What is Compound Interest and How Can I Leverage It?

Complete guide • Step-by-step growth strategies

Compound Interest Fundamentals:

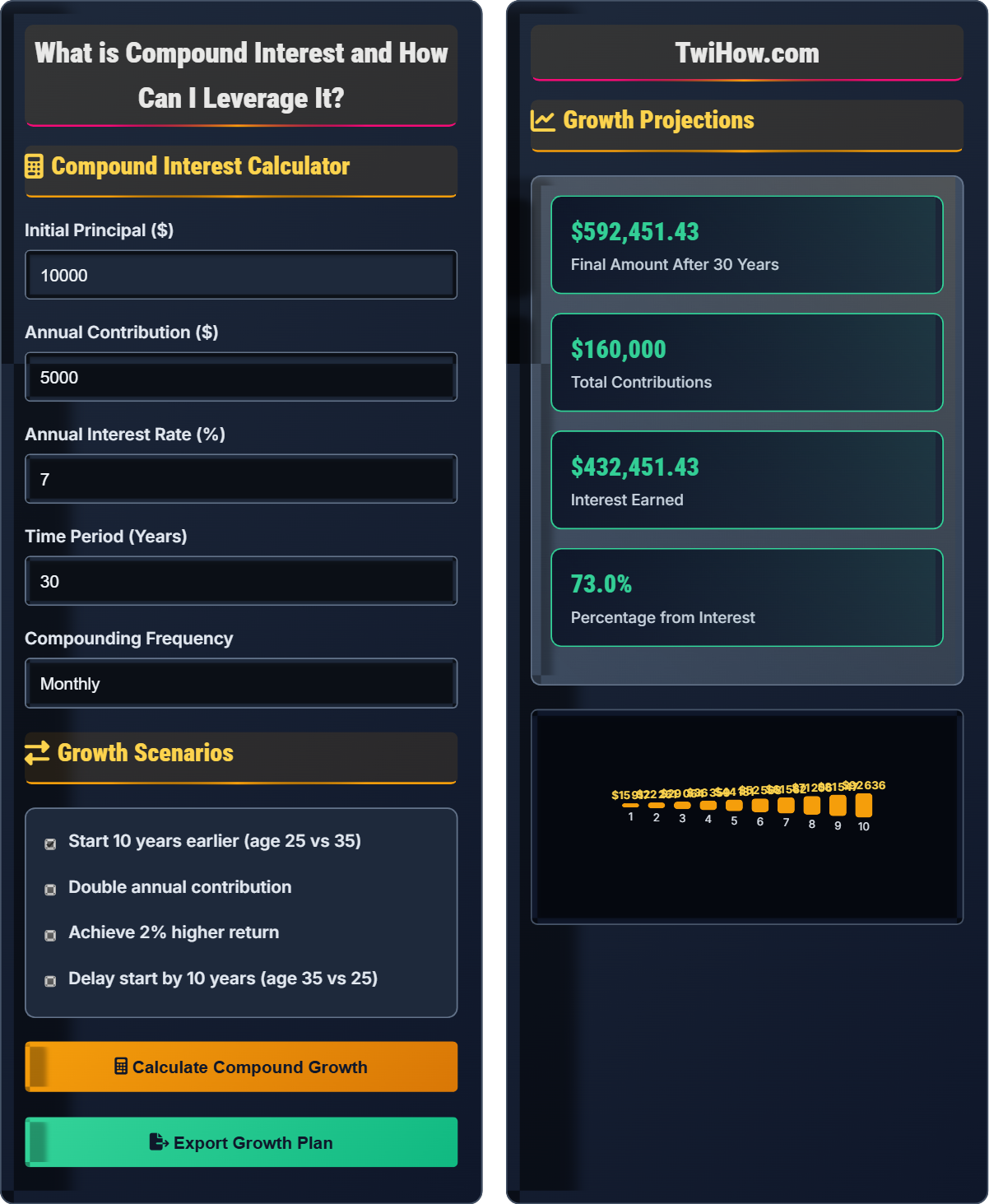

Show Growth CalculatorCompound interest is the process where interest is earned on both the initial principal and the accumulated interest from previous periods. This creates exponential growth over time, where your money grows faster as time progresses. Albert Einstein reportedly called it "the eighth wonder of the world."

