Roth vs Traditional IRA: Complete Guide

Tax benefits, contribution limits, withdrawal rules

IRA Fundamentals:

Compare IRAsIndividual Retirement Accounts (IRAs) are tax-advantaged investment accounts designed to encourage retirement savings. There are two main types: Roth IRAs and Traditional IRAs, each offering different tax benefits at different stages of your financial journey.

Traditional IRA: Contributions are tax-deductible now, but withdrawals are taxed later.

Roth IRA: Contributions are made with after-tax dollars, but qualified withdrawals are tax-free.

Key differences:

- Tax Treatment: Traditional deducts contributions, Roth taxes them upfront

- Withdrawal Rules: Traditional has required minimum distributions, Roth doesn't

- Income Limits: Roth has income restrictions, Traditional doesn't

- Age Limits: Traditional allows contributions until age 72, Roth has no age limit

The choice between Roth and Traditional depends on your current tax bracket, expected future tax bracket, and retirement goals. If you expect to be in a higher tax bracket in retirement, Roth is often preferred. If you expect to be in a lower tax bracket, Traditional may be better.

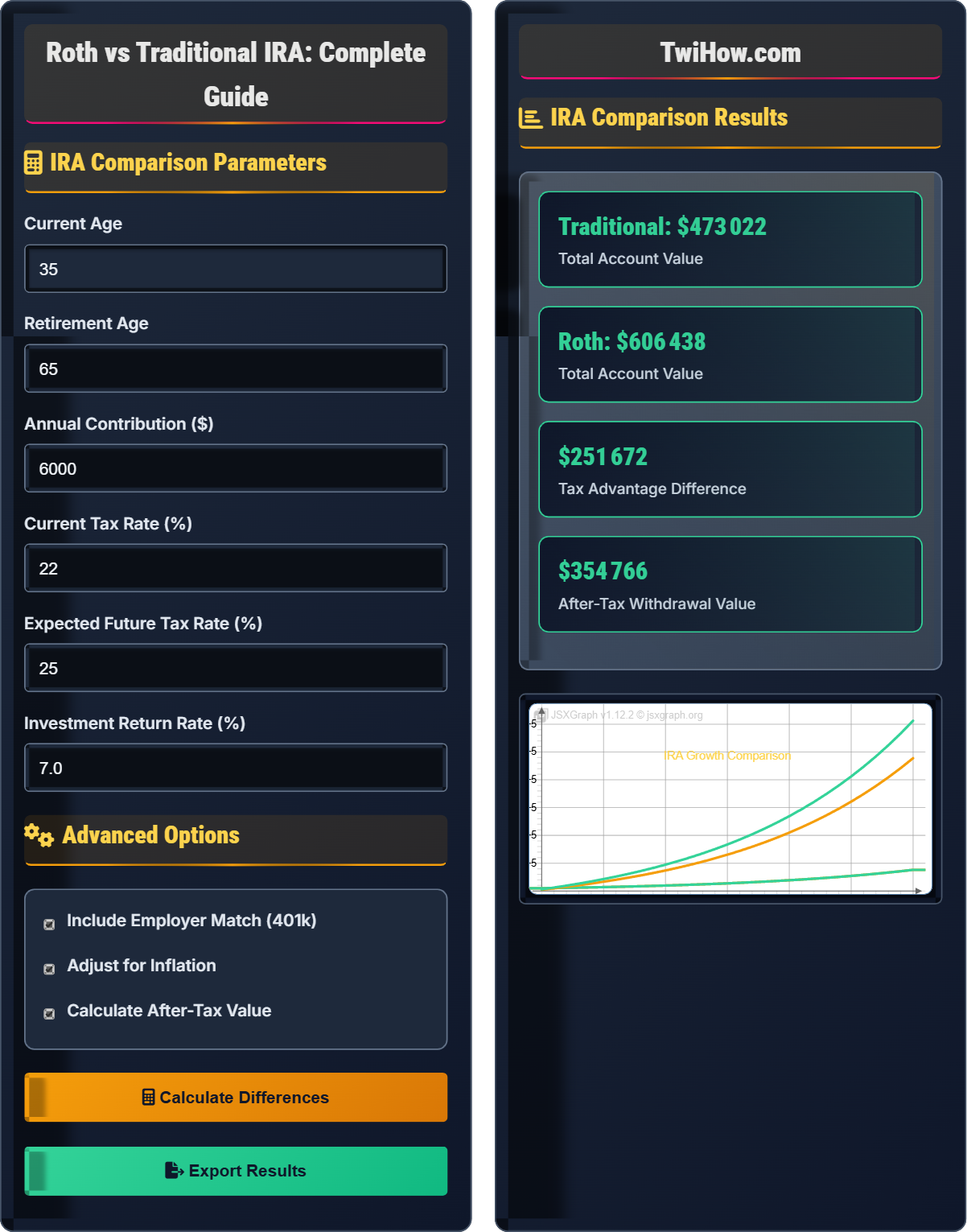

IRA Comparison Parameters

Advanced Options

IRA Comparison Results

| Feature | Traditional IRA | Roth IRA |

|---|---|---|

| Contribution Tax Deduction | Yes | No |

| Tax-Free Growth | Yes | Yes |

| Tax-Free Withdrawals | No | Yes (qualified) |

| Income Limits | No | Yes |

| Required Minimum Distributions | Yes | No |

Contributions are tax-deductible in the year they're made, reducing your taxable income. Investment growth is tax-deferred until withdrawal. Withdrawals are taxed as ordinary income. Required minimum distributions begin at age 73.

Contributions are made with after-tax dollars, so there's no immediate tax deduction. Investment growth is tax-free. Qualified withdrawals (age 59½ and account open for 5 years) are completely tax-free. No required minimum distributions during owner's lifetime.

Understanding IRA Types Explained

An Individual Retirement Account (IRA) is a tax-advantaged investment account that individuals can use to save and invest for retirement. IRAs offer significant tax benefits compared to regular investment accounts, making them essential tools for retirement planning.

Traditional IRA: Contributions reduce taxable income, withdrawals are taxed

Roth IRA: Contributions are made after tax, withdrawals are tax-free

