What is Risk Tolerance?

Complete risk tolerance guide • Step-by-step explanations

Risk Tolerance Fundamentals:

Assess My Risk ToleranceRisk tolerance is the degree of variability in investment returns that an investor is willing to withstand. It reflects an individual's willingness to accept uncertainty and potential losses in pursuit of higher returns. Understanding your risk tolerance is crucial for making appropriate investment decisions and building a portfolio that aligns with your comfort level.

Risk tolerance is influenced by various factors including personality, age, financial situation, investment goals, and life experience. It's important to distinguish between risk tolerance (willingness to take risk) and risk capacity (ability to take risk based on financial circumstances).

Key aspects:

- Personal Assessment: Understanding your comfort with market fluctuations

- Financial Capacity: Your ability to absorb losses without affecting financial goals

- Investment Horizon: Time available to recover from market downturns

- Goal Alignment: Matching investments to your objectives

Properly assessing risk tolerance helps investors avoid emotional decision-making during market volatility and maintain a consistent investment strategy.

Psychological Comfort

Your emotional response to market volatility and potential losses.

Financial Capacity

Your ability to withstand financial losses without impacting your goals.

Time Horizon

The length of time before you need to access your investments.

Goal Alignment

Matching investment risk to your specific financial objectives.

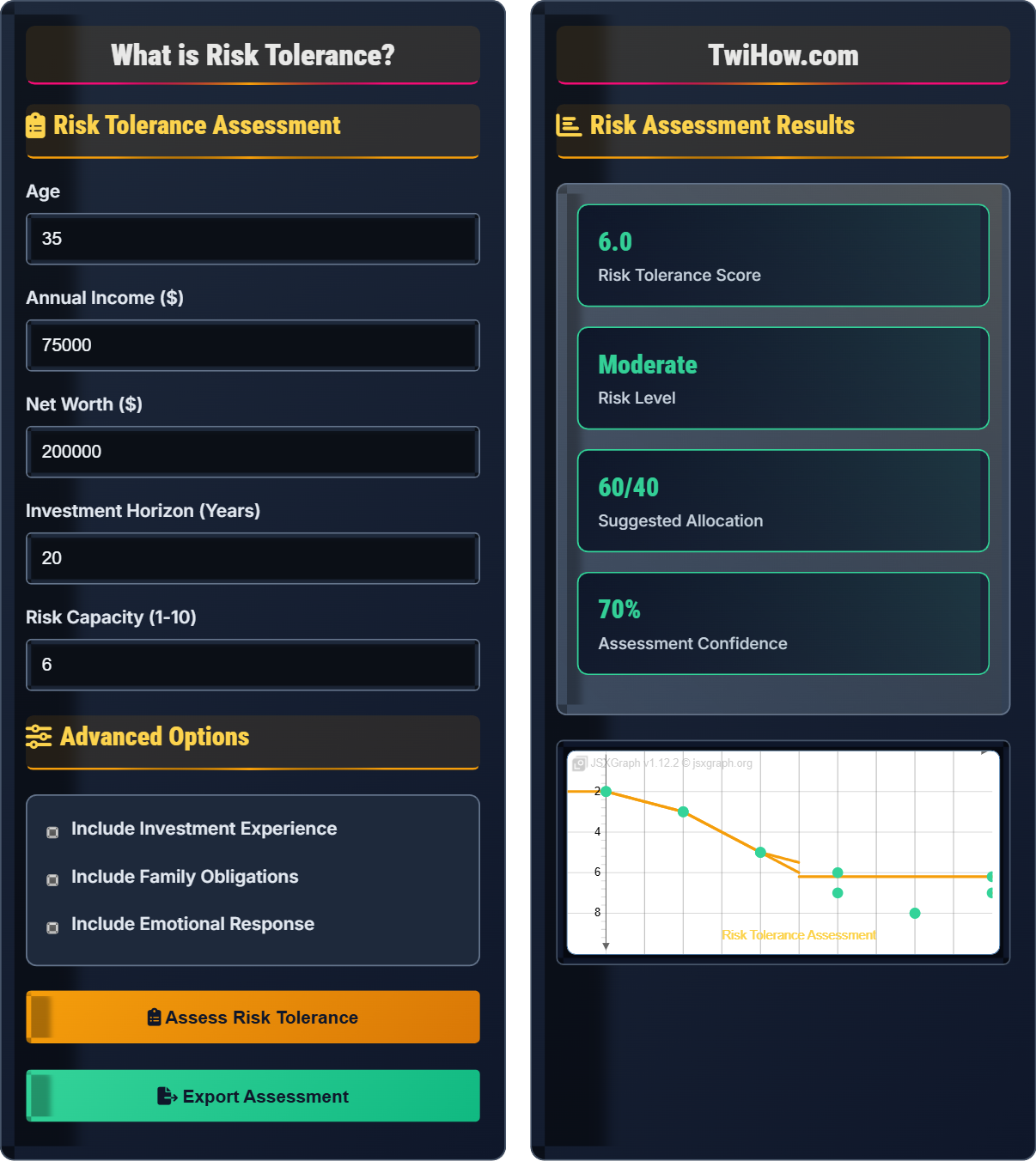

Risk Tolerance Assessment

Advanced Options

Risk Assessment Results

Characteristics: Balanced approach to risk and return. Willing to accept some volatility for potential growth.

Behavior: May experience some anxiety during market downturns but generally maintains course.

Investment Style: Mix of growth and stability-oriented investments.

- Comfortable with 15-20% market drops

- Seeks diversified portfolio

- Focuses on long-term goals

Conservative: Prioritizes capital preservation over growth. Prefers low-volatility investments.

Aggressive: Seeks maximum growth potential. Comfortable with high volatility.

Very Conservative: Minimal risk tolerance. Focuses on safety and income.

Suggested Asset Allocation

Risk Tolerance Assessment Questions

These questions help determine your comfort level with investment risk:

a) Sell everything immediately to prevent further losses

b) Sell some investments to reduce risk

c) Hold steady and wait for recovery

d) Buy more at lower prices

a) Preserve capital and avoid losses

b) Generate steady income

c) Achieve moderate growth

d) Maximize returns regardless of risk

a) Less than 2 years

b) 2-5 years

c) 5-10 years

d) More than 10 years

