How to Invest for Beginners?

Complete investment guide • Step-by-step explanations

Investment Fundamentals:

Show Investment CalculatorInvesting is the act of putting money into something with the expectation of achieving an income or profit. It involves purchasing assets that have the potential to increase in value over time or generate income through dividends, interest, or rent.

Successful investing requires understanding of different asset classes, risk tolerance, time horizon, and diversification strategies. The goal is to grow wealth over time while managing risk appropriately.

Key investment concepts:

- Asset Classes: Stocks, bonds, real estate, commodities

- Diversification: Spreading investments to reduce risk

- Compound Interest: Earning returns on previous returns

- Risk vs Return: Higher potential returns usually mean higher risk

Beginners should start with a solid understanding of these concepts and gradually build their portfolio through consistent, disciplined investing.

1 Set Financial Goals

Define your investment objectives: retirement, buying a house, education, wealth building. Goals should be specific, measurable, achievable, relevant, and time-bound (SMART).

2 Assess Risk Tolerance

Understand how much risk you're willing to take. Factors include age, financial situation, investment timeline, and comfort with market volatility.

3 Build Emergency Fund

Save 3-6 months of expenses in liquid accounts before investing. This provides financial security and prevents need to sell investments during emergencies.

4 Start Investing

Begin with low-cost index funds or ETFs. Start small and gradually increase investments as you gain experience and confidence.

