What is Compound Interest?

Complete compound interest guide • Step-by-step explanations

Compound Interest Fundamentals:

Calculate Compound InterestCompound interest is the addition of interest to the principal sum of a loan or deposit, or in other words, interest on interest. It is the result of reinvesting interest, rather than paying it out, so that interest in the next period is then earned on the principal sum plus previously accumulated interest.

Compound interest is distinct from simple interest, where previously accumulated interest is not added to the principal amount of the current period. This exponential growth effect makes compound interest a powerful force in finance and investing.

Key concepts:

- Exponential Growth: Growth accelerates over time

- Time Value: Earlier investments grow more due to compounding

- Frequency Matters: More frequent compounding increases returns

- Wealth Building: Foundation of long-term investment success

Albert Einstein allegedly called compound interest "the eighth wonder of the world" and said "he who understands it, earns it; he who doesn't, pays it."

Interest on Interest

Compound interest earns returns on both principal and previously earned interest, creating exponential growth over time.

Time Factor

The longer money compounds, the greater the exponential growth effect due to the power of time.

Exponential Growth

Growth accelerates over time as interest builds on previous interest, creating a snowball effect.

Wealth Building

Compound interest is the foundation of long-term wealth accumulation and financial independence.

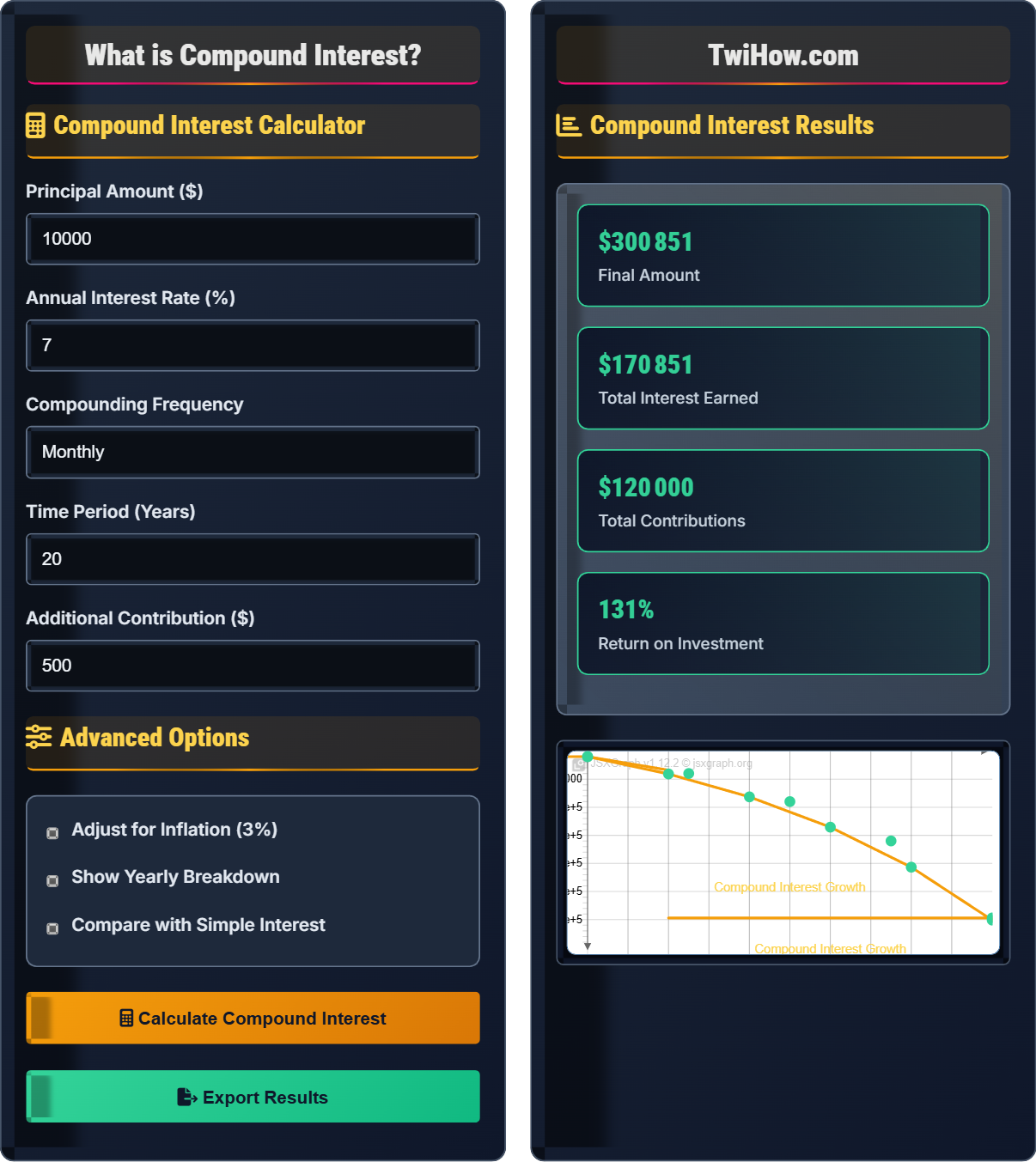

Compound Interest Calculator

Advanced Options

Compound Interest Results

| Year | Balance | Interest Earned | Total Contributions |

|---|---|---|---|

| 1 | $15,950 | $1,350 | $15,500 |

| 5 | $39,200 | $4,200 | $35,000 |

| 10 | $90,500 | $9,500 | $60,000 |

| 15 | $161,000 | $16,100 | $85,000 |

| 20 | $296,968 | $29,697 | $110,000 |

Compound interest results in $176,968 more than simple interest over 20 years.

Compound Interest Visualization

Compound interest works like a tree branching out, where each branch generates its own branches over time:

Where P = Principal, I₁ = Interest in Year 1, I₂ = Interest in Year 2, etc.

Compound Interest Formula

Where: A = final amount, P = principal, r = annual interest rate, n = number of times interest applied per year, t = time in years

