Index Fund Investing: Complete Guide

Passive investing • Low-cost • Portfolio diversification

Index Fund Fundamentals:

Calculate Index Fund ReturnsIndex fund investing is a passive investment strategy that aims to track the performance of a specific market index, such as the S&P 500. Instead of actively picking individual stocks, index funds hold all or a representative sample of the securities in an index, providing instant diversification and low costs.

Low Cost Advantage: Index funds typically have expense ratios of 0.05-0.20%, compared to 1-2% for actively managed funds.

Key benefits of index fund investing:

- Instant Diversification: Holds hundreds or thousands of securities in one fund

- Low Fees: Minimal management costs compared to active funds

- Market-Matching Returns: Historically delivers strong long-term performance

- Transparency: Holdings and strategy are clearly disclosed

- Accessibility: Available through most brokerages with low minimums

Index fund investing is ideal for most investors seeking long-term wealth building with minimal effort and low costs. The strategy works best when combined with regular contributions and a long-term investment horizon.

Index Fund Return Calculator

Investment Options

Index Fund Performance

| Feature | Index Fund | Active Fund |

|---|---|---|

| Expense Ratio | 0.10% | 1.50% |

| Management Style | Passive | Active |

| Goal | Track Index | Beat Index |

| Turnover | Low | High |

| Tax Efficiency | High | Medium |

For most investors, a simple allocation works well:

- 70% Total Stock Market Index

- 20% International Index

- 10% Bond Index

Adjust allocation based on age and risk tolerance:

- 20s-30s: 90% stocks, 10% bonds

- 40s-50s: 70% stocks, 30% bonds

- 60s+: 50% stocks, 50% bonds

Understanding Index Fund Investing

The future value of an index fund investment with regular contributions is calculated as:

Where FV = Future Value, PV = Present Value, r = net return rate (gross return - expense ratio), n = number of years, PMT = annual contribution.