For Traditional IRA:

For Roth IRA:

Where r = annual return rate, n = number of years invested

Key areas where IRAs play a crucial role:

- Retirement Savings: Primary vehicle for tax-advantaged retirement planning

- Tax Planning: Strategic tool for managing current and future tax liability

- Estate Planning: Roth IRAs can pass tax-free to beneficiaries

- Emergency Backup: Roth contributions can be withdrawn penalty-free

- Spousal Planning: Spousal IRAs for non-working spouses

- Backdoor Strategies: Converting Traditional to Roth for high earners

Annual contribution limits (2023-2024):

- Traditional IRA: $6,500 ($7,500 if 50+)

- Roth IRA: $6,500 ($7,500 if 50+) - subject to income limits

- Combined: You cannot exceed total limits across both types

IRA Fundamentals

Traditional IRA, Roth IRA, tax deferral, tax-free growth, contribution limits, required minimum distributions.

Traditional: (Contribution × Tax Rate) + (Future Growth) - (Withdrawal Tax)

Roth: (Future Growth) - (Contribution Tax) + (Tax-Free Withdrawal)

- Traditional IRA contributions may be deductible

- Roth IRA withdrawals are tax-free if qualified

- Both have annual contribution limits

IRA Comparison

Tax treatment timing, income limits, withdrawal rules, estate planning benefits.

- Current vs expected future tax rate

- Income eligibility for Roth

- Desire for RMD flexibility

- Estate planning considerations

- Higher current tax bracket favors Roth

- Higher future tax bracket favors Roth

- Income limits restrict Roth access

- RMDs required for Traditional after age 73

IRA Learning Quiz

Which statement accurately describes the tax treatment of Traditional and Roth IRAs?

Traditional IRAs allow tax-deductible contributions, meaning you can reduce your taxable income by the amount you contribute (subject to income limits and participation in employer plans). Roth IRAs do not offer tax deductions for contributions since they are made with after-tax dollars. However, qualified withdrawals from Roth IRAs are tax-free.

The answer is B) Traditional allows tax-deductible contributions; Roth does not.

Understanding the timing of tax benefits is fundamental to IRA selection. Traditional IRAs provide an immediate tax benefit by reducing current taxable income, while Roth IRAs provide a future tax benefit by allowing tax-free withdrawals. This "tax deferral vs. tax prepayment" concept is crucial for optimizing retirement savings based on your current and expected future tax situation.