Younger investors typically have higher risk tolerance due to longer time horizon for recovery from losses. As you age, risk tolerance often decreases.

Those with stable income and emergency funds can afford higher risk. Those with financial constraints should be more conservative.

Greater knowledge often correlates with higher risk tolerance as investors better understand market dynamics and long-term trends.

Risk Scenarios

How different risk profiles might react to market events:

Conservative: Panic sell, move to cash, miss recovery

Moderate: Hold steady, maybe add at lows

Aggressive: Buy more at discounted prices

Conservative: Take profits, reduce risk

Moderate: Stay invested, maintain allocation

Aggressive: Increase equity allocation

Conservative: Move to safer assets

Moderate: Maintain diversification

Aggressive: Look for opportunities

Risk Education Resources

Risk Tolerance Explained

Risk tolerance is the degree of variability in investment returns that an investor is willing to withstand. It reflects an individual's willingness to accept uncertainty and potential losses in pursuit of higher returns. Risk tolerance is distinct from risk capacity, which refers to the financial ability to absorb losses without affecting financial goals.

Understanding your risk tolerance is crucial for making appropriate investment decisions and building a portfolio that aligns with your comfort level.

Quantitative models for assessing risk tolerance:

Where:

- Willingness: Psychological comfort with risk

- Ability: Financial capacity to take risk

- Need: Required risk to meet financial goals

Common risk tolerance classifications:

- Very Conservative: Focus on capital preservation, minimal risk

- Conservative: Emphasis on safety with modest growth

- Moderate: Balanced approach to risk and return

- Aggressive: Higher risk for greater growth potential

- Very Aggressive: Maximum risk tolerance, growth-focused

Key determinants of risk tolerance:

- Age: Younger investors typically have higher tolerance

- Financial Stability: Stable income allows for higher risk

- Investment Experience: More experience often increases tolerance

- Personality: Natural disposition toward risk-taking

- Investment Goals: Time horizon and return objectives

- Life Circumstances: Family obligations and responsibilities

Risk Tolerance Fundamentals

Risk tolerance, risk capacity, risk willingness, investment psychology, behavioral finance, volatility.

Risk Tolerance = (Willingness + Ability + Need) / 3

Where willingness = psychological comfort, ability = financial capacity, need = required risk.

- Assess both willingness and ability to take risk

- Consider time horizon in risk decisions

- Reassess periodically as circumstances change

Risk Assessment

Questionnaires, scenario analysis, financial capacity evaluation, psychological profiling.

