How to Build an Investment Portfolio?

Complete portfolio guide • Step-by-step explanations

Portfolio Construction Fundamentals:

Build My PortfolioBuilding an investment portfolio is a systematic process that involves selecting and combining various investment assets to meet specific financial goals while managing risk. A well-constructed portfolio balances growth potential with risk management through diversification and strategic asset allocation.

The process involves understanding your risk tolerance, time horizon, and financial objectives, then implementing a strategy that includes diversification, rebalancing, and ongoing monitoring. Successful portfolio construction requires discipline, patience, and regular review.

Key components:

- Asset Allocation: Distribution across different asset classes

- Diversification: Spreading investments to reduce risk

- Rebalancing: Periodic adjustment to maintain targets

- Monitoring: Regular review and adjustment

Following a structured approach to portfolio construction helps investors achieve their financial goals while managing risk effectively.

Asset Allocation

Strategic distribution of investments across different asset classes to balance risk and return.

Diversification

Spreading investments to reduce exposure to any single asset or risk.

Rebalancing

Periodic adjustment to maintain desired allocation as markets change.

Goal Alignment

Tailoring portfolio to meet specific financial objectives and time horizons.

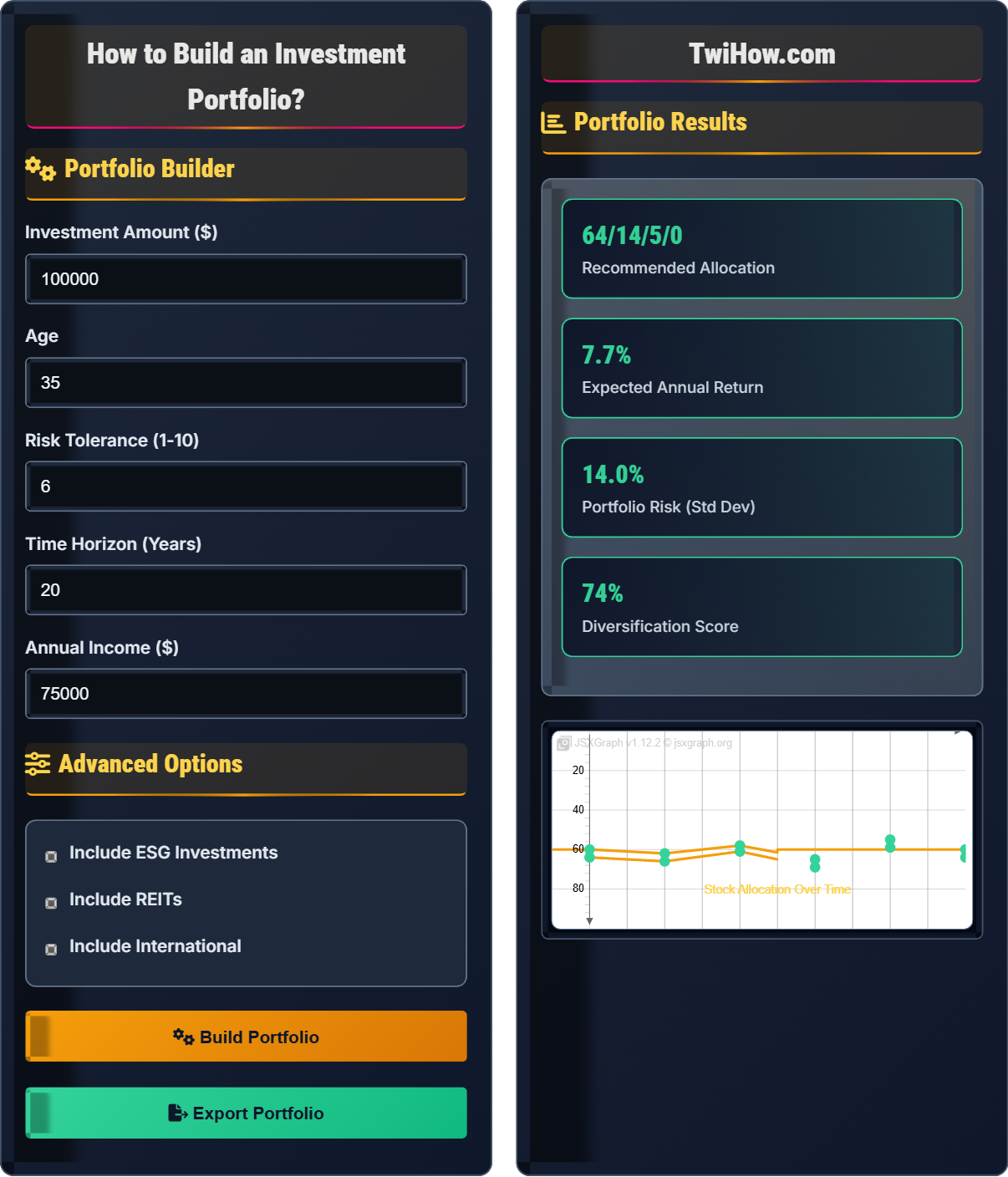

Portfolio Builder

Advanced Options

Portfolio Results

Recommended Asset Allocation

Allocation: 40% Stocks, 50% Bonds, 10% Alternatives

Focus: Capital preservation and income generation

- Lower volatility

- Regular income

- Protection from market downturns

Allocation: 80% Stocks, 15% Bonds, 5% Alternatives

Focus: Long-term capital appreciation

- Higher growth potential

- Acceptable volatility

- Time to recover from losses

Establish clear financial objectives including time horizon, expected returns, and risk tolerance. Specific goals help determine appropriate investment strategies.

Determine the mix of asset classes (stocks, bonds, alternatives) based on risk tolerance and time horizon. This is the most critical decision in portfolio construction.

Spread investments across different sectors, geographic regions, and asset classes to reduce risk and improve risk-adjusted returns.

Portfolio Rebalancing

Regular rebalancing maintains your target allocation as market movements change your portfolio's composition:

Portfolio Monitoring Tools

Portfolio Construction Explained

Building an investment portfolio is a systematic process that involves selecting and combining various investment assets to meet specific financial goals while managing risk. A well-constructed portfolio balances growth potential with risk management through diversification and strategic asset allocation.

The Modern Portfolio Theory, developed by Harry Markowitz, provides the mathematical framework for portfolio construction by showing how to achieve optimal portfolios that offer the highest expected return for a given level of risk.

The optimal portfolio allocation can be determined using the following optimization:

Subject to: \(\sum_{i=1}^{n} w_i = 1\) and \(\sum_{i=1}^{n} w_i \mu_i = \mu_p\)

- \(\sigma_p^2\): Portfolio variance

- \(w_i, w_j\): Weights of assets i and j

- \(\sigma_{ij}\): Covariance between assets i and j

- \(\mu_i\): Expected return of asset i

- \(\mu_p\): Target portfolio return

Different approaches to determining portfolio allocation:

- Age-Based: Subtract age from 100 to determine stock allocation

- Life-Cycle: Automatically adjust allocation over time

- Goals-Based: Allocate based on specific financial objectives

- Mean-Variance: Use mathematical optimization

- Factor-Based: Allocate based on risk factors

- Equal Weighting: Equal allocation across all assets

Methods for maintaining target allocation:

- Calendar Rebalancing: Rebalance at regular intervals

- Threshold Rebalancing: Rebalance when allocation drifts beyond a threshold

- Hybrid Rebalancing: Combination of calendar and threshold methods

- Drift Rebalancing: Rebalance based on portfolio drift from targets

Portfolio Construction Fundamentals

Asset allocation, diversification, rebalancing, risk tolerance, portfolio optimization, Modern Portfolio Theory.

Minimize σ²ₚ = ΣᵢΣⱼ wᵢwⱼσᵢⱼ subject to constraints

Where σ²ₚ = portfolio variance, wᵢ = asset weights, σᵢⱼ = covariance between assets.

- Asset allocation is most important decision

- Diversification reduces risk

- Rebalance regularly to maintain targets

Construction Strategies

Age-based allocation, life-cycle investing, goals-based investing, factor-based allocation, equal weighting.

- Assess risk tolerance and goals

- Choose appropriate allocation strategy

- Select diversification approach

- Implement rebalancing plan

- Match allocation to time horizon

- Consider tax implications

- Factor in transaction costs

Portfolio Construction Learning Quiz

What is the most important factor in determining asset allocation?

