How Much Should I Invest Monthly?

Complete investment planning guide • Step-by-step explanations

Investment Planning Fundamentals:

Calculate My Investment AmountDetermining how much to invest monthly is a crucial financial decision that depends on your income, expenses, financial goals, risk tolerance, and time horizon. The right investment amount should balance your financial obligations with your long-term wealth-building objectives.

Successful monthly investing follows the principle of "paying yourself first" - treating investment contributions as essential expenses rather than optional purchases. This approach helps build wealth consistently over time through compound interest.

Key factors to consider:

- Budget Analysis: Your income minus expenses determines available funds

- Financial Goals: Target amounts and timeframes for specific objectives

- Risk Tolerance: Comfort level with market volatility

- Life Stage: Age and career progression impact investment capacity

The golden rule is to start investing as early as possible, even if it's a small amount, and gradually increase contributions over time.

Income Assessment

Calculate your monthly after-tax income to determine investment capacity.

Expense Tracking

Track monthly expenses to identify areas for reduction and investment funds.

Goal Setting

Define specific, measurable financial goals to guide investment planning.

Progress Monitoring

Regularly review and adjust your investment plan based on life changes.

Investment Goal Categories

Set specific targets for different investment timeframes:

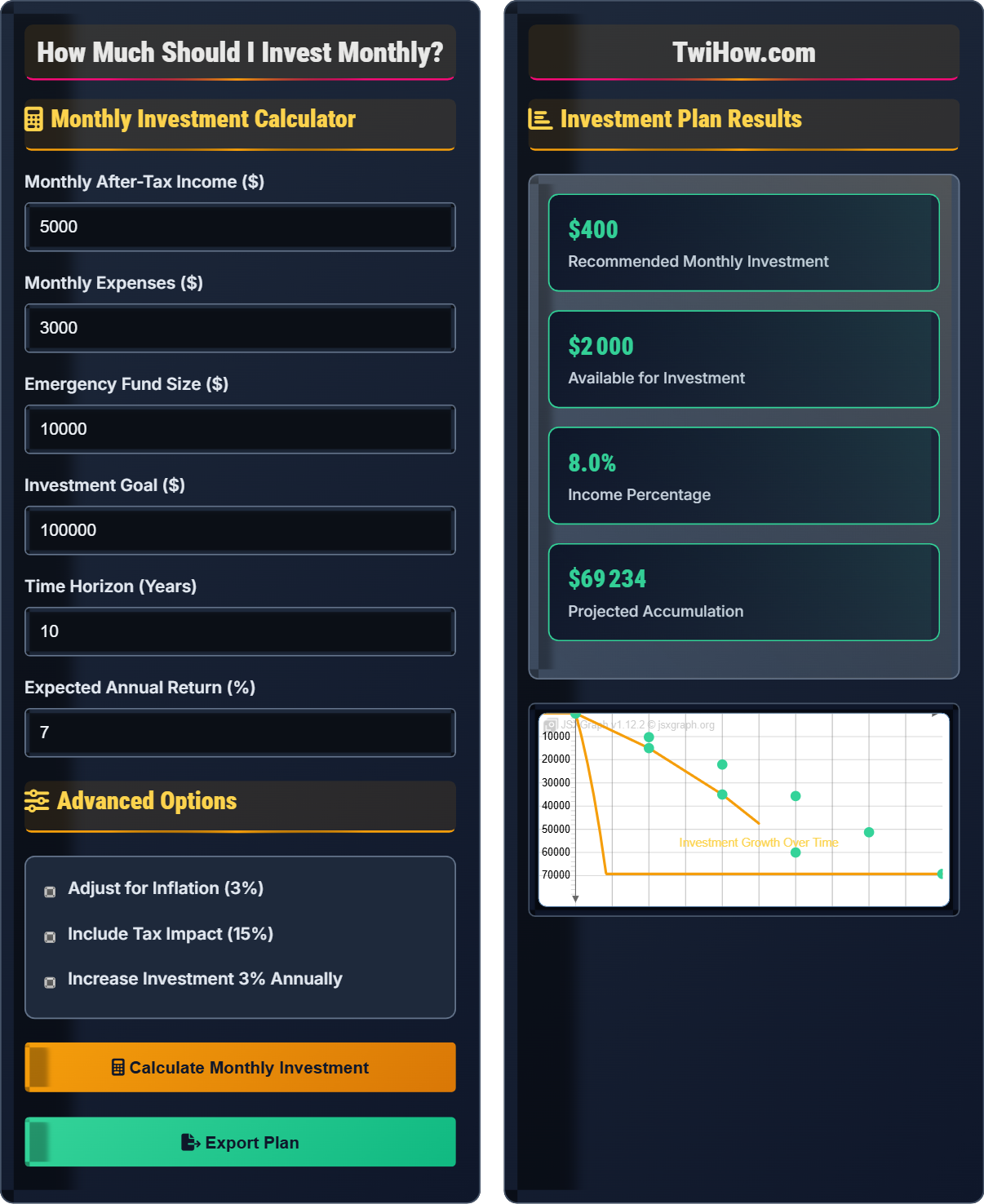

Monthly Investment Calculator

Advanced Options

Investment Plan Results

Your monthly income is $5,000 with expenses of $3,000, leaving $2,000 available for savings and investments.

To reach $100,000 in 10 years with 7% annual returns, you need to invest $500 monthly.

Set up automatic transfers to investment accounts to ensure consistent contributions.

Review your plan annually and adjust based on income changes or life events.

| Category | Amount | Percentage | Priority |

|---|---|---|---|

| Housing | $1,500 | 30% | High |

| Food & Utilities | $800 | 16% | High |

| Transportation | $400 | 8% | Medium |

| Investments | $500 | 10% | High |

| Other | $300 | 6% | Low |

Based on your current financial situation and risk tolerance, we recommend starting with $300 monthly to establish consistent investing habits.

- Focus on low-risk investments initially

- Gradually increase as income grows

- Build emergency fund first

