How to Manage Personal Finances?

Complete personal finance guide • Step-by-step explanations

Personal Finance Fundamentals:

Show Finance CalculatorPersonal finance management involves creating a comprehensive system for tracking income, controlling expenses, saving for goals, and investing wisely. The foundation includes budgeting, debt management, emergency planning, and long-term financial goal setting. Success requires discipline, planning, and consistent execution of financial strategies.

Key personal finance components:

- Budgeting: Tracking income and expenses systematically

- Savings: Building emergency funds and achieving goals

- Debt Management: Eliminating high-interest debt efficiently

- Investing: Growing wealth through strategic investments

- Insurance: Protecting against financial risks

Effective personal finance management creates financial security and freedom to pursue life goals.

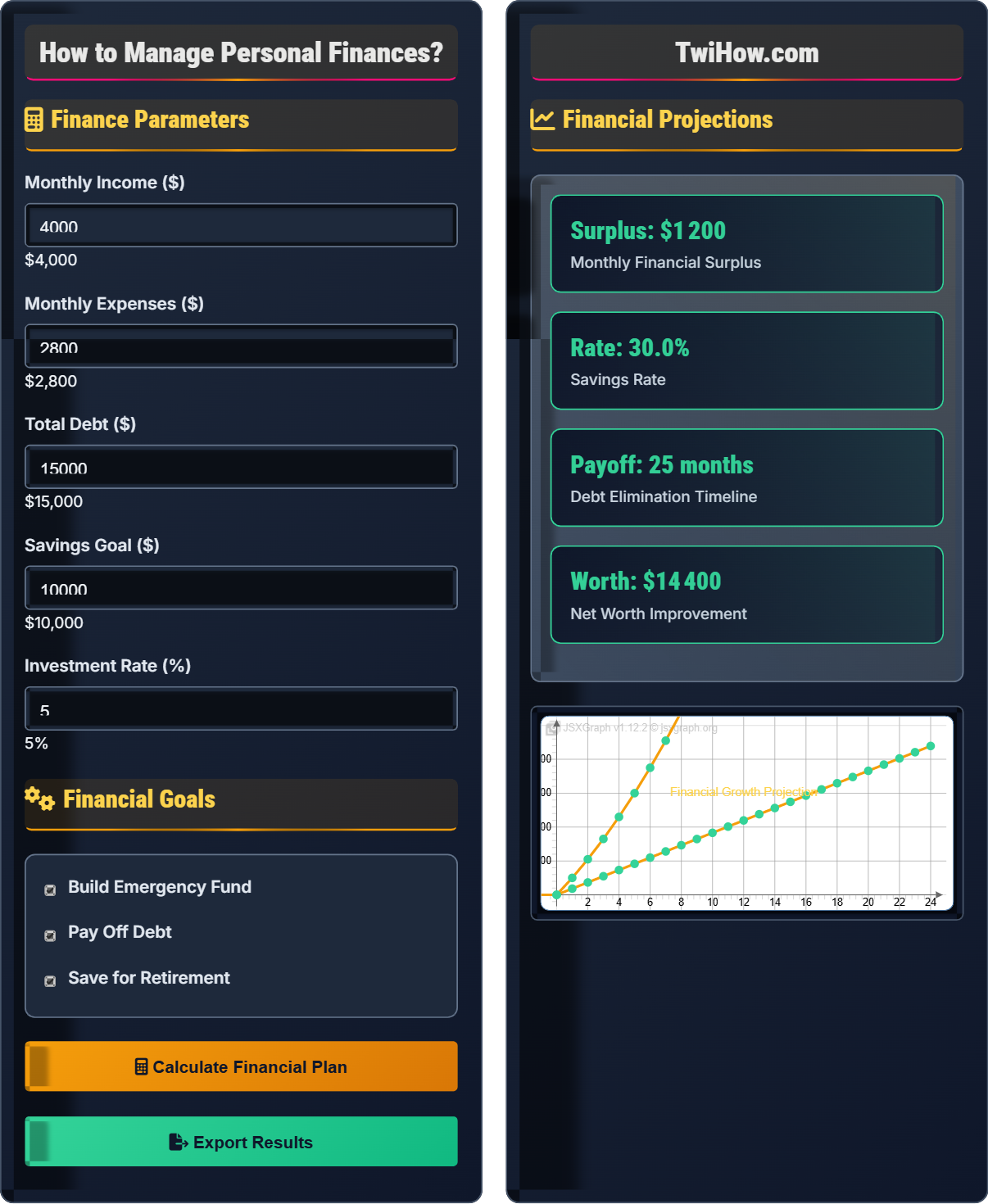

Finance Parameters

Financial Goals

Financial Projections

| Category | Amount | Percentage | Priority |

|---|---|---|---|

| Emergency Fund | $1,000 | 25% | 1 |

| Debt Payment | $800 | 20% | 2 |

| Retirement | $600 | 15% | 3 |

| Investment | $400 | 10% | 4 |

| Other Goals | $400 | 10% | 5 |

How to Manage Personal Finances

Personal finance management is the process of planning and controlling your financial resources to achieve your life goals. It involves creating a systematic approach to earning, spending, saving, and investing money. The goal is to create financial security, achieve financial goals, and build wealth over time through disciplined money management.

