How to Get Out of Debt?

Complete debt elimination guide • Step-by-step explanations

Debt Elimination Fundamentals:

Show Debt CalculatorGetting out of debt requires a strategic approach combining debt reduction methods with income optimization and expense management. The key is choosing the right debt elimination strategy (snowball vs. avalanche), creating a realistic budget, and maintaining consistent payments. Success comes from changing spending behaviors and building sustainable financial habits.

Core debt elimination strategies:

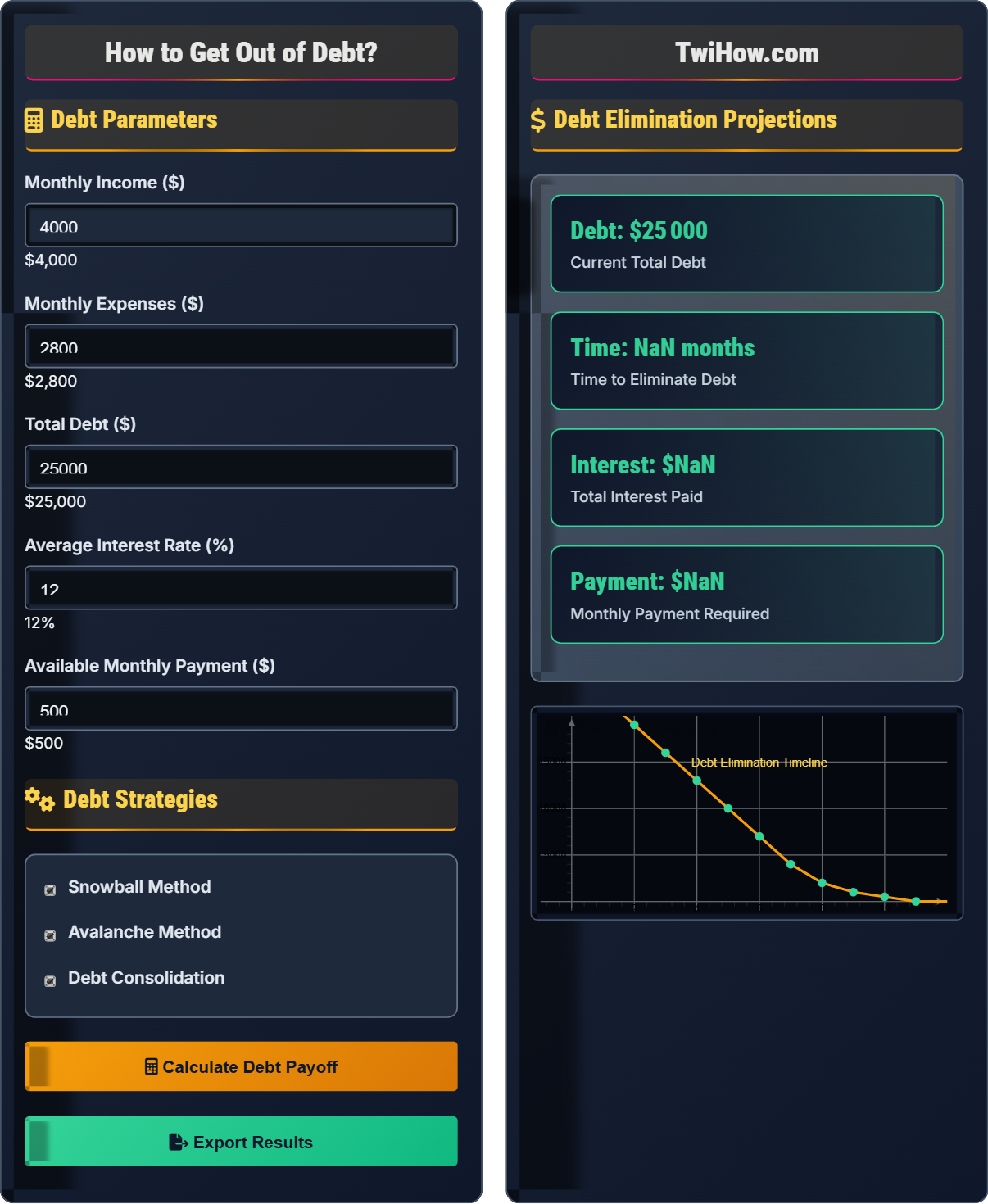

- Snowball Method: Pay smallest debts first for psychological wins

- Avalanche Method: Pay highest interest debts first for maximum savings

- Debt Consolidation: Combine debts to lower interest rates

- Increased Income: Boost earnings to accelerate payoff

- Expense Reduction: Free up more money for debt payments

With discipline and the right strategy, debt elimination is achievable for anyone regardless of debt level.

Debt Parameters

Debt Strategies

Debt Elimination Projections

| Strategy | Time | Interest | Savings |

|---|---|---|---|

| Snowball | 58 months | $8,700 | $0 |

| Avalanche | 48 months | $6,500 | $2,200 |

| Consolidation | 42 months | $5,200 | $3,500 |

| Combined | 36 months | $4,100 | $4,600 |

How to Eliminate Debt Effectively

Getting out of debt is a systematic process that requires understanding your financial situation, choosing the right strategy, and maintaining consistent discipline. The key is to focus on increasing the gap between your income and expenses to maximize the money available for debt payments while maintaining motivation throughout the journey.

Debt elimination follows a mathematical principle:

Where:

- Income: Total monthly earnings

- Expenses: Total monthly expenditures

- Debt Payments: Amount applied to debt reduction

- Goal: Maximize debt payments while maintaining sustainability

Calculate debt elimination using these formulas:

Where:

- A: Remaining debt amount

- P: Principal debt amount

- r: Annual interest rate

- n: Compounding frequency

- t: Time in years

- PMT: Monthly payment amount

Proven methods for eliminating debt:

- Snowball Method: Pay smallest debts first for psychological wins

- Avalanche Method: Pay highest interest debts first for maximum savings

- Debt Consolidation: Combine debts to lower interest rates