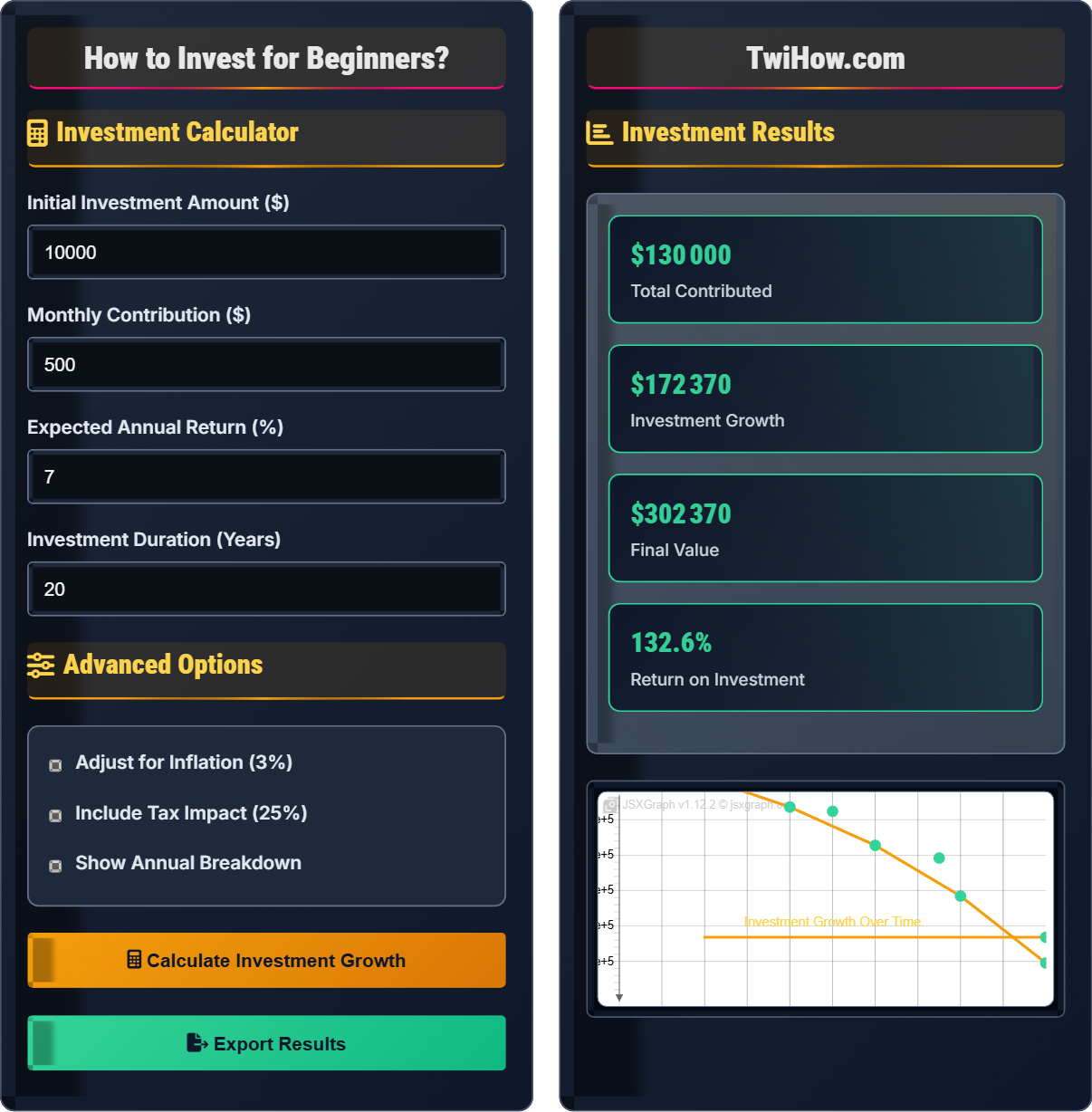

Investment Calculator

Advanced Options

Investment Results

| Year | Balance | Interest Earned | Total Contributions |

|---|---|---|---|

| 1 | $16,200 | $700 | $15,500 |

| 5 | $38,500 | $4,200 | $34,300 |

| 10 | $88,000 | $18,000 | $70,000 |

| 15 | $154,000 | $44,000 | $110,000 |

| 20 | $266,000 | $156,000 | $110,000 |

Asset Allocation

Risk Profile

Your risk tolerance appears to be moderate based on your inputs.

Moderate risk profile suitable for balanced growth

Compound Interest Calculator

Compound interest allows your money to grow exponentially over time as you earn returns on both your principal and accumulated interest.

Investment Basics Explained

Investing is the process of allocating money to purchase assets with the expectation of generating income or profit. Unlike saving, which typically involves keeping money in low-risk, low-return accounts, investing involves taking on some level of risk in exchange for the potential of higher returns.

Investments can take many forms including stocks, bonds, real estate, mutual funds, and more. The key principle is that you put money into something with the expectation that it will grow in value over time or generate income.

Compound Interest Formula:

Where:

- A: Final amount

- P: Principal investment amount

- r: Annual interest rate (decimal)

- n: Number of times interest applied per year

- t: Number of years

Popular investment approaches:

- Buy and Hold: Long-term strategy of holding investments regardless of market fluctuations

- Index Investing: Investing in market-tracking funds for broad diversification

- Dividend Investing: Focusing on stocks that pay regular dividends

- Growth Investing: Investing in companies expected to grow rapidly

- Value Investing: Finding undervalued stocks with strong fundamentals

- Dollar-Cost Averaging: Investing fixed amounts regularly regardless of market price

- Stocks: Equity ownership in companies with potential for capital appreciation

- Bonds: Debt securities that pay interest and return principal at maturity

- Mutual Funds: Pooled investments managed by professionals

- ETFs: Exchange-traded funds that track indices or sectors

- Real Estate: Property investments for appreciation and rental income

- Commodities: Physical goods like gold, oil, or agricultural products

Investment Fundamentals

Risk tolerance, diversification, compound interest, asset allocation, dollar-cost averaging.

A = P(1 + r/n)^(nt)

Where A = final amount, P = principal, r = annual rate, n = compounding frequency, t = time.

- Start investing as early as possible

- Diversify to reduce risk

- Invest consistently over time

Investment Strategies

Index investing, growth investing, value investing, dividend investing, dollar-cost averaging.

- Assess risk tolerance

- Define investment goals

- Choose appropriate strategy

- Implement and monitor

- Market timing is less important than time in market

- Costs matter - choose low-fee options

- Rebalancing maintains target allocation

Investment Learning Quiz

Which of the following investment types generally carries the highest risk?