Tax-Deductible: Reduces taxable income in the year of contribution

After-Tax Dollars: Money that has already been taxed

Tax-Free Growth: Investment gains not subject to taxation

• Traditional contributions may be deductible based on income and employer plan participation

• Roth contributions are never deductible

• Both offer tax-free investment growth

• Consider your current vs. future tax bracket when choosing

• Use Traditional if you expect to be in a lower tax bracket in retirement

• Use Roth if you expect to be in a higher tax bracket in retirement

• Assuming Roth contributions are tax-deductible

• Thinking Traditional withdrawals are tax-free

• Ignoring the impact of current tax rate on decision

Explain the differences in Required Minimum Distribution (RMD) rules between Traditional and Roth IRAs. Why are these rules important for retirement planning?

Traditional IRA RMDs: Required beginning at age 73 (as of 2023). You must withdraw a minimum amount each year based on your account balance and life expectancy. Failure to take RMDs results in a 50% penalty on the amount not withdrawn.

Roth IRA RMDs: No RMDs during the original owner's lifetime. Beneficiaries must take RMDs after the owner's death.

Importance for Planning: RMDs affect your tax strategy in retirement. With Traditional IRAs, you lose control over when you pay taxes on those funds. Roth IRAs allow your money to continue growing tax-free, providing more flexibility in retirement. This difference is particularly valuable for estate planning purposes.

RMDs represent one of the most significant differences between Traditional and Roth IRAs. They fundamentally alter the control you have over your retirement assets. Understanding RMD rules helps in strategic planning around tax brackets, Social Security optimization, and legacy planning. The absence of RMDs in Roth IRAs gives you complete control over when and how much to withdraw.

Required Minimum Distribution (RMD): Minimum amount that must be withdrawn annually from tax-advantaged retirement accounts after reaching age 73

Life Expectancy Factor: IRS table value used to calculate RMD amounts

Penalty: 50% tax on amounts not withdrawn as required

• Traditional IRA RMDs begin at age 73

• Roth IRAs have no RMDs during owner's lifetime

• 50% penalty for missed RMDs

• Consider Roth conversions to reduce Traditional IRA balances and future RMDs

• Plan RMDs strategically with other income sources

• Use Roth IRAs for estate planning flexibility

• Forgetting to take RMDs from Traditional IRAs

• Assuming Roth IRAs also have RMDs

• Not considering RMDs in overall tax planning

Sarah is 35 years old, currently in the 22% tax bracket, and expects to be in the 25% tax bracket during retirement. She earns $120,000 annually and has access to a 401(k) at work. Her employer offers a 50% match up to 6% of salary. Sarah can afford to save $10,000 annually for retirement. Should she prioritize a Traditional or Roth IRA? Justify your recommendation with calculations showing the tax implications over her working years.

Recommendation: Roth IRA is better for Sarah given her circumstances.

Reasoning: Sarah expects to be in a higher tax bracket in retirement (25% vs 22%), which favors Roth contributions. By paying taxes now at 22% and withdrawing tax-free later at 25%, she saves 3% on every dollar withdrawn.

Calculations: If Sarah contributes $6,500 to Roth IRA annually for 30 years at 7% return: - Total contributions: $195,000 - Account value at retirement: ~$632,000 - If withdrawn at 25% tax rate (Traditional equivalent): $474,000 after tax - Roth value (tax-free): $632,000 - Tax advantage: $158,000

Strategy: Max out 401(k) match first ($6,000), then contribute to Roth IRA ($6,500), and potentially backdoor Roth conversion if Traditional IRA exists.

This example demonstrates the importance of comparing current vs. future tax rates when choosing between Traditional and Roth IRAs. When future tax rates are expected to be higher than current rates, Roth contributions are generally preferable. The calculation shows the compounding effect of tax-free growth over decades, which significantly amplifies the benefits of choosing the right account type.

Tax Bracket: Percentage of income paid in taxes

401(k) Match: Employer contribution matching employee contributions up to a percentageBackdoor Roth: Strategy to convert Traditional IRA to Roth despite income limits

• Higher future tax bracket favors Roth

• Always maximize employer match first

• Consider total tax strategy across all accounts

• Use online calculators to model different scenarios

• Consider "mega backdoor Roth" if available

• Reassess periodically as circumstances change

• Not considering future tax bracket changes

• Forgetting to maximize employer match first

• Not accounting for state tax implications

Mark and Lisa are married filing jointly with a combined income of $250,000. They want to contribute to Roth IRAs but are concerned about income limits. Explain their options and suggest alternative strategies for tax-advantaged retirement savings.