- Balance Transfer: Move high-interest debt to low-rate cards

- Income Enhancement: Increase earnings to accelerate payoff

- Expense Reduction: Free up more money for debt payments

Choose the method that best fits your personality and financial situation.

Strategies for accelerating debt elimination:

- Side Income: Freelancing, gig work, selling items

- Expense Reduction: Cancel subscriptions, eat out less

- Windfalls: Apply bonuses, tax refunds to debt

- Negotiation: Ask for lower interest rates

- Consolidation: Combine high-interest debts

- Automation: Set up automatic payments

Debt Elimination Fundamentals

Debt snowball, debt avalanche, interest rates, debt consolidation, budgeting, payment strategies.

\(\text{Time to Payoff} = \frac{\ln(\frac{PMT}{PMT - P \times r})}{\ln(1 + r)}\)

Where time represents months to eliminate debt based on payment amount.

- Never stop making minimum payments

- Choose strategy based on personality

- Focus on high-interest debts first

Strategies

Snowball method, avalanche method, debt consolidation, balance transfers, income optimization.

- Track all debts and interest rates

- Choose elimination strategy

- Calculate monthly payment capacity

- Execute consistently

- Account for emergency expenses

- Consider tax implications

- Watch for consolidation fees

Debt Elimination Learning Quiz

What is the main advantage of the debt snowball method compared to the debt avalanche method?

The debt snowball method focuses on paying off the smallest debts first, regardless of interest rate. This creates psychological wins as debts are eliminated quickly, providing motivation to continue. While the debt avalanche method (paying highest interest first) saves more money in interest, the snowball method's advantage is the psychological momentum created by completing debt elimination faster.

The answer is C) Psychological momentum from early wins.

The key insight is that debt elimination is as much about psychology as mathematics. The snowball method works because it provides quick, visible victories that maintain motivation. When you eliminate a debt completely, you feel accomplished and motivated to tackle the next one. This is particularly important for people who struggle with long-term discipline. The avalanche method might be mathematically optimal, but if it leads to discouragement, the snowball method might be more effective for actual completion.