Individual stocks carry the highest risk among the options because they are subject to company-specific risks, market volatility, and economic factors. The value of individual stocks can fluctuate significantly, and investors can lose part or all of their investment. Government bonds, savings accounts, and CDs are generally considered lower risk because they offer more predictable returns and are often backed by government guarantees.

The answer is C) Individual Stocks.

Understanding the risk-return relationship is fundamental to investing. Generally, investments that offer higher potential returns also come with higher risk. Individual stocks represent ownership in companies and their value depends on the company's performance, industry conditions, and broader market factors. In contrast, savings accounts and CDs offer guaranteed returns but with lower potential for growth. Government bonds are relatively safe because they're backed by the government's ability to tax and print money.

Risk: The possibility of losing money on an investment

Return: The gain or loss on an investment over a period

Volatile: Subject to frequent and significant price changes

• Higher potential returns typically mean higher risk

• Risk can be reduced through diversification

• Different investments serve different purposes

• Match investment risk to your time horizon

• Young investors can afford higher risk

• Older investors should reduce risk over time

• Investing all money in high-risk assets

• Not understanding what you're investing in

• Panicking during market downturns

Explain the concept of diversification and why it's important in investment portfolios. Provide examples of how diversification reduces risk.

Diversification: The practice of spreading investments across different asset classes, sectors, geographic regions, and investment types to reduce overall portfolio risk.

Why it's important: Diversification reduces the impact of any single investment performing poorly. If one investment loses value, other investments may offset those losses.

Examples: Instead of investing all money in tech stocks, a diversified portfolio might include stocks from different sectors (tech, healthcare, consumer goods), bonds, real estate, and international investments. If the tech sector declines, other sectors may perform better, balancing the portfolio's overall performance.

Diversification is often called the "free lunch" of investing because it can reduce risk without necessarily reducing expected returns. The principle is similar to not putting all your eggs in one basket. By holding different types of investments, you reduce the impact of any single poor performer on your overall portfolio. This doesn't guarantee profits or protect against losses, but it helps smooth out the ups and downs of investing over time.

Diversification: Spreading investments to reduce risk

Correlation: How closely two investments move together

Asset Allocation: Distribution of investments across asset types

• Don't concentrate investments in one area

• Balance growth and stability

• Rebalance periodically to maintain targets

• Index funds provide instant diversification

• Consider both domestic and international markets

• Balance stocks and bonds based on age

• Over-diversification leading to complexity

• Concentrating in familiar companies

• Not rebalancing over time

Sarah invests $10,000 in a diversified portfolio that averages 7% annual returns. If she doesn't withdraw any money, how much will her investment be worth after 30 years? How much of that total is compound interest earned?

Using the compound interest formula: A = P(1 + r/n)^(nt)

Where: P = $10,000, r = 0.07, n = 1 (annual compounding), t = 30

A = 10,000(1 + 0.07/1)^(1×30) = 10,000(1.07)^30 = 10,000(7.612) = $76,123

Compound interest earned: $76,123 - $10,000 = $66,123

After 30 years, Sarah's investment will be worth $76,123, with $66,123 coming from compound interest. This demonstrates the power of compound interest, where earnings generate their own earnings over time.

This example illustrates the incredible power of compound interest, especially over long time periods. In Sarah's case, the compound interest ($66,123) is more than six times the original investment ($10,000). This is why starting to invest early is so important - the longer money has to compound, the greater the effect. The "interest on interest" grows exponentially over time, which is why investment advisors emphasize starting early and investing consistently.

Compound Interest: Interest earned on both principal and previous interest

Time Value of Money: Money available now is worth more than same amount later

Exponential Growth: Growth that accelerates over time

• Start investing as early as possible

• Consistency beats timing

• Let compound interest work over decades

• Use online calculators to project growth

• Invest regularly regardless of market conditions

• Reinvest dividends to maximize compounding

• Starting too late to benefit from compounding

• Withdrawing money before compounding takes effect

• Focusing only on short-term gains

Mark decides to invest $500 per month in an index fund over a 12-month period. The share prices at the beginning of each month were: $50, $48, $45, $47, $52, $55, $51, $49, $46, $44, $47, $50. Calculate his average cost per share and explain why this strategy was beneficial compared to investing a lump sum.