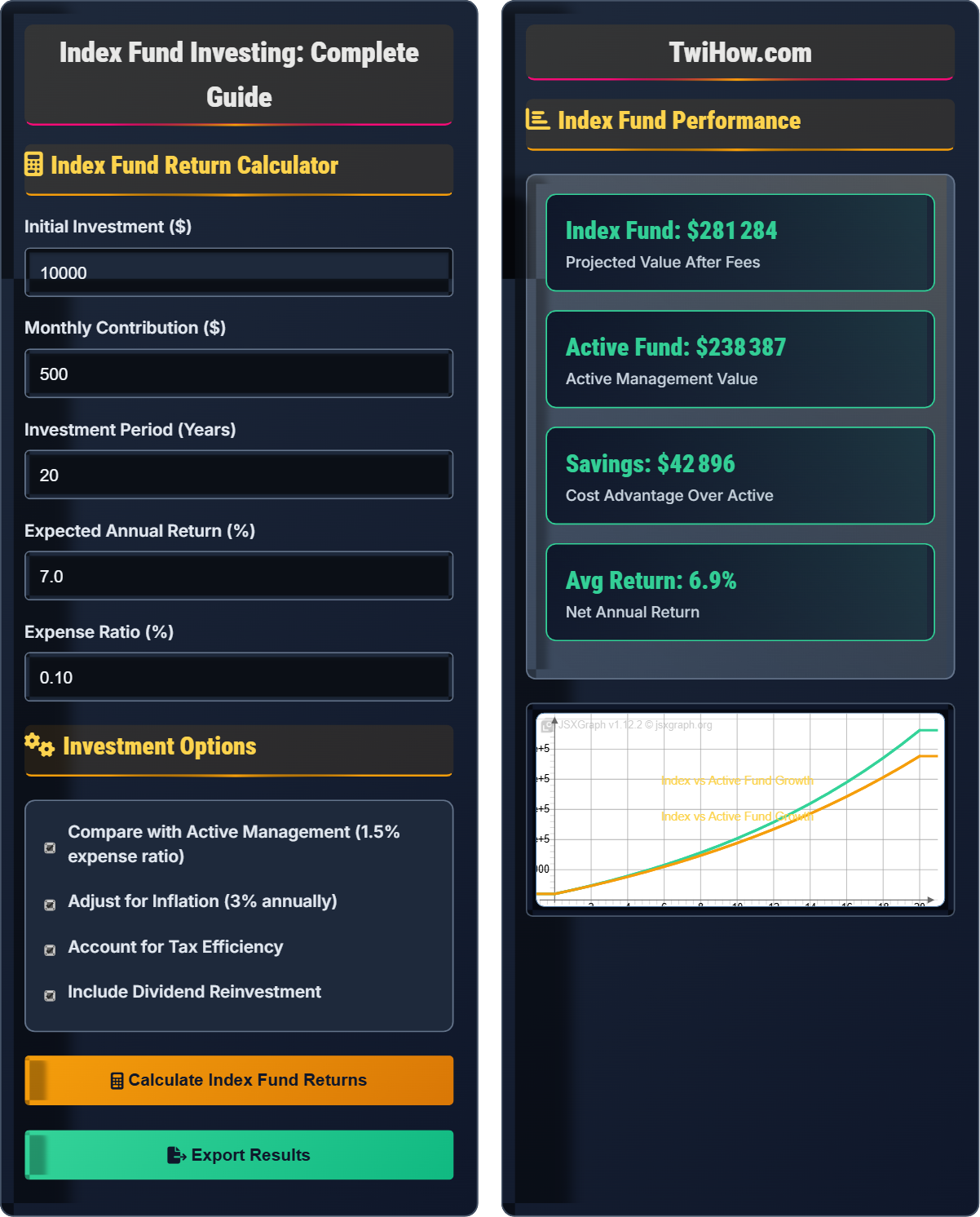

The cost advantage of index funds over active funds is significant over time:

For example, a 1.4% difference on $100,000 over 20 years equals $280,000 in additional costs for active management.

Effective approaches to maximize index fund benefits:

- Buy and Hold: Maintain investments through market ups and downs

- Dollar-Cost Averaging: Invest fixed amounts regularly regardless of market conditions

- Asset Allocation: Diversify across different asset classes

- Minimize Taxes: Use tax-advantaged accounts when possible

- Keep Costs Low: Choose funds with the lowest expense ratios

- Rebalance Annually: Maintain target allocation over time

Index Fund Basics

Index funds, passive investing, expense ratios, market tracking, diversification, dollar-cost averaging.

FV = PV(1+r)^n + PMT[((1+r)^n - 1)/r]

Where FV = Future Value, PV = Present Value, r = net return rate, n = number of periods, PMT = periodic payment.

- Choose funds with expense ratios below 0.20%

- Diversify across multiple asset classes

- Rebalance portfolio annually

Investment Strategies

Asset allocation, dollar-cost averaging, rebalancing, tax-efficient investing, target-date funds.

- Young investors: Focus on stock-heavy portfolios

- Middle-aged: Gradually shift toward bonds

- Near retirement: Emphasize preservation of capital

- Retired: Focus on income generation

- Asset allocation should become more conservative with age

- Consider both Traditional and Roth accounts

- Minimize investment fees

- Review and adjust strategy regularly

Index Fund Learning Quiz

What is the typical expense ratio range for a low-cost index fund compared to an actively managed fund?

Low-cost index funds typically have expense ratios ranging from 0.05% to 0.20%, while actively managed funds typically have expense ratios from 1.0% to 2.0% or higher. The lower fees of index funds represent a significant cost advantage over time. For example, a 1.5% difference on a $100,000 investment over 30 years could result in more than $300,000 in additional costs for the active fund.

The answer is B) Index: 0.05-0.20%, Active: 1.0-2.0%.

The expense ratio is a critical factor in investment returns. Even small differences in fees can have a massive impact over long periods due to compound growth. Index funds are cheaper because they don't require expensive research teams or frequent trading to beat the market. This cost advantage translates directly to higher returns for investors over time.

