How Much Should I Save Each Month?

Complete monthly savings guide • Step-by-step explanations

Monthly Savings Fundamentals:

Show Savings CalculatorDetermining how much to save each month requires understanding your financial goals, current expenses, and income. The key is to establish a sustainable savings rate that balances immediate needs with long-term financial security. A good starting point is the 50/30/20 rule: 50% for needs, 30% for wants, and 20% for savings and debt repayment.

Key factors for determining monthly savings:

- Emergency Fund: 3-6 months of living expenses

- Retirement Goals: 10-15% of income for retirement savings

- Specific Goals: Vacation, home down payment, education

- Age and Life Stage: Younger adults can save more aggressively

- Income Stability: Higher stability allows for more aggressive savings

With proper planning and consistent execution, you can achieve significant financial milestones.

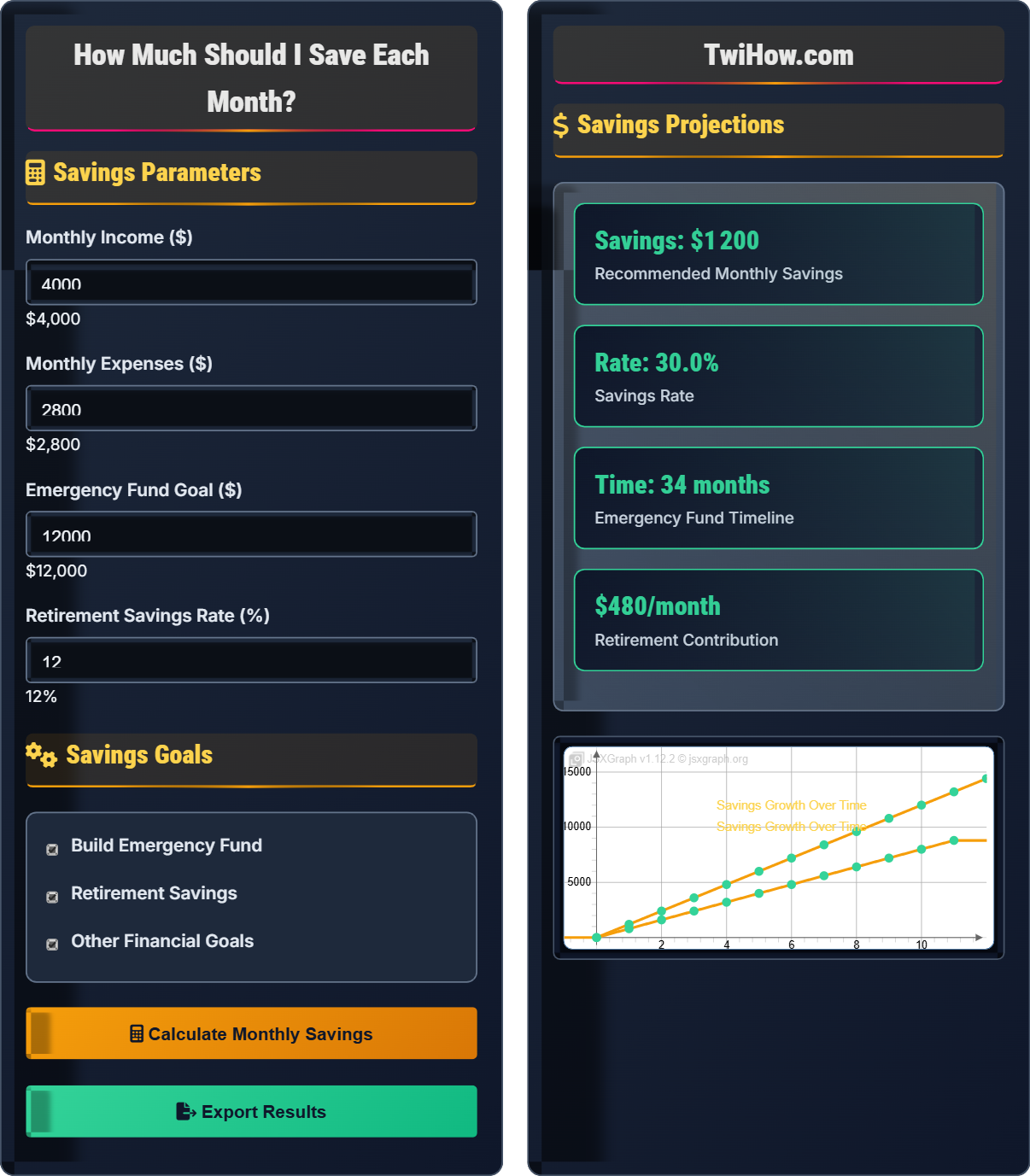

Savings Parameters

Savings Goals

Savings Projections

| Category | Amount | Percentage | Timeline |

|---|---|---|---|

| Emergency Fund | $300 | 7.5% | 40 months |

| Retirement | $480 | 12% | Ongoing |

| Other Goals | $20 | 0.5% | Varies |

| Total | $800 | 20% | Ongoing |

How Much Should I Save Each Month?

Determining how much to save each month requires understanding your financial goals, current expenses, and income. The key is to establish a sustainable savings rate that balances immediate needs with long-term financial security. A good starting point is the 50/30/20 rule: 50% for needs, 30% for wants, and 20% for savings and debt repayment.

Effective monthly savings follow a simple mathematical principle:

Where:

- Monthly Income: Your total monthly earnings

- Monthly Expenses: Your total monthly expenditures

- Monthly Savings: The difference that goes into savings

- Goal: Maximize the difference through optimization

Your savings rate determines how quickly you'll reach your financial goals:

Where:

- Monthly Savings: Amount saved per month

- Monthly Income: Total monthly income

- Savings Rate: Percentage of income saved

A proven budgeting strategy for sustainable savings:

- 50% Needs: Housing, utilities, food, transportation

- 30% Wants: Entertainment, dining out, hobbies

- 20% Savings: Emergency fund, investments, debt repayment

Adjust these percentages based on your financial situation and goals.

Key areas for monthly savings allocation:

- Emergency Fund: 3-6 months of expenses for unexpected events

- Retirement: Long-term savings for financial independence

- Short-term Goals: Vacations, home down payment, education

- Investment: Building wealth through stocks, bonds, or real estate

- Debt Repayment: Paying down high-interest debt

Monthly Savings Fundamentals

Budgeting, expense tracking, emergency fund, retirement savings, compound interest, financial goals.

\(\text{Savings Rate} = \frac{\text{Monthly Savings}}{\text{Monthly Income}} \times 100\%\)

Where savings rate represents the percentage of income saved monthly.

- Pay yourself first by automating savings

- Build emergency fund before investing

- Maximize employer 401(k) match

Allocation Strategies

50/30/20 rule, emergency fund, retirement accounts, goal-based savings, debt repayment.

- Emergency fund (3-6 months)

- Retirement (10-15% of income)

- Other goals (5-10% of income)

- Investments (remaining amount)

- Adjust based on age and life stage

- Consider tax implications

- Account for inflation

Monthly Savings Learning Quiz

According to financial experts, what is the recommended minimum savings rate for financial stability?

Financial experts generally recommend saving at least 20% of your income for financial stability. This follows the 50/30/20 rule where 50% goes to needs, 30% to wants, and 20% to savings and debt repayment. While any amount is better than nothing, 20% provides a solid foundation for building wealth and preparing for emergencies.

The answer is C) 20%.

The 20% savings rate is a benchmark that balances financial security with lifestyle. It's designed to be achievable for most people while still building meaningful wealth over time. The key insight is that even small adjustments to your spending habits can help you reach this target. For example, reducing dining out by $200/month or canceling unused subscriptions can make a significant difference in your ability to save.