Compound Interest Explained

Compound interest is the addition of interest to the principal sum of a loan or deposit, or in other words, interest on interest. It is the result of reinvesting interest, rather than paying it out, so that interest in the next period is then earned on the principal sum plus previously accumulated interest.

This differs from simple interest, where previously accumulated interest is not added to the principal amount of the current period. Compound interest is distinct from simple interest, where interest is not added to the principal.

The standard formula for compound interest is:

Where:

- A: Final amount

- P: Principal investment amount

- r: Annual interest rate (decimal)

- n: Number of times interest applied per year

- t: Number of years

Compound interest creates exponential growth rather than linear growth. Key benefits include:

- Exponential Growth: Growth accelerates over time

- Time Advantage: Earlier investments have more time to compound

- Multiplier Effect: Interest earns interest, which earns more interest

- Wealth Accumulation: Small amounts can grow significantly over time

- Passive Income: Money works for you without additional effort

Compound interest applies to various financial instruments:

- Savings Accounts: Bank accounts with compound interest

- Investment Accounts: Stocks, bonds, mutual funds

- Retirement Plans: 401(k), IRA, pension plans

- CDs: Certificates of deposit with compound interest

- Bonds: Reinvestment of coupon payments

- REITs: Real Estate Investment Trusts with dividend reinvestment

Compound Interest Fundamentals

Compound interest, exponential growth, time value of money, reinvestment, principal, interest rate.

A = P(1 + r/n)^(nt)

Where A = final amount, P = principal, r = annual rate, n = compounding frequency, t = time in years.

- Time is the most important factor

- Higher rates accelerate growth

- More frequent compounding increases returns

Applications

Savings accounts, investment portfolios, retirement planning, loan calculations, wealth building.

- Start investing early

- Invest regularly

- Reinvest dividends

- Choose appropriate investments

- Minimize fees that reduce compounding

- Consider tax implications

- Account for inflation

Compound Interest Learning Quiz

If you invest $10,000 at 5% annual interest for 10 years, how much more would you earn with compound interest compared to simple interest?