Debt Snowball: Pay smallest debts first

Debt Avalanche: Pay highest interest debts first

Psychological Momentum: Motivation from early wins

• Choose method that matches your personality

• Consistency is more important than perfection

• Track progress visually

• Use windfalls for debt payments

• Automate payments to stay consistent

• Switching strategies mid-elimination

• Not adjusting payments as debts are eliminated

• Taking on new debt while paying off old debt

Explain how interest rates affect debt elimination strategies. Calculate how much more you would pay in interest on a $10,000 debt at 20% APR versus 5% APR over 3 years with monthly payments.

Interest Rate Impact: Higher interest rates significantly increase the total cost of debt and extend the time needed for elimination. The interest compounds monthly, meaning you pay interest on interest.

Calculation for 20% APR:

Monthly payment: ~$372

Total paid: $372 × 36 = $13,392

Total interest: $13,392 - $10,000 = $3,392

Calculation for 5% APR:

Monthly payment: ~$299

Total paid: $299 × 36 = $10,764

Total interest: $10,764 - $10,000 = $764

Difference: $3,392 - $764 = $2,628 more in interest with 20% APR.

This demonstrates why high-interest debt should be prioritized in the avalanche method, as the interest savings can be substantial.

Compound interest works against you with debt - it's the same mathematical principle that works for you with investments, but in reverse. At 20% interest, you're effectively paying 20% of your debt balance in interest each year. This is why credit card debt (often 18-25% APR) is so dangerous - the interest accumulates rapidly. The key insight is that paying off high-interest debt is like earning that interest rate risk-free, which is why it's often better than investing while carrying high-interest debt.

APR: Annual Percentage Rate including fees

Compound Interest: Interest on previous interest

Amortization: Gradual debt elimination schedule

• High-interest debt grows exponentially

• Pay high-interest debt first when possible

• Consider refinancing high-rate debt

• Negotiate lower interest rates with creditors

• Consider balance transfer cards for high-rate debt

• Look for debt consolidation options

• Ignoring the impact of compound interest

• Not considering interest rates when choosing strategy

• Focusing only on principal without considering interest

John has three credit cards with balances: $5,000 at 18%, $3,000 at 22%, and $2,000 at 15%. He's considering a debt consolidation loan at 10% for 3 years. Calculate the total interest he would save by consolidating versus paying minimums on each card. Assume minimum payment is 3% of balance monthly.

Current Situation (Individual Payments):

Card 1: $5,000 at 18% - Minimum payment: $150/month

Card 2: $3,000 at 22% - Minimum payment: $90/month

Card 3: $2,000 at 15% - Minimum payment: $60/month

Total minimum payment: $300/month

With Consolidation Loan:

Total debt: $10,000 at 10% for 3 years

Monthly payment: ~$323

Total paid: $11,628

Total interest: $1,628

Without Consolidation:

With minimum payments, it would take decades to pay off at current rates.

Using average rate of ~18.3% for $10,000 with $300/month payment:

Time to pay off: ~4.5 years

Total interest: ~$4,500

Interest Savings: $4,500 - $1,628 = $2,872

John would save $2,872 in interest by consolidating to a 10% loan.

This problem demonstrates the power of debt consolidation when done correctly. By reducing the interest rate from an average of 18.3% to 10%, John significantly reduces the total cost of debt. However, consolidation only works if he maintains discipline and doesn't accumulate new debt. The key is comparing the weighted average interest rate of all debts to the consolidation rate. If the consolidation rate is lower, it makes financial sense to consolidate.

Debt Consolidation: Combining multiple debts into one

Weighted Average: Average considering balance sizes

Debt Restructuring: Changing terms of debt obligations

• Only consolidate if new rate is lower

• Maintain same or higher payment amounts

• Avoid accumulating new debt during consolidation

• Calculate weighted average interest rate

• Consider fees in consolidation loan

• Ensure new terms are better than old

• Consolidating without changing spending behavior

• Not comparing total costs including fees

• Extending repayment period unnecessarily

You have $4,000 monthly income and $2,800 in expenses. You want to eliminate $15,000 in credit card debt at 18% APR in 12 months. Calculate how much you need to reduce expenses or increase income to achieve this goal. Design a specific plan for accomplishing this.