Asset allocation should be based primarily on your risk tolerance and time horizon. These factors determine your ability and willingness to take risk, which directly influences the appropriate mix of stocks, bonds, and other assets. While market conditions and economic forecasts are important considerations, they shouldn't be the primary drivers of asset allocation decisions.

The answer is B) Risk tolerance and time horizon.

Asset allocation is the foundation of portfolio construction and should be determined by personal factors rather than market timing. Your risk tolerance reflects your psychological comfort with volatility, while your time horizon determines your ability to recover from losses. Together, these factors help determine the appropriate balance between growth and stability in your portfolio.

Asset Allocation: Distribution of investments across asset classes

Risk Tolerance: Willingness to accept uncertainty and potential losses

Time Horizon: Length of time before needing investment returns

• Asset allocation drives most portfolio returns

• Personal factors should drive allocation

• Rebalance to maintain targets

• Focus on long-term personal factors

• Consider life changes in allocation

• Using market timing for allocation

• Ignoring personal risk tolerance

• Not adjusting for life changes

Explain the benefits of diversification and why it's important in portfolio construction. Provide specific examples of how diversification reduces risk without necessarily reducing returns.

Benefits of Diversification: Diversification reduces portfolio risk by spreading investments across different assets that don't move in perfect correlation. When some investments decline, others may rise, smoothing out overall returns.

Mathematical Principle: Portfolio variance is not simply the weighted average of individual variances but also depends on correlations between assets. Lower correlations lead to greater diversification benefits.

Example: A portfolio with 50% stocks and 50% bonds will have lower volatility than a portfolio with 100% stocks, while potentially maintaining similar long-term returns due to the different risk-return profiles of the two asset classes.

Diversification works because different asset classes and individual securities respond differently to market events. The key is selecting assets with low or negative correlations, meaning they don't all move in the same direction at the same time. This reduces the impact of any single investment on the overall portfolio while maintaining the potential for growth from the combined assets.

Diversification: Spreading investments to reduce risk

Correlation: Statistical measure of how assets move together

Portfolio Variance: Measure of portfolio risk

• Choose low-correlation assets

• Diversify across asset classes

• Geographic diversification is important

• Use index funds for instant diversification

• Consider international exposure

• Rebalance to maintain diversification

• Thinking all stocks are diversified

• Not considering correlation changes

• Over-diversification

You have a $100,000 portfolio allocated 60% stocks/40% bonds. After a year of strong stock market performance, your portfolio is now 70% stocks/30% bonds with a value of $115,000. You prefer a threshold-based rebalancing strategy with a 5% tolerance band. Should you rebalance now? If so, what transactions would you need to make to restore your target allocation?

Current Situation: Stocks: $80,500 (70%), Bonds: $34,500 (30%)

Target Allocation: Stocks: $69,000 (60%), Bonds: $46,000 (40%)

Threshold Analysis: Stock allocation has drifted from 60% to 70%, which is a 10% deviation. Since your tolerance is 5%, rebalancing is required.

Transactions Needed: Sell $11,500 of stocks and buy $11,500 of bonds to restore the 60/40 allocation.

This rebalancing brings your portfolio back to target allocation, maintaining your desired risk level.

This example demonstrates why rebalancing is important. Without rebalancing, your portfolio would continue to drift toward a more aggressive allocation as stocks outperform bonds. This would increase your risk level beyond your comfort zone. Rebalancing forces you to "sell high" (stocks) and "buy low" (bonds), maintaining your planned risk level and potentially improving long-term returns.

Rebalancing: Adjusting portfolio to maintain target allocation

Threshold-Based: Rebalancing when allocation deviates beyond tolerance

Tolerance Band: Acceptable range for allocation drift

• Rebalance when threshold exceeded

• Sell high, buy low

• Maintain planned risk level

• Use tax-advantaged accounts for rebalancing

• Consider transaction costs

• Rebalance regularly

• Not rebalancing regularly

• Ignoring tax implications

• Rebalancing too frequently

You're 35 years old with a 70% stock/30% bond portfolio. You're planning to retire in 30 years and have a high risk tolerance. Now you're getting married and planning to have children. How should you adjust your portfolio allocation and rebalancing strategy to account for these life changes?