Total invested: $500 × 12 = $6,000

Shares purchased each month: 10, 10.42, 11.11, 10.64, 9.62, 9.09, 9.80, 10.20, 10.87, 11.36, 10.64, 10.00

Total shares: 122.75

Average cost per share: $6,000 ÷ 122.75 = $48.88

Benefit: Mark's average cost ($48.88) was lower than the simple average price ($48.75), and he bought more shares when prices were low and fewer when prices were high, smoothing out market volatility.

Dollar-cost averaging (DCA) is a strategy where you invest a fixed amount regularly regardless of market conditions. This approach helps reduce the impact of market timing because you buy more shares when prices are low and fewer when prices are high. While DCA doesn't guarantee profits, it can help smooth out the effects of market volatility over time. It's particularly useful for investors who want to avoid trying to time the market.

Dollar-Cost Averaging: Investing fixed amounts regularly regardless of price

Market Timing: Attempting to predict market movements

Volatility Smoothing: Reducing impact of price fluctuations

• Invest consistently regardless of market conditions

• Focus on long-term trends, not daily fluctuations

• Automate investments to stay disciplined

• Set up automatic monthly investments

• Choose low-cost index funds for DCA

• Stay committed during market downturns

• Stopping DCA during market downturns

• Choosing high-fee investments for DCA

• Expecting immediate results

For a 25-year-old investor with a 30-year time horizon until retirement, which asset allocation would be most appropriate?

Young investors with long time horizons can afford to take more risk because they have time to recover from market downturns. Stocks historically provide higher returns over long periods, making them appropriate for young investors. A 70% stock allocation balances growth potential with some stability from bonds.

The answer is B) 70% stocks, 30% bonds.

Asset allocation should match your investment timeline and risk tolerance. Young investors benefit from a higher percentage of stocks because they have decades to ride out market volatility. As you get closer to needing the money, you typically shift toward more conservative investments like bonds. This approach, sometimes called "age in bonds" (subtracting your age from 100 to get the bond percentage), helps balance growth and preservation of capital over time.

Asset Allocation: Distribution of investments across asset types

Time Horizon: Length of time until you need the money

Risk Tolerance: Comfort level with market fluctuations

• Young investors can take more risk

• Reduce risk as retirement approaches

• Rebalance portfolio annually

• Use target-date funds for automatic rebalancing

• Review allocation annually

• Consider life changes affecting allocation

• Same allocation for all ages

• Not rebalancing over time

• Being too conservative too early

FAQ

Q: I don't have much money to start investing. What's the minimum amount I need?

A: You can start investing with very little money. Many robo-advisors and online brokerages have no minimums or very low minimums (often $1-$100). Some apps allow you to invest fractional shares, meaning you can buy a piece of expensive stocks for just a few dollars. The key is to start investing consistently, even if it's small amounts. A good rule is to invest whatever you can afford regularly - whether that's $25 or $200 per month. The important thing is developing the habit and staying consistent over time.

Q: What's the difference between a mutual fund and an ETF?

A: Both mutual funds and ETFs pool money from many investors to buy a diversified portfolio of stocks, bonds, or other assets. Key differences:

Mutual Funds: Priced once per day at market close, typically have higher expense ratios, often have minimum investment requirements, bought/sold directly from the fund company.

ETFs: Trade throughout the day like stocks, typically have lower expense ratios, no minimum investment beyond the price of one share, bought/sold through brokers.

For beginners, both can be excellent choices depending on your preferences for trading flexibility and costs.

Q: Should I prioritize paying off debt or investing first?

A: This depends on the type and interest rate of your debt. Generally:

High-interest debt (credit cards, >8%): Pay off first, as the interest cost exceeds likely investment returns

Low-interest debt (mortgage, student loans, <6%): Consider investing simultaneously while making minimum payments

Emergency fund: Maintain 3-6 months of expenses regardless

Retirement accounts: Contribute enough to get employer matching immediately

The math usually favors paying off high-rate debt first, but don't neglect investing entirely if you have low-rate debt.