For maximum growth potential while maintaining financial stability, $500 monthly allows for balanced portfolio building.

- Diversified portfolio allocation

- Take advantage of compound growth

- Prepare for long-term goals

If you can afford it, $800 monthly maximizes long-term wealth accumulation and reaches goals faster.

- Higher risk tolerance required

- Significant compound growth

- Earlier financial independence

Risk Assessment

The recommended investment amount takes into account your financial stability and risk tolerance.

Investment Planning Explained

Determining how much to invest monthly involves analyzing your financial situation and setting realistic goals. The key is finding a balance between your current needs and future aspirations.

Formula for calculating monthly investment needs:

Where:

- PMT: Monthly investment amount

- FV: Future value (investment goal)

- r: Monthly interest rate (annual rate ÷ 12)

- n: Total number of months

A popular budgeting guideline that allocates after-tax income as follows:

- 50% Needs: Essential expenses (housing, food, transportation)

- 30% Wants: Non-essential expenses (entertainment, dining out)

- 20% Savings/Investments: Emergency fund and investment contributions

Of the 20% for savings/investments, you might allocate 10% to investments and 10% to emergency savings.

Different approaches to determining investment amounts:

- Fixed Dollar Amount: Invest a set amount regardless of income changes

- Percentage of Income: Invest a percentage that scales with income

- Paycheck Method: Invest a portion of each paycheck automatically

- Goal-Based: Calculate backwards from your target goal

- Surplus Method: Invest remaining funds after expenses

Approaches to optimize your investment timing:

- Dollar-Cost Averaging: Invest fixed amounts regularly regardless of price

- Automatic Transfers: Set up recurring investments to ensure consistency

- Annual Increases: Gradually increase investment amounts over time

- Windfall Investments: Invest bonuses, tax refunds, or unexpected income

- Pay Raise Strategy: Increase investments when you receive raises

Investment Planning Fundamentals

Budget analysis, goal setting, risk tolerance, compound interest, dollar-cost averaging, asset allocation.

PMT = (FV × r) / ((1 + r)^n - 1)

Where PMT = monthly payment, FV = future value, r = monthly rate, n = number of months.

- Start with emergency fund first

- Invest consistently regardless of market

- Match investment to time horizon

Planning Strategies

50/30/20 rule, dollar-cost averaging, goal-based investing, percentage-based allocation.