Immediate Adjustments: While your long-term time horizon remains the same, family responsibilities may reduce your risk capacity. Consider shifting to 65% stocks/35% bonds to account for new financial responsibilities.

Long-term Strategy: Maintain a glide path that gradually shifts to more conservative allocation as retirement approaches, but adjust the starting point to reflect new circumstances.

Rebalancing: Continue with threshold-based rebalancing but consider shorter time horizons for rebalancing as family expenses may require more stable income.

Monitoring: Increase frequency of portfolio reviews to account for changing family needs.

Life changes significantly impact portfolio construction. While your time horizon for retirement remains long, family responsibilities create new financial needs and potentially reduce your ability to take risk. The key is to find a balance between maintaining growth potential for long-term goals while being mindful of new responsibilities. Regular reassessment is crucial as circumstances evolve.

Risk Capacity: Financial ability to take risk

Glide Path: Gradual shift in allocation over time

Life Changes: Events affecting financial circumstances

• Reassess after major life changes

• Consider both risk tolerance and capacity

• Adjust strategy as circumstances change

• Plan for family-related expenses

• Maintain emergency fund

• Reassess annually

• Not adjusting for family responsibilities

• Maintaining same risk level despite changes

• Not involving spouse in decisions

According to Modern Portfolio Theory, what is the primary benefit of diversification?

Modern Portfolio Theory shows that diversification can reduce unsystematic risk (specific to individual companies or sectors) without necessarily reducing expected returns. The theory demonstrates that by combining assets with different risk-return characteristics, investors can achieve better risk-adjusted returns. Systematic risk (market-wide risk) cannot be eliminated through diversification.

The answer is B) Reducing unsystematic risk without necessarily reducing expected returns.

Modern Portfolio Theory revolutionized investing by mathematically proving that diversification could improve risk-adjusted returns. The key insight is that diversification eliminates unsystematic risk (company-specific or industry-specific risk) while maintaining exposure to systematic risk (market risk) that provides the expected returns. This is why diversification is often called "the only free lunch in finance" - it reduces risk without necessarily reducing expected returns.

Modern Portfolio Theory: Mathematical framework for portfolio construction

Unsystematic Risk: Company or industry-specific risk

Systematic Risk: Market-wide risk that cannot be diversified away

• Diversification eliminates unsystematic risk

• Systematic risk remains regardless of diversification

• Optimal portfolios lie on efficient frontier

• Focus on diversification benefits

• Understand different risk types

• Use MPT principles in allocation

• Believing diversification eliminates all risk

• Not understanding systematic vs unsystematic risk

• Over-diversifying to eliminate market risk

FAQ

Q: How many investments should I have in my portfolio?

A: The number of investments depends on your approach:

Index Fund Approach: 3-5 funds can provide excellent diversification (e.g., total stock market, international, bonds).

Individual Stock Approach: 20-30 stocks for adequate diversification, though this requires significant research.

Practical Considerations:

• More positions reduce idiosyncratic risk but increase complexity

• Transaction costs increase with more positions

• Management time increases with more holdings

Recommendation: For most investors, 3-7 well-diversified funds provide optimal diversification with manageable complexity.

Q: Should I rebalance my portfolio myself or hire a professional?

A: The decision depends on several factors:

DIY Rebalancing:

• Pros: Lower costs, more control, educational value

• Cons: Requires discipline, time, and knowledge

Professional Management:

• Pros: Expertise, automation, tax efficiency

• Cons: Higher costs, less control

Guidelines:

• DIY if: Portfolio under $500K, simple allocation, time to learn

• Professional if: Complex portfolio, time constraints, tax complications

Many investors use hybrid approaches with target-date funds or robo-advisors.

Q: How do I know if my portfolio is properly diversified?

A: Proper diversification includes multiple dimensions:

Asset Class Diversification: Stocks, bonds, alternatives, cash

Geographic Diversification: Domestic and international exposure

Sector Diversification: Technology, healthcare, finance, consumer goods

Company Size: Large, mid, small-cap stocks

Measures of Diversification:

• Portfolio volatility compared to individual holdings

• Correlation between different parts of portfolio

• Performance sensitivity to single events

Rule of Thumb: If losing 10% of your portfolio would devastate you, you may need more diversification.