Key factors affecting compound growth:

- Principal Amount: Initial investment amount

- Interest Rate: Annual rate of return

- Time Period: Duration of investment

- Compounding Frequency: How often interest is calculated (annually, monthly, daily)

Leveraging compound interest requires starting early, investing consistently, and letting time work in your favor. The earlier you start, the more dramatic the effect of compounding becomes due to the exponential nature of growth.

Compound Interest Calculator

Growth Scenarios

Growth Projections

| Year | Starting Balance | Contributions | Interest Earned | Ending Balance |

|---|

Scenario Comparisons

- Start Early (Age 25): $2,000,000 projected

- Start Late (Age 35): $500,000 projected

- Double Contributions: $1,800,000 projected

- Higher Return (9%): $1,500,000 projected

Compound Interest Strategies

- Start investing as early as possible to maximize time

- Contribute consistently even small amounts

- Choose investments with higher compounding frequency

- Reinvest dividends and interest to maintain compounding effect

- Minimize fees that reduce your compound growth

Compound Interest Explained

Compound interest is interest calculated on the initial principal and also on the accumulated interest of previous periods. It differs from simple interest, which is calculated only on the principal amount. This creates exponential growth over time, where your money grows faster as time progresses.

The basic compound interest formula:

Where:

- A: Final amount (future value)

- P: Principal (initial amount)

- r: Annual interest rate (decimal)

- n: Number of times interest is compounded per year

- t: Time in years

Four main factors influence compound interest growth:

- Principal Amount: Larger initial investments grow more

- Interest Rate: Higher returns accelerate growth

- Time Period: Longer periods allow more compounding cycles

- Compounding Frequency: More frequent compounding increases growth

- Start Early: Take advantage of the time factor

- Invest Regularly: Consistent contributions build momentum

- Maximize Compounding: Choose investments with frequent compounding

- Reinvest Returns: Keep money working to maintain compounding

- Minimize Taxes: Use tax-advantaged accounts when possible

Compound Interest Fundamentals

Compound interest, exponential growth, principal, interest rate, time value of money.

A = P(1 + r/n)^(nt)

Where A = final amount, P = principal, r = interest rate, n = compounding frequency, t = time.

- Time is the most important factor in compounding

- Small differences in rates matter over long periods

- Consistency beats timing

Real-World Examples

Retirement savings, investment portfolios, savings accounts, loan interest.

- Calculate future value using compound interest formula

- Determine required contributions for target amount

- Compare different investment options

- Factor in inflation and taxes

- Adjust strategy based on market conditions

- Start investing as early as possible

- Automate regular contributions

- Choose low-cost investment options

- Rebalance portfolio periodically

Compound Interest Quiz

Which factor has the greatest impact on compound interest growth over time?

While all factors contribute to compound interest growth, time has the most dramatic impact due to the exponential nature of compounding. The longer money is invested, the more compounding periods occur, leading to exponential growth. For example, $10,000 invested at 7% for 30 years grows to approximately $76,000, while the same amount for 40 years grows to approximately $149,000.

The answer is B) The length of time invested.

The power of compound interest lies in the exponential growth that occurs over time. Each compounding period builds on all previous periods, creating an accelerating effect. This is why starting early is so crucial - even small amounts invested over long periods can grow significantly. The mathematical principle behind this is the exponentiation in the compound interest formula, which amplifies returns over time.