- Self-evaluation of comfort level

- Financial situation analysis

- Goal setting and time horizon

- Portfolio construction

- Match risk tolerance to investment goals

- Consider emotional responses to market events

- Factor in family and financial obligations

Risk Tolerance Learning Quiz

What is the primary difference between risk tolerance and risk capacity?

Risk tolerance refers to an individual's psychological willingness to accept uncertainty and potential losses (emotional aspect), while risk capacity refers to the financial ability to withstand losses without affecting financial goals (financial aspect).

The answer is A) Risk tolerance is emotional, risk capacity is financial.

This distinction is crucial for proper investment planning. Someone might have a high financial capacity (ability to take losses) but low emotional tolerance (uncomfortable with risk). Conversely, someone might be emotionally comfortable with risk but have low financial capacity (cannot afford to take losses). Both factors must be considered when determining appropriate investment strategies.

Risk Tolerance: Willingness to accept uncertainty and potential losses

Risk Capacity: Financial ability to withstand losses

Investment Psychology: Emotional response to investment decisions

• Consider both tolerance and capacity

• Emotional comfort affects investment behavior

• Financial capacity sets limits

• Assess both emotional and financial factors

• Factor in family obligations

• Only considering financial capacity

• Ignoring emotional responses

• Overestimating risk tolerance

Explain how age affects risk tolerance and why younger investors typically have higher risk tolerance. Discuss the implications for investment allocation and portfolio construction.

Age Impact: Younger investors typically have higher risk tolerance due to longer investment time horizons, allowing more time to recover from market downturns.

Recovery Time: A 25-year-old has 40+ years to recover from losses, while a 60-year-old has only 5-10 years before retirement.

Implications: Younger investors can afford to allocate more to growth assets (stocks), while older investors should focus on preservation and income.

Portfolio Construction: Age-based allocation models suggest higher equity allocation when young (e.g., 90% stocks at age 25) gradually shifting to more conservative allocation as one ages (e.g., 50% stocks at age 65).

The relationship between age and risk tolerance is fundamental to investment planning. The time horizon concept is crucial—more time allows for greater recovery from temporary losses. This is why financial advisors often recommend aggressive allocation when young and conservative allocation when approaching retirement. However, individual circumstances may vary, so personal risk tolerance should always be assessed alongside age-based guidelines.

Time Horizon: Length of time before needing investment returns

Recovery Time: Period needed to recover from losses

Asset Allocation: Distribution of investments across asset classes

• Longer time horizon = higher risk tolerance

• Shift to conservative as retirement approaches

• Consider individual circumstances

• Use age-based allocation as starting point

• Adjust based on personal comfort

• Reassess regularly

• Ignoring time horizon in allocation

• Not adjusting as age changes

• Following age-based rules rigidly

Sarah is 30 years old with a moderate risk tolerance. Her portfolio consists of 60% stocks and 40% bonds. Due to a market crash, her portfolio dropped 30%, leaving her uncomfortable with the risk level. She now feels more conservative. How should she adjust her portfolio, and what does this teach us about risk tolerance assessment?

Immediate Response: Sarah might consider rebalancing to 50% stocks/50% bonds to feel more comfortable.

Long-term Strategy: However, as a 30-year-old with a long time horizon, she could consider maintaining or even increasing her stock allocation.

Key Lesson: This scenario demonstrates that risk tolerance can change based on market conditions and recent experiences. It highlights the difference between temporary emotional responses and long-term capacity for risk.

Recommendation: Sarah should reassess her risk tolerance considering both her emotional comfort and long-term financial capacity, potentially maintaining a higher stock allocation while adding some stability.

This example illustrates the dynamic nature of risk tolerance. Market downturns often reveal that our perceived risk tolerance is different from our actual tolerance when faced with real losses. It's important to distinguish between temporary emotional responses and long-term financial capacity. The best approach often involves a middle ground that respects emotional comfort while maintaining long-term growth potential.

Risk Tolerance: Willingness to accept uncertainty

Emotional Response: Psychological reaction to market events

Long-term Capacity: Financial ability over extended period

• Risk tolerance can change with market conditions

• Distinguish emotional from financial capacity

• Consider time horizon in decisions

• Reassess after major market events

• Consider both emotional and financial factors

• Don't make hasty changes during stress

• Panicking and selling during downturns

• Not reassessing risk tolerance

• Ignoring long-term perspective

You've been investing with an aggressive risk tolerance profile for 10 years. Now you're getting married and expecting your first child. How should you reassess your risk tolerance and adjust your investment strategy? Consider both the emotional and financial impacts of this life change.