Simple Interest: $10,000 × 0.05 × 10 = $5,000 in interest

Compound Interest: $10,000 × (1.05)^10 = $16,289 (total), so $6,289 in interest

Difference: $6,289 - $5,000 = $1,289

The extra amount comes from earning interest on previously earned interest, demonstrating the power of compounding.

The answer is B) $1,289.

This example clearly demonstrates the difference between simple and compound interest. With simple interest, you only earn interest on the original principal amount. With compound interest, you earn interest on both the principal and all previously earned interest. This "interest on interest" effect becomes more pronounced over longer time periods, which is why starting to invest early is so important.

Simple Interest: Interest calculated only on the principal amount

Compound Interest: Interest calculated on principal plus accumulated interest

Principal: Original amount invested or borrowed

• Compound interest grows exponentially

• Simple interest grows linearly

• Difference increases with time

• Use the rule of 72 to estimate doubling time

• Longer time periods amplify the effect

• Confusing simple and compound interest

• Not accounting for compounding frequency

• Underestimating the time factor

Explain why time is the most important factor in compound interest. Use specific examples to illustrate how starting to invest earlier can result in significantly more wealth despite contributing less money.

Time Importance: Time allows compound interest to work more effectively, as each year of compounding builds on all previous years' growth.

Example: Person A invests $5,000 annually for 10 years starting at age 25, then stops. Person B starts at age 35 and invests $5,000 annually for 30 years.

Person A invests $50,000 total but at age 65 has ~$602,000.

Person B invests $150,000 total but at age 65 has ~$472,000.

Despite investing $100,000 less, Person A ends up with $130,000 more due to the additional 10 years of compounding.

This example perfectly illustrates the exponential nature of compound interest. The first investments have the longest time to grow and compound, which creates a snowball effect. The last few years of investing often contribute more to the final amount than the first several years of contributions because of the accumulated growth. This is why financial advisors always emphasize starting to invest as early as possible.

Time Value of Money: Money available now is worth more than same amount later

Exponential Growth: Growth that accelerates over time

Snowball Effect: Growth that accelerates as it builds upon itself

• Start investing as early as possible

• Even small amounts benefit from compounding

• The last years contribute disproportionately

• Use the "pay yourself first" principle

• Automate investments to stay consistent

• Take advantage of employer matches

• Delaying investment start date

• Underestimating compound interest power

• Focusing only on contribution amounts

Mike wants to retire with $1 million in 30 years. He expects to earn 7% annually on his investments. Using compound interest, calculate how much he needs to invest today as a lump sum. Then calculate how much he would need to invest monthly to reach the same goal. Explain the difference in strategies.

Lump Sum Calculation: Using A = P(1+r)^t, we get $1,000,000 = P(1.07)^30

P = $1,000,000 / (1.07)^30 = $1,000,000 / 7.612 = $131,367

Monthly Investment: Using future value of annuity formula: FV = PMT × [((1+r)^n - 1) / r]

With monthly compounding: $1,000,000 = PMT × [((1.00583)^360 - 1) / 0.00583]

PMT = $1,000,000 / 1,219.97 = $819.71 per month

Difference: Lump sum requires $131,367 upfront, while monthly investing totals $295,096, but spreads the burden over time.

This example shows two different paths to the same goal. The lump sum approach requires a significant upfront investment but benefits from maximum compounding time. The monthly approach is more practical for most people but requires a larger total investment due to the later timing of contributions. Both approaches leverage compound interest, but the timing of money invested significantly affects the required amounts.

Lump Sum: Single payment made at one time

Annuity: Series of equal payments made at regular intervals

Present Value: Current value of future sum

• Earlier money has more compounding time

• Regular contributions build over time

• Both strategies use compound interest

• Start with what you can afford

• Increase contributions over time

• Take advantage of compound growth

• Not starting soon enough

• Underestimating required amounts

• Not adjusting for inflation

Compare the growth of $10,000 invested at 6% annual interest over 10 years with different compounding frequencies: annually, monthly, and daily. Calculate the final amounts and explain why more frequent compounding results in higher returns.