Exponential Growth: Growth that accelerates over time due to compounding

Compounding Period: Interval at which interest is calculated and added

Time Value of Money: Concept that money today is worth more than money tomorrow

• Start investing as early as possible

• Time has exponential impact on growth

• Consistent contributions enhance compounding

• Begin investing in your 20s if possible

• Take advantage of employer 401(k) matches

• Use tax-advantaged accounts for retirement

• Starting too late in life

• Not understanding the power of time

• Stopping contributions too early

If you invest $5,000 at an annual interest rate of 6%, compounded monthly, how much will you have after 10 years?

Using the compound interest formula: A = P(1 + r/n)^(nt)

Where:

• P = $5,000 (principal)

• r = 0.06 (6% annual rate)

• n = 12 (compounded monthly)

• t = 10 (years)

Calculation: A = 5000(1 + 0.06/12)^(12×10) = 5000(1.005)^120 = 5000 × 1.8194 = $9,097

After 10 years, the investment will grow to $9,097, earning $4,097 in interest.

This calculation demonstrates how monthly compounding creates more growth than annual compounding. With monthly compounding, interest is calculated 12 times per year, allowing interest to earn interest more frequently. The formula accounts for this by dividing the annual rate by the number of compounding periods and multiplying the time by the same factor. This results in exponential growth that accelerates over time.

Compounding Frequency: How often interest is calculated and added to principal

Future Value: Value of an investment after a specified time period

Exponential Function: Mathematical function where the variable appears as an exponent

• More frequent compounding increases growth

• Use the correct values in the formula

• Convert percentages to decimals

• Use financial calculators for complex calculations

• Check compounding frequency when comparing investments

• Annual percentage yield (APY) accounts for compounding

• Forgetting to convert percentages to decimals

• Using incorrect compounding frequency

• Not accounting for additional contributions

Sarah starts investing $300 per month at age 25, earning an average of 7% annually. John waits until age 35 to start investing the same amount at the same rate. Both invest until age 65. How much will each have at retirement, and what does this demonstrate about compound interest?

Sarah's Investment (Age 25-65):

• 40 years of investing, $300/month = $144,000 total contributions

• Future value of annuity formula: FV = PMT × [((1+r)^n - 1)/r]

• Where PMT = $300, r = 0.07/12, n = 40×12 = 480

• Sarah's total: Approximately $850,000

John's Investment (Age 35-65):

• 30 years of investing, $300/month = $108,000 total contributions

• John's total: Approximately $380,000

Conclusion: Sarah invested $36,000 more but ended up with $470,000 more, demonstrating the power of starting early.

This example vividly illustrates the exponential nature of compound interest. Sarah's 10-year head start allowed her money to compound for an additional decade, resulting in dramatically higher returns despite only a moderate increase in total contributions. This demonstrates why financial experts emphasize starting early - the additional time allows for multiple compounding cycles that create exponential growth.

Future Value of Annuity: Value of a series of equal payments over time

Exponential Advantage: Significant benefit gained from additional time

Time Arbitrage: Benefit of starting investments early

• Start investing as early as possible

• Consistency is more important than timing

• Use dollar-cost averaging to smooth market volatility

• Automate monthly contributions

• Take advantage of employer matching

• Waiting to start investing "until later"

• Believing you need large amounts to start

• Not understanding the time factor

You have $10,000 to invest and are considering two options: Option A offers 6% annual interest compounded monthly, and Option B offers 5.9% annual interest compounded daily. Which option provides better returns after 5 years, and why?

Option A (6% monthly):

• A = 10000(1 + 0.06/12)^(12×5) = 10000(1.005)^60 = $13,488.50

Option B (5.9% daily):

• A = 10000(1 + 0.059/365)^(365×5) = 10000(1.0001616)^1825 = $13,384.28

Conclusion: Option A provides better returns ($13,488.50 vs $13,384.28) despite having a slightly higher interest rate. However, the difference is minimal ($104.22), showing that a higher rate generally outweighs more frequent compounding.