- Assess financial situation

- Define investment goals

- Choose appropriate strategy

- Implement and monitor

- Start early to maximize compounding

- Automate investments for consistency

- Review and adjust annually

Investment Planning Learning Quiz

According to the 50/30/20 budgeting rule, what percentage of after-tax income should be allocated to savings and investments?

The 50/30/20 rule allocates income as follows: 50% to needs (essential expenses), 30% to wants (non-essential expenses), and 20% to savings and investments. This rule provides a simple framework for managing money while ensuring adequate savings and investment contributions.

The answer is B) 20%.

The 50/30/20 rule is a widely accepted budgeting guideline that helps people balance their financial priorities. The 20% allocation to savings and investments ensures that individuals are consistently building wealth while maintaining their current lifestyle. This percentage can be split between emergency savings and investment accounts based on individual needs and goals.

50/30/20 Rule: Budgeting guideline allocating income to needs, wants, and savings

Needs: Essential expenses required for basic living

Wants: Non-essential expenses for lifestyle enhancement

• 50% for essential needs

• 30% for lifestyle wants

• 20% for savings and investments

• Adjust percentages based on individual circumstances

• Automate savings and investments

• Spending all money on wants

• Not saving enough for emergencies

• Skipping investment contributions

Explain how to assess your risk tolerance and why it's important for determining your monthly investment amount. Provide examples of how different risk tolerances would affect investment choices.

Risk Tolerance Assessment: Consider your financial goals, time horizon, age, income stability, and psychological comfort with market fluctuations.

Importance: Risk tolerance determines your investment allocation, which affects both potential returns and monthly investment requirements.

Examples: A conservative investor might choose 60% bonds/40% stocks, requiring higher monthly contributions to reach goals. An aggressive investor might choose 80% stocks/20% bonds, potentially reaching goals with lower monthly contributions but accepting higher volatility.

Risk tolerance is a critical factor in investment planning because it affects both the types of investments you choose and the amount you need to invest to reach your goals. Higher-risk investments may offer higher returns but also greater volatility. Lower-risk investments provide more stability but typically lower returns, requiring larger monthly contributions to achieve the same goals. Understanding your risk tolerance helps you select an investment strategy that you can stick with during market ups and downs.

Risk Tolerance: Comfort level with investment volatility and potential losses

Asset Allocation: Distribution of investments across asset classes

Time Horizon: Length of time until you need the money

• Match investments to risk tolerance

• Consider time horizon in allocation

• Reassess periodically

• Take risk tolerance questionnaires

• Consider how you react to market drops

• Balance risk and return objectives

• Overestimating risk tolerance

• Not considering actual reactions to losses

• Ignoring time horizon

Sarah is 30 years old and wants to retire at 65 with $1.5 million. She expects to earn 7% annually on her investments. Using the future value of an annuity formula, calculate how much she needs to invest monthly to reach her goal. If she can only afford $800/month, what would her expected retirement amount be?

Time Period: 65 - 30 = 35 years = 420 months

Monthly Rate: 7% / 12 = 0.5833% = 0.005833

Formula: PMT = FV × r / [(1 + r)^n - 1]

Required Monthly Investment: PMT = $1,500,000 × 0.005833 / [(1.005833)^420 - 1]

PMT = $8,749.50 / [10.68 - 1] = $8,749.50 / 9.68 = $904

If investing $800/month: FV = PMT × [(1 + r)^n - 1] / r

FV = $800 × [(1.005833)^420 - 1] / 0.005833 = $800 × 9.68 / 0.005833 = $1,329,000

Sarah needs $904/month to reach $1.5M, or would have $1.33M with $800/month.

This example demonstrates how the future value of an annuity formula works in practice. The formula accounts for both the regular contributions and the compound growth of those contributions over time. It shows that even small differences in monthly contributions can have significant impacts on long-term outcomes due to the power of compound interest over extended periods.

Future Value of Annuity: Total value of regular payments with compound interest

Annuity: Series of equal payments made at regular intervals

Compound Interest: Interest earned on both principal and previous interest

• Longer time periods require lower monthly amounts

• Higher returns reduce required contributions

• Start early to maximize compounding

• Use online calculators for verification

• Consider inflation in long-term planning

• Adjust for changing life circumstances

• Not accounting for inflation

• Assuming constant returns

• Underestimating required amounts

You've been investing $500/month for retirement. Now you're getting married and will have a combined household income of $8,000/month. Your new spouse has no retirement savings. How should you adjust your investment strategy and monthly contributions? Consider both joint and individual goals.