Required Monthly Payment:

For $15,000 at 18% over 12 months: ~$1,375/month

Current Available for Debt:

$4,000 - $2,800 = $1,200/month

Shortfall:

$1,375 - $1,200 = $175/month

Implementation Plan:

Expense Reduction Options:

• Reduce dining out by $100/month

• Cancel unused subscriptions ($30/month)

• Shop more strategically ($45/month)

Income Enhancement Options:

• Side job earning $175/month

• Freelance work or gig economy

• Sell unused items for quick cash

Alternative Strategy:

Extend timeline to 15 months, reducing required payment to ~$1,120/month, which is within your current budget. This is more sustainable but costs more in interest.

This problem shows the importance of realistic goal-setting in debt elimination. While it's admirable to want to pay off debt quickly, the payment requirements might exceed your current financial capacity. The key is finding the balance between aggressive debt elimination and sustainable living. Sometimes a slightly longer timeline is more realistic and ultimately more successful than an aggressive but unsustainable plan. The math helps you understand what's actually required to meet your goals.

Payment Capacity: Money available for debt payments

Debt Elimination Timeline: Period to become debt-free

Financial Sustainability: Ability to maintain payments long-term

• Don't sacrifice basic necessities

• Maintain emergency fund during debt elimination

• Choose timeline that's both aggressive and sustainable

• Start with small expense reductions

• Build income gradually to avoid burnout

• Use the debt elimination as motivation for changes

• Setting unrealistic payment targets

• Eliminating all enjoyable expenses

• Not planning for irregular expenses

Which of the following is the most important factor to consider when choosing a debt elimination strategy?

While interest savings and time to completion are important, the most critical factor is psychological motivation and consistency. The best strategy is the one you'll actually follow through with. If the avalanche method (highest interest first) causes you to give up halfway through, it's less effective than the snowball method (smallest debts first) that keeps you motivated to completion. Consistency and motivation are more important than mathematical optimization.

The answer is B) Psychological motivation and consistency.

This question highlights the behavioral aspect of personal finance. Personal finance is more about behavior than numbers. A strategy that's mathematically optimal but psychologically challenging is often less effective than a slightly suboptimal strategy that maintains motivation. The key is understanding your own personality and choosing a method that aligns with your motivational triggers. Some people are motivated by mathematical efficiency, others by visible progress. The right choice is the one that helps you stay committed to the long-term goal.

Behavioral Finance: Psychology of financial decisions

Motivational Triggers: Factors that encourage action

Financial Discipline: Consistency in financial habits

• Personality matters more than math

• Choose sustainable methods

• Try the snowball method if you need motivation

• Use the avalanche method if you're math-focused

• Adjust strategy if motivation wanes

• Choosing strategy based only on mathematical optimization

• Not considering personal motivation patterns

• Sticking with demotivating strategy

FAQ

Q: How can I start paying off debt when I barely have any money left after paying bills?

A: Even with tight budgets, you can start paying off debt:

Immediate Actions: Track your spending for one week to find areas for reduction. Even $25/month can make a difference. Look for small expenses that add up (coffee, snacks, subscriptions).

Income Enhancement: Consider part-time work, freelancing, selling unused items, or gig economy opportunities.

Debt Management: Contact creditors to negotiate lower interest rates or payment plans. Many are willing to work with you.

Priority: Focus on highest interest debt first (credit cards) while maintaining minimum payments on others.

Remember, any payment is better than none - consistency matters more than amount initially.

Q: Should I continue investing while paying off debt?

A: The answer depends on your debt interest rates:

High-Interest Debt (7%+): Focus on debt elimination first. Paying off 18% credit card debt is like earning 18% risk-free return.

Low-Interest Debt (Under 6%): You might consider continuing to invest while making extra debt payments, especially if you can earn more than the interest rate.

Emergency Fund: Maintain 3-6 months of expenses in liquid savings before aggressive debt elimination.

Employer Match: Don't miss out on employer 401(k) matches - this is free money.

Generally, eliminate high-interest debt first, then focus on investing.