Expense Ratio: Annual fee expressed as a percentage of fund assets

Active Management: Fund manager attempts to beat market returns

Passive Management: Fund tracks a market index

• Always look for expense ratios below 0.20%

• Small differences in fees compound over time

• Lower fees mean higher net returns

• Compare expense ratios across similar funds

• Look for funds with ratios below 0.10%

• Consider total cost including transaction fees

• Not paying attention to expense ratios

• Confusing expense ratios with other fees

• Overlooking the impact of fees over time

Explain what dollar-cost averaging is, why it's beneficial for index fund investing, and provide a practical example of how it works.

Dollar-Cost Averaging (DCA) Definition: DCA is an investment strategy where you invest a fixed amount of money at regular intervals (monthly or quarterly) regardless of market conditions. Instead of investing a lump sum all at once, you spread your investments over time.

How it Works: When prices are low, your fixed investment buys more shares. When prices are high, it buys fewer shares. Over time, this evens out the purchase price.

Example: If you invest $500 monthly in an index fund for 3 months: Month 1: Price $50, you buy 10 shares Month 2: Price $40, you buy 12.5 shares Month 3: Price $60, you buy 8.33 shares Average purchase price: ~$48.48 vs. current price of $60

Benefits: DCA removes emotion from investing, reduces timing risk, and is ideal for index funds since you're building long-term positions in broad market indices without trying to time the market.

DCA is particularly effective with index funds because it aligns with the passive investing philosophy. Since index funds are meant to be held long-term, regular contributions through DCA help smooth out market volatility. This strategy is especially valuable for new investors who might be nervous about market timing.

Dollar-Cost Averaging: Investing fixed amounts at regular intervals

Timing Risk: Risk of investing at market peaks

Lump Sum: Investing all money at once

• Invest consistently regardless of market conditions

• Works best for long-term investments

• Reduces emotional decision-making

• Set up automatic monthly investments

• Use payroll deduction if available

• Combine with index funds for best results

• Stopping contributions during market downturns

• Trying to time the market instead of DCA

• Not maintaining consistency

Sarah is 30 years old and wants to start investing for retirement. She has $50,000 in savings and can invest $800 per month. She's considering a 70% stock and 30% bond allocation. Recommend specific index funds for her portfolio and explain why this allocation is appropriate for her age.

Fund Recommendations:

Stock Portion (70% = $35,000 + $560/month): - Vanguard Total Stock Market Index Fund (VTSMX) or ETF (VTI) - Expense ratio: 0.04% - Tracks: Broad U.S. stock market

Bond Portion (30% = $15,000 + $240/month): - Vanguard Total Bond Market Index Fund (VBTLX) or ETF (BND) - Expense ratio: 0.03% - Tracks: Broad U.S. bond market

Allocation Justification: At age 30, Sarah has a 35-year investment horizon until retirement at 65. This allows her to take on more risk for higher potential returns. The 70/30 split provides: 1. Growth potential through stock exposure 2. Stability through bond allocation 3. Diversification across asset classes 4. Low costs with index funds

Strategy: Set up automatic monthly contributions to maintain the target allocation over time.

This allocation is appropriate for Sarah's age because it balances growth potential with some stability. Young investors can afford to take more risk since they have time to recover from market downturns. The 70/30 split allows for significant growth while providing some protection. As she ages, she can gradually shift toward more conservative allocations.

Asset Allocation: Distribution of investments across asset classes

Investment Horizon: Time period for investment

Risk Tolerance: Ability to withstand market volatility

• Young investors can take more risk

• Diversify across asset classes

• Choose low-cost index funds

• Consider target-date funds for simplicity

• Rebalance annually to maintain allocation

• Use tax-advantaged accounts first

• Being too conservative at a young age

• Not diversifying properly

• Choosing high-cost funds

Mark has a $100,000 portfolio allocated 70% stocks and 30% bonds. After a strong stock market year, his allocation has shifted to 80% stocks and 20% bonds. Explain why rebalancing is important and provide a strategy for Mark to return to his target allocation.

