A: Generally, you should continue contributing to retirement accounts up to the employer match if available. Here's the recommended approach:

1. Contribute enough to get employer match: This is free money

2. Focus extra money on debt elimination: Pay minimums on all debts, then attack the target debt

3. Resume full contributions after debt elimination: Once debt-free, maximize retirement savings

Skipping retirement contributions entirely can cause you to miss out on employer contributions and compound growth. However, high-interest debt (above 8-10%) should generally take priority over retirement contributions beyond the employer match.