Savings Rate: Percentage of income saved monthly

50/30/20 Rule: Budgeting guideline for income allocation

Emergency Fund: Savings for unexpected expenses

• Start with any amount if 20% is too high

• Automate savings to make it consistent

• Build emergency fund first

• Round up purchases to nearest dollar and save difference

• Use windfalls for savings boost

• Start with 5% and gradually increase

• Waiting to save until bills are paid

• Not having a specific savings goal

• Spending windfalls instead of saving them

Explain the purpose of an emergency fund and calculate how much should be saved based on monthly expenses. How does this affect your monthly savings target?

Purpose of Emergency Fund: An emergency fund provides financial security for unexpected events like job loss, medical expenses, or major repairs. It prevents you from going into debt during crises and gives peace of mind.

Recommended Amount: 3-6 months of essential expenses (not wants). For someone with $3,000 monthly expenses, the emergency fund should be $9,000-$18,000.

Calculation Example:

Monthly expenses: $3,000

Target emergency fund: $3,000 × 4 months = $12,000

If you have $2,000 saved, you need $10,000 more.

At $500/month, it takes 20 months to build.

Effect on Monthly Savings: Building an emergency fund should be your first priority. Once established, you can allocate those funds toward other goals. The emergency fund portion of your monthly savings is temporary but essential.

The emergency fund is the foundation of financial security. Think of it as a financial cushion that protects you from falling into debt when unexpected expenses arise. The 3-6 month rule is based on the average time it takes to find a new job if you lose yours. Once you have this buffer, you can confidently pursue other financial goals knowing you're protected against life's surprises.

Emergency Fund: Savings for unexpected expenses

Essential Expenses: Necessary monthly costs

Financial Security: Buffer against unexpected events

• Keep emergency fund in liquid accounts

• Don't invest emergency fund in volatile assets

• Replenish after use

• Start with $1,000 emergency fund

• Use high-yield savings accounts

• Don't touch except for true emergencies

• Not having an emergency fund

• Using emergency fund for non-emergencies

• Investing emergency fund in risky assets

John is 30 years old with a monthly income of $5,000. He wants to retire at 65 with $1.5 million in savings. Calculate how much he should save monthly for retirement if he expects a 7% annual return. How does this fit into his overall monthly savings plan?

Retirement Savings Calculation:

Using the future value of an annuity formula:

FV = PMT × [((1 + r)^n - 1) / r]

Where: FV = $1,500,000, r = 0.07/12 = 0.00583, n = 35 × 12 = 420 months

Solving for PMT:

$1,500,000 = PMT × [((1.00583)^420 - 1) / 0.00583]

$1,500,000 = PMT × 1,517.62

PMT = $989 per month

Overall Savings Plan:

Monthly income: $5,000

Retirement savings: $989 (19.8%)

Emergency fund: $500 (10%)

Total savings: $1,489 (29.8%)

John should save approximately $989 monthly for retirement, which represents about 20% of his income. Combined with an emergency fund contribution, he should aim for about 30% of his income in savings, which is above the recommended 20% and appropriate for his ambitious retirement goal.

This problem demonstrates the power of compound interest and the importance of starting early. John's goal of $1.5 million in 35 years requires a significant monthly contribution, but starting at 30 gives him the time needed for compound growth. The key insight is that the earlier you start saving for retirement, the less you need to save each month due to the compounding effect.

Future Value: Value of an investment at a future date

Compound Interest: Interest earned on previous interestTime Value of Money: Money available now is worth more than later

• Start retirement savings as early as possible

• Take advantage of employer matching

• Increase contributions with raises

• Maximize 401(k) employer match first

• Consider Roth IRA for tax diversification

• Increase contributions by 1% annually

• Starting retirement savings too late

• Not taking advantage of employer match

• Being too conservative with investments

You currently spend $3,500/month with $4,500/month income. Your largest expenses are: Rent ($1,400), Food ($600), Transportation ($400), Entertainment ($500), and Other ($600). Design a strategy to increase your monthly savings from $1,000 to $1,500. Which expenses would you target and by how much?