Annual Compounding: A = $10,000(1 + 0.06/1)^(1×10) = $10,000(1.06)^10 = $17,908

Monthly Compounding: A = $10,000(1 + 0.06/12)^(12×10) = $10,000(1.005)^120 = $18,194

Daily Compounding: A = $10,000(1 + 0.06/365)^(365×10) = $10,000(1.000164)^3650 = $18,220

Difference: Daily compounding yields $312 more than annual due to more frequent interest additions.

Explanation: More frequent compounding means interest is added to the principal more often, allowing each subsequent interest calculation to work with a slightly larger base amount.

This example demonstrates that the frequency of compounding matters, though the effect diminishes as frequency increases. The difference between annual and monthly compounding is more significant than between monthly and daily. This is why high-yield savings accounts that compound daily are preferable to those that compound monthly or annually, all else being equal.

Compounding Frequency: How often interest is calculated and added

Annual Percentage Yield (APY): Effective annual rate considering compounding

Effective Rate: Actual rate earned considering compounding

• More frequent compounding = higher returns

• Diminishing returns as frequency increases

• APY considers compounding effects

• Compare APY, not just stated rates

• Look for daily compounding when possible

• Understand the compounding schedule

• Confusing APR with APY

• Not considering compounding frequency

• Assuming all "annual" rates compound annually

Using the Rule of 72, approximately how long will it take for an investment to double at 9% annual compound interest?

The Rule of 72 states that the time to double an investment is approximately 72 divided by the annual interest rate. So, 72 ÷ 9 = 8 years. This is an approximation that becomes more accurate around 8% interest rates.

The exact calculation would be log(2)/log(1.09) ≈ 8.04 years, confirming the Rule of 72's accuracy in this case.

The answer is B) 8 years.

The Rule of 72 is a mental math shortcut that helps quickly estimate how long it takes for an investment to double at a given compound interest rate. It's particularly useful for quick comparisons between different investment options. The rule works because of the mathematical relationship between logarithms and exponential growth, making it a practical tool for financial planning.

Rule of 72: Quick estimation method for investment doubling time

Approximation: Close estimate that simplifies complex calculations

Exponential Growth: Growth that accelerates over time

• Rule of 72 = 72 ÷ interest rate

• Most accurate around 8% rates

• Provides quick mental estimates

• Use for quick investment comparisons

• Remember it's an approximation

• Works well for rates between 6-10%

• Using it for very high or low rates

• Confusing with simple interest

• Forgetting it's an approximation

FAQ

Q: Why is compound interest called "the eighth wonder of the world"?

A: This quote is often attributed to Albert Einstein (though its true origin is debated) because compound interest demonstrates a seemingly magical property: exponential growth. Unlike linear growth where increases are constant, exponential growth accelerates over time.

For example, if you start with $1 and double it every day, by day 30 you'd have over $500 million! While investment returns aren't this dramatic, the principle is the same - the growth becomes significantly faster in later years due to the interest earning interest effect. This exponential nature is what makes starting to invest early so powerful.

Q: How does compound interest work with investments like stocks that don't pay interest?

A: With stocks, compound interest works through capital appreciation and dividend reinvestment. When you reinvest dividends, you purchase additional shares that themselves generate more dividends. Additionally, as stock prices appreciate, the value of all your shares (including those acquired through dividend reinvestment) increases.

For example, if you own 100 shares of a $100 stock paying a 2% dividend yield, you receive $200 in dividends. If you reinvest those dividends, you buy more shares. Next year, you'll earn dividends on more than 100 shares, and the process continues. This creates the same compounding effect as traditional interest-bearing accounts.

Q: Can compound interest work against me?

A: Absolutely. Compound interest works both ways - it can grow your investments but also increase your debt. Credit card debt is the most common example. If you carry a balance at 18% annual interest, the interest compounds monthly, meaning you pay interest on your interest.

For example, a $1,000 credit card balance at 18% APR compounded monthly becomes $1,196 after one year, then $1,428 after two years, growing exponentially. This is why it's crucial to pay off high-interest debt quickly and why compound interest is both a powerful wealth-building tool and a dangerous debt-accumulating force.