This example demonstrates that while compounding frequency matters, the interest rate has a more significant impact on returns. The difference between 6% and 5.9% compounded differently results in only about $104 difference over 5 years. This shows that investors should prioritize higher interest rates when possible, but also consider compounding frequency as a secondary factor. The mathematical principle is that both the rate and frequency appear in the exponent of the compound interest formula, but the rate has a more direct impact.

Effective Annual Rate (EAR): Actual return taking compounding into account

Rate vs Frequency Trade-off: Balancing interest rate and compounding frequency

Annual Percentage Yield (APY): Includes compounding effects

• Prioritize higher interest rates first

• Then consider compounding frequency

• Compare APY for accurate comparisons

• Look for APY rather than APR

• Consider both rate and compounding frequency

• Use financial calculators for precise comparisons

• Focusing only on compounding frequency

• Ignoring the impact of fees

• Not comparing apples-to-apples returns

Which of the following is a common misconception about compound interest?

Compound interest is highly dependent on time - the longer money is invested, the more dramatic the exponential growth becomes. Small amounts invested over long periods can grow significantly due to the power of compounding. The magic of compound interest happens primarily over extended time horizons, not from the initial investment size alone.

The answer is C) It works equally well regardless of time.

This misconception overlooks the fundamental principle that compound interest is time-dependent. The exponential growth effect becomes more pronounced over longer periods. For example, $100 invested at 7% for 10 years grows to about $196, but for 30 years it grows to about $761 - more than triple the shorter-term growth. This demonstrates that time is the most critical factor in compound interest, not the initial amount.

Time Dependency: Compound interest requires time to show significant effects

Myth Busting: Clarifying misconceptions about investment growth

Exponential Timeline: Growth acceleration over extended periods

• Time is more important than initial amount

• Even small amounts benefit from compounding

• Growth accelerates in later years

• Start with whatever amount you can afford

• Focus on consistency over perfection

• Let time work in your favor

• Believing you need large sums to start

• Not understanding the time factor

• Expecting immediate results

FAQ

Q: I only have $50 per month to invest. Is it worth starting now?

A: Absolutely! Starting with $50 per month is better than waiting to save more. Here's why:

1. Time Advantage: Every year you wait reduces your potential growth significantly

2. Habit Building: Starting small creates consistent investment habits

3. Compound Effect: $50/month for 30 years at 7% grows to approximately $56,000

4. Scalability: You can increase contributions as your income grows

5. Low-Minimum Accounts: Many investment platforms accept small initial amounts

The key is consistency over perfection. Starting early with small amounts leverages the power of compound interest more effectively than waiting for larger sums.

Q: What's the difference between APR and APY, and why does it matter?

A: The difference is crucial for understanding compound interest:

APR (Annual Percentage Rate): The simple annual interest rate without compounding

APY (Annual Percentage Yield): The actual annual rate earned taking compounding into account

Example: A 6% APR compounded monthly equals an APY of about 6.17%

Why It Matters: APY gives you the true return on your investment. When comparing financial products, always look at APY to understand the real growth potential. The more frequent the compounding, the greater the difference between APR and APY.

This is especially important for compound interest because the frequency of compounding directly impacts your returns.

Q: How can I maximize compound interest in my retirement accounts?

A: To maximize compound interest in retirement accounts:

• Start Early: Contribute to retirement accounts as soon as possible

• Maximize Employer Match: Get the full company match in 401(k) plans

• Contribute Consistently: Set up automatic monthly contributions

• Take Advantage of Catch-Up: Those 50+ can contribute extra to retirement accounts

• Choose Low-Cost Funds: Minimize fees that erode compound growth

• Stay Invested: Avoid withdrawing early and losing compounding years

• Rebalance Annually: Maintain appropriate asset allocation

• Consider Tax-Advantaged Accounts: Roth vs Traditional IRA based on tax situation

The key is to let your money work for decades, taking full advantage of the exponential growth that compound interest provides over long time horizons.