Current Situation:

Monthly income: $4,500

Monthly expenses: $3,500

Current savings: $1,000 (22.2%)

Target savings: $1,500 (33.3%)

Additional savings needed: $500

Strategy for $500 Additional Monthly Savings:

1. Entertainment Reduction ($150): Cut from $500 to $350 by choosing free activities, limiting dining out, and using streaming instead of cable.

2. Food Reduction ($150): Reduce from $600 to $450 by meal planning, cooking at home, and buying generic brands.

3. Transportation Reduction ($100): Cut from $400 to $300 by carpooling, using public transport, or negotiating car insurance.

4. Other Expenses ($100): Reduce miscellaneous spending from $600 to $500 by being more mindful of purchases.

Result: New expenses: $3,000, New savings: $1,500 (33.3% savings rate)

This strategy maintains quality of life while significantly increasing savings.

This problem demonstrates the importance of targeting the largest expenses for maximum impact. Entertainment, food, and transportation are often the most flexible categories for reduction. The key is making sustainable changes that you can maintain long-term. Small changes in multiple categories are often more effective than drastic cuts in one area that you can't maintain.

Budget Optimization: Improving budget efficiency

Expense Categories: Groupings of similar expenses

Disposable Income: Income after essential expenses

• Focus on largest expense categories first

• Maintain quality of life while saving

• Make changes sustainable long-term

• Use the 50/30/20 rule as a baseline

• Set up automatic savings transfers

• Track progress weekly

• Cutting expenses too drastically to maintain

• Not accounting for occasional expenses

• Forgetting to adjust budget for life changes

How should your monthly savings rate change as you progress through different life stages?

Your monthly savings rate should generally increase with age as your earning potential rises and expenses stabilize. Young adults should aim for 15-20% of income, while those in their 40s and 50s should consider saving 20-30% to catch up for retirement. The key is to increase savings rates when you get raises or pay off major expenses like mortgages.

The answer is C) Increase with age as earning potential rises.

The optimal savings rate changes throughout life based on earning potential and financial responsibilities. Early career: 15-20% (lower income, higher debt). Peak earning years: 20-30% (higher income, fewer dependents). Pre-retirement: 15-25% (maximize retirement contributions). The key principle is to increase your savings rate when your income increases, not just your lifestyle.

Life Stage Planning: Adjusting finances for different life phases

Earning Potential: Expected income over career

Financial Responsibilities: Obligations affecting savings

• Increase savings rate with income increases

• Adjust for life stage needs

• Maximize savings during peak earning years

• Automate savings increases with raises

• Adjust for major life events

• Plan for different life stage needs

• Maintaining same savings rate throughout career

• Not adjusting for changing expenses

• Lifestyle inflation with income increases

FAQ

Q: How can I save money when I'm just starting my career and have a low salary?

A: Even with a low salary, starting early gives you the advantage of compound growth:

Start Small: Begin with 5-10% of your income, even if it's just $50-100/month. The habit is more important than the amount initially.

Automate: Set up automatic transfers to make saving effortless.

Focus on Essentials: Live below your means by choosing affordable housing, transportation, and lifestyle options.

Take Advantage of Employer Benefits: Maximize any employer 401(k) match immediately.

Invest in Yourself: Use early career years to develop skills that will increase your earning potential.

Remember, saving 5% of a low salary is better than saving 0% of a higher salary later.

Q: What's the difference between saving and investing, and how should I allocate my monthly savings?

A: The key differences are:

Saving: Preserving money for short-term goals and emergencies. Uses safe, liquid accounts like savings accounts, CDs, or money market funds. Offers lower returns but principal protection.

Investing: Growing money for long-term goals. Uses stocks, bonds, mutual funds, or real estate. Offers higher potential returns but with more risk.

Monthly Allocation Strategy:

Emergency Fund (3-6 months): Keep in high-yield savings account

Short-term Goals (1-3 years): Use CDs or money market accounts

Long-term Goals (5+ years): Invest in diversified portfolios

General Rule: Keep 1-2 years of expenses in savings/investments that are easily accessible, with the rest in long-term investments.