Successful personal finance follows a fundamental equation:

Where:

- Income: Total monthly earnings

- Needs: Essential expenses (housing, utilities, food)

- Wants: Non-essential spending (entertainment, dining)

- Savings: Money set aside for future goals

- Debt Repayment: Payments to reduce outstanding debts

A popular budgeting method that allocates income as follows:

Where:

- Needs (50%): Essential expenses for basic living

- Wants (30%): Discretionary spending for enjoyment

- Savings/Debt (20%): Savings, investments, and debt payments

Key components of effective financial planning:

- Emergency Fund: 3-6 months of expenses for unexpected events

- Debt Elimination: Systematic approach to reducing liabilities

- Goal Setting: Specific, measurable financial objectives

- Investment Strategy: Long-term wealth building approach

- Insurance Protection: Safeguarding against major risks

- Tax Optimization: Minimizing tax burden legally

Each component works together to create financial stability and growth.

Proven methods for achieving financial success:

- Automate Everything: Set up automatic savings and bill payments

- Track Expenses: Monitor spending to identify improvement areas

- Live Below Means: Spend less than you earn consistently

- Invest Early: Take advantage of compound growth

- Minimize Fees: Reduce investment and banking costs

- Stay Informed: Continuously educate yourself about finance

Personal Finance Fundamentals

Budgeting, emergency fund, debt management, investment, net worth, cash flow, financial goals.

\(\text{Cash Flow} = \text{Income} - \text{Expenses} - \text{Debt Payments}\)

Where cash flow represents the money available for savings and investment.

- Pay yourself first by automating savings

- Build emergency fund before investing

- Eliminate high-interest debt first

Strategies

50/30/20 rule, debt snowball, debt avalanche, dollar-cost averaging, compound interest.

- Budget tracking

- Expense reduction

- Income optimization

- Debt elimination

- Adjust strategies based on life stage

- Consider tax implications

- Account for inflation

Personal Finance Learning Quiz

According to financial experts, what should be your first financial priority when starting to manage personal finances?

Building an emergency fund should be your first financial priority. Financial experts recommend having 3-6 months of expenses saved before focusing on other goals. This provides a financial buffer for unexpected events like job loss or medical expenses, preventing you from going into debt during emergencies. Without this foundation, other financial goals become vulnerable to disruption.

The answer is B) Build an emergency fund.

Think of the emergency fund as the foundation of a house - you can't build the upper floors without a solid foundation. If you start investing or paying down debt without an emergency fund, a single unexpected expense (like a car repair or medical bill) could force you to abandon your financial progress. The emergency fund provides stability and allows you to pursue other financial goals with confidence that you can handle unexpected events without derailing your plan.

Emergency Fund: Savings for unexpected expenses

Financial Foundation: Basic financial stability elements

Unexpected Expenses: Unplanned financial obligations

• Emergency fund comes before investments

• Maintain liquid savings for emergencies

• Don't invest emergency fund

• Start with $1,000 emergency fund minimum

• Use high-yield savings account

• Automate emergency fund contributions

• Investing before having emergency fund

• Not adjusting fund size for circumstances

• Using emergency fund for non-emergencies

Explain the difference between the debt snowball and debt avalanche methods. When should each method be used and what are the advantages of each?

Debt Snowball Method: Pay minimum payments on all debts, then put extra money toward the smallest debt balance first. Once that debt is paid off, move to the next smallest.

Advantages: Provides psychological wins, maintains motivation, simple to understand.

Debt Avalanche Method: Pay minimum payments on all debts, then put extra money toward the debt with the highest interest rate first.

Advantages: Saves more money in interest, pays off debt faster overall.

When to Use Each:

Snowball: When you need motivation and encouragement to stay committed to debt elimination.

Avalanche: When you want to minimize total interest paid and pay off debt fastest.

Research shows that the snowball method has higher completion rates due to psychological benefits, while the avalanche method saves more money.

This question highlights the tension between mathematical optimization and behavioral psychology in personal finance. The avalanche method is mathematically superior because it eliminates interest-bearing debt faster, saving money. However, the snowball method works better for many people because it provides early wins that maintain motivation. The key insight is that the best method is the one you'll actually complete. If the psychological motivation of paying off a small debt quickly helps you stay committed to the entire process, the snowball method might be more effective for you personally, even if it costs more in interest.

Debt Snowball: Pay smallest debts first for motivation

Debt Avalanche: Pay highest interest debts first for savings

Psychological Momentum: Motivation from early successes

• Always make minimum payments on all debts

• Choose method based on personality

• Stay consistent with chosen method

• Start with whichever method feels right

• Switch methods if motivation wanes

• Use windfalls for debt payments

• Stopping payments on other debts

• Not tracking progress

• Giving up too early

Sarah has a monthly income of $5,000 and monthly expenses of $3,500. She wants to build a 6-month emergency fund. Calculate how long it will take her to build this fund if she saves her entire monthly surplus. If she wants to build it in 8 months instead, how much should she save monthly?

Current Monthly Surplus:

$5,000 (income) - $3,500 (expenses) = $1,500/month

Emergency Fund Needed:

$3,500 (monthly expenses) × 6 months = $21,000

Time to Build Fund:

$21,000 ÷ $1,500/month = 14 months

Monthly Savings for 8-Month Goal:

$21,000 ÷ 8 months = $2,625/month

Additional Required:

$2,625 - $1,500 = $1,125/month additional

Sarah would need to find an additional $1