Why Rebalancing is Important:

1. Manages Risk: Without rebalancing, Mark's portfolio has become more aggressive than intended, exposing him to higher volatility.

2. Maintains Target Allocation: Rebalancing ensures the portfolio aligns with his risk tolerance and investment goals.

3. Disciplined Investing: Forces him to sell high (stocks) and buy low (bonds).

Rebalancing Strategy:

Current holdings: $80,000 stocks, $20,000 bonds

Target allocation: $70,000 stocks, $30,000 bonds

Mark should sell $10,000 of stocks and buy $10,000 of bonds to return to his 70/30 target. This can be done gradually over several months or all at once.

Alternative Strategy: Direct future contributions to the underweighted asset class (bonds) until target allocation is restored.

Rebalancing is crucial for maintaining your intended risk level. Markets naturally cause allocations to drift over time. Without rebalancing, your portfolio can become significantly more aggressive or conservative than planned. Regular rebalancing helps ensure your portfolio matches your risk tolerance and investment timeline.

Rebalancing: Adjusting portfolio to maintain target allocation

Target Allocation: Desired percentage in each asset class

Asset Drift: Change in allocation due to market movements

• Rebalance at least annually

• Consider tax implications in taxable accounts

• Rebalance when allocation deviates by more than 5%

• Use new contributions to rebalance toward targets

• Rebalance tax-advantaged accounts first

• Consider threshold-based rebalancing

• Never rebalancing and letting allocation drift

• Rebalancing too frequently (transaction costs)

• Not considering tax consequences in taxable accounts

What does it mean when an index fund "tracks" a market index?

When an index fund "tracks" a market index, it means the fund holds all or a representative sample of the securities included in that index. For example, an S&P 500 index fund would hold shares of all 500 companies in the S&P 500 in proportion to their weighting in the index. The fund's goal is to match the index's performance as closely as possible, minus fees. This is accomplished through passive management, not active trading or stock selection.

The answer is B) The fund holds all or a representative sample of securities in the index.

Index tracking is the fundamental principle of passive investing. Instead of trying to outperform the market, index funds aim to mirror market performance. This approach eliminates the need for expensive research teams and frequent trading, resulting in lower costs for investors. The tracking process is mechanical and systematic, ensuring broad market exposure.

Index Tracking: Holding securities to match index performance

Passive Management: No active stock selection

Market Exposure: Access to broad market performance

• Index funds don't try to beat the market

• They aim to match market returns

• Holdings mirror the index composition

• Look for funds with low tracking error

• Check if fund holds all index components

• Monitor tracking performance over time

• Thinking index funds try to beat the market

• Confusing active with passive management

• Not understanding the tracking mechanism

FAQ

Q: Isn't it better to pick individual stocks or hire an advisor to beat the market?

A: Research consistently shows that most actively managed funds fail to beat their benchmark indices over long periods. After fees, only about 15-20% of actively managed funds outperform their benchmarks over 10-year periods. Here's why index funds often perform better:

1. Lower Costs: Index funds have significantly lower expense ratios

2. Consistent Performance: Market returns are predictable over long periods

3. No Manager Risk: No worry about changing fund managers

4. Broad Diversification: Instant exposure to hundreds or thousands of companies

While some skilled managers do outperform, identifying them ahead of time is extremely difficult. Index funds provide market returns at a fraction of the cost, which historically leads to better outcomes for most investors.

Q: How do I know if index fund investing is right for my financial situation?

A: Index fund investing is suitable for most investors, especially those with these characteristics:

• Long-term horizon: At least 5-10 years until you need the money

• Comfortable with market volatility: Can stay invested during market downturns

• Wants to keep costs low: Prefers minimizing fees and expenses

• Seeks diversification: Wants broad market exposure

• Not interested in stock picking: Prefers simple, systematic approach

However, if you have a short-term time horizon (less than 5 years), need stable returns, or want to invest in specific sectors/regions, other strategies might be more appropriate. Index investing works best when combined with a solid financial plan and appropriate asset allocation.