Financial Impact: New family responsibilities may reduce your financial capacity to take risk, as you now have dependents to support.

Emotional Impact: Responsibility for family welfare may decrease your emotional comfort with risk.

Strategy Adjustment: Consider shifting from aggressive to moderate profile, perhaps reducing stock allocation from 85% to 70% and increasing bonds.

Long-term Planning: Factor in future expenses (education, healthcare) and adjust accordingly.

Communication: Discuss investment philosophy with your partner to ensure alignment.

Major life events significantly impact risk tolerance by changing both financial capacity and emotional comfort levels. Having dependents introduces new financial responsibilities that reduce the ability to take risk. It's crucial to reassess risk tolerance after significant life changes and adjust investment strategies accordingly. This doesn't necessarily mean becoming conservative, but rather finding an appropriate balance for the new life stage.

Life Events: Major changes affecting financial circumstances

Family Responsibilities: Financial obligations to dependents

Investment Philosophy: Approach to investment decision-making

• Reassess risk tolerance after life changes

• Consider impact on dependents

• Align strategies with new goals

• Plan for family-related expenses

• Discuss investments with partner

• Gradually adjust allocation

• Not reassessing after life changes

• Maintaining same risk level despite new responsibilities

• Not involving partner in decisions

Which psychological bias most commonly causes investors to have an inaccurate assessment of their risk tolerance?

Recency bias is the tendency to give disproportionate weight to recent events when making decisions. In risk tolerance assessment, investors often overestimate their risk tolerance during bull markets (when recent returns have been positive) and underestimate it during bear markets (when recent losses have occurred). This leads to inaccurate self-assessment that doesn't reflect true long-term risk tolerance.

The answer is C) Recency bias.

Recency bias significantly impacts risk tolerance assessment because it causes investors to base their risk preferences on recent market experiences rather than their long-term capacity and comfort. During market highs, investors feel more confident and willing to take risk, while during downturns they become overly cautious. This bias can lead to poor timing decisions and inappropriate asset allocation based on temporary market conditions rather than long-term investment needs.

Recency Bias: Giving more weight to recent events

Behavioral Finance: Study of psychological influences on investing

Cognitive Bias: Systematic error in thinking

• Assess risk tolerance during calm markets

• Consider long-term perspective

• Be aware of psychological biases

• Reassess during stable periods

• Consider historical market cycles

• Focus on long-term goals

• Making decisions based on recent performance

• Not considering full market cycles

• Ignoring psychological influences

FAQ

Q: How often should I reassess my risk tolerance?

A: Risk tolerance should be reassessed regularly:

Major Life Events: Marriage, birth of children, divorce, job changes, inheritance, etc. These should trigger immediate reassessment.

Regular Reviews: At minimum, review annually during portfolio rebalancing.

Market Extremes: After significant market movements (both positive and negative), reassess your comfort level.

Age Milestones: Every 5-10 years, consider age-appropriate adjustments to risk level.

Financial Changes: Significant changes in income, expenses, or net worth warrant reassessment.

The key is to reassess proactively rather than reactively during stressful market conditions.

Q: Can my risk tolerance be too high or too low?

A: Yes, both scenarios present problems:

Risk Tolerance Too High:

• May lead to excessive risk-taking beyond financial capacity

• Could result in panic selling during market downturns

• Might cause emotional stress affecting decision-making

Risk Tolerance Too Low:

• May not generate sufficient returns to meet long-term goals

• Could result in missing out on growth opportunities

• Might lead to inflation risk (losing purchasing power)

The goal is finding the optimal balance between risk and return that aligns with your comfort level and financial objectives.

Q: How do I know if I'm really comfortable with risk or just think I am?

A: Distinguishing true risk tolerance from perceived tolerance requires careful observation:

True Risk Tolerance Signs:

• Remain calm during market volatility

• Don't make impulsive decisions during downturns

• Can sleep well knowing portfolio fluctuates

• Stick to long-term investment plan

Perceived Tolerance Signs:

• Anxiety during market declines

• Constantly checking portfolio value

• Temptation to make changes during stress

• Regret after market losses

Testing Method: Consider how you felt during the 2008 financial crisis or March 2020 market crash. This often reveals true risk tolerance.