Immediate Actions: Assess combined financial situation, merge financial goals, and evaluate risk tolerance as a couple.

Increased Contributions: With higher combined income, consider increasing total monthly investment to $1,200-$1,500 (15-18% of income).

Allocation Strategy: Prioritize catch-up for spouse ($300-500/month) while maintaining your own contributions ($500-700/month).

Joint Goals: Establish shared financial objectives beyond retirement (home purchase, children's education).

Account Structure: Utilize both spouses' 401(k) matches and IRAs to maximize tax advantages.

Major life changes like marriage require reassessment of financial plans. The combined household typically has increased earning power but also new shared responsibilities. It's important to align financial goals and strategies while taking advantage of additional tax-advantaged accounts. The key is to maintain consistent investing habits while adapting to new circumstances.

Combined Income: Total household earnings from all sources

Financial Alignment: Coordinating financial goals and strategiesHousehold Budget: Joint financial plan for shared expenses

• Communicate openly about finances

• Align financial goals and strategies

• Maximize available tax advantages

• Set up automatic joint contributions

• Maintain individual investment accounts

• Schedule regular financial reviews

• Not discussing financial goals openly

• Failing to maximize employer matches

• Ignoring individual financial autonomy

Which investment strategy is most effective for consistent monthly investing?

Dollar-cost averaging (DCA) is the most effective strategy for consistent monthly investing. This approach involves investing a fixed amount regularly regardless of market conditions, which helps smooth out market volatility by buying more shares when prices are low and fewer when prices are high. Research shows that DCA reduces the impact of market timing and provides consistent investment discipline.

The answer is B) Dollar-cost averaging.

Dollar-cost averaging is particularly effective for monthly investing because it removes emotion from investment decisions and ensures consistent participation in the market. While it may not maximize returns in a continuously rising market, it provides protection against market volatility and helps investors maintain discipline. This strategy is especially valuable for beginners who might otherwise be tempted to time the market.

Dollar-Cost Averaging: Investing fixed amounts regularly regardless of price

Market Timing: Attempting to predict market movements

Investment Discipline: Consistent adherence to investment plan

• Invest consistently regardless of market

• Focus on time in market, not timing

• Maintain discipline during volatility

• Automate monthly investments

• Ignore short-term market noise

• Stay focused on long-term goals

• Trying to time the market

• Stopping during market downturns

• Emotional investment decisions

FAQ

Q: I only have $100/month to invest. Is that too little to make a difference?

A: Absolutely not! $100/month is an excellent starting point. Here's why:

Consistency Matters: Regular investing builds discipline and takes advantage of dollar-cost averaging.

Compound Growth: $100/month invested at 7% annually for 30 years would grow to approximately $121,000.

Start Early: Beginning with what you can afford and increasing over time is better than waiting for a larger amount.

Scale Up: As your income increases, you can incrementally raise your investment amount.

The key is starting the habit now, regardless of the initial amount.

Q: Should I invest monthly or wait to accumulate a larger sum?

A: Monthly investing is generally superior to accumulating for a lump sum for several reasons:

Dollar-Cost Averaging: Regular investments smooth out market volatility by buying more shares when prices are low and fewer when high.

Market Timing Risk: Waiting to accumulate a large sum means missing potential growth during the accumulation period.

Psychological Benefits: Regular investing builds discipline and reduces the pressure of making large investment decisions.

Compound Interest: Money invested earlier has more time to grow through compounding.

However, if you have a large sum ready to invest, research suggests that gradual investment over 6-12 months may be appropriate to balance market timing concerns.

Q: How do I balance investing with paying off debt?

A: The balance depends on your interest rates and financial situation:

High-Interest Debt (credit cards >8%): Pay off first, as interest rates exceed likely investment returns.

Low-Interest Debt (mortgage, student loans <6%): Consider investing simultaneously while making minimum payments.

Emergency Fund: Maintain 3-6 months of expenses regardless.

Retirement Accounts: Contribute enough to get employer matching immediately.

As a general rule, if your debt interest rate is higher than your expected investment return, prioritize debt repayment. Otherwise, consider splitting your efforts between both.