Income Limit Issue: For 2023, Roth IRA contribution limits begin to phase out at $218,000 AGI for married filing jointly and eliminate completely at $228,000. At $250,000, Mark and Lisa are above the income limit for direct Roth contributions.

Options:

1. Backdoor Roth Conversion: Make non-deductible Traditional IRA contributions (no income limit) then convert to Roth. Requires careful pro-rata rule consideration.

2. After-Tax 401(k) Contributions: If their plan allows, contribute after-tax dollars and roll to Roth IRA later.

3. Max Out Traditional 401(k): Get tax deduction now, accept RMDs later.

4. HSA Contributions: Triple tax advantage account that can function as a retirement account.

For their high income, a combination of maxing 401(k) and utilizing HSA would provide significant tax advantages.

Income limits represent a significant constraint for high earners wanting to access Roth benefits. The "backdoor Roth" strategy is a legal way to circumvent these limits, but it requires careful planning to avoid the pro-rata rule complications. Understanding these limitations and workarounds is essential for comprehensive retirement planning.

Modified Adjusted Gross Income (MAGI): Income measure for Roth IRA eligibility

Pro-Rata Rule: Requires prorating Traditional and Roth IRA balances when converting

Backdoor Roth: Strategy to access Roth benefits despite income limits

• Roth IRA has income limits for direct contributions

• Backdoor Roth is legal but complex

• Pro-rata rule affects conversion taxation

• Consult tax professional for backdoor Roth strategy

• Consider after-tax 401(k) if available

• Use HSA as additional tax-advantaged account

• Assuming Roth is unavailable due to income

• Improperly executing backdoor Roth conversion

• Ignoring other tax-advantaged accounts

Which IRA type provides superior estate planning benefits for leaving wealth to heirs?

Roth IRAs provide superior estate planning benefits because distributions to heirs are tax-free (assuming the account has been open for 5+ years). Traditional IRA distributions to heirs are fully taxable as ordinary income. While heirs must take RMDs from inherited Roth IRAs, they don't owe taxes on these distributions, making Roth IRAs excellent wealth-transfer vehicles.

The answer is B) Roth IRA - because distributions to heirs are tax-free.

This highlights an often-overlooked benefit of Roth IRAs - their estate planning advantages. Because the money has already been taxed, beneficiaries can receive the full benefit of the tax-free growth without owing taxes. This creates a significant advantage when considering the long-term wealth transfer potential of retirement accounts. The tax-free nature of Roth distributions to heirs can result in substantial tax savings across generations.

Stepped-Up Basis: Adjustment of asset cost basis to fair market value at death

Beneficiary: Person designated to receive IRA assets after owner's death

Required Minimum Distribution (RMD): Mandatory withdrawal amounts for beneficiaries

• Roth distributions to heirs are tax-free

• Traditional distributions to heirs are taxable

• Both require RMDs from beneficiaries

• Consider Roth IRAs as wealth transfer vehicles

• Designate beneficiaries on all accounts

• Review beneficiary designations regularly

• Not considering estate planning implications

• Assuming Traditional IRAs are better for estates

• Forgetting to update beneficiary forms

FAQ

Q: I'm young and in a low tax bracket now, but expect to be in a higher bracket in retirement. Should I still choose Roth over Traditional?

A: Yes, in your situation Roth IRA is typically the better choice. When you expect to be in a higher tax bracket in retirement, paying taxes now at a lower rate to get tax-free withdrawals later is financially advantageous. For example, if you're currently in the 12% tax bracket but expect to be in the 22% bracket in retirement, you're effectively getting a tax discount by paying 12% now instead of 22% later. Additionally, Roth IRAs offer other benefits like no required minimum distributions and tax-free inheritance for beneficiaries.

Q: Can I contribute to both a Traditional and Roth IRA in the same year?

A: Yes, you can contribute to both Traditional and Roth IRAs in the same year, but your total contributions cannot exceed the annual limit. For 2023-2024, the combined limit is $6,500 ($7,500 if 50 or older). For example, you could contribute $3,000 to a Traditional IRA and $3,500 to a Roth IRA (total $6,500). However, keep in mind that Roth contribution limits may be reduced or eliminated based on your income and filing status. It's often beneficial to diversify with both account types to have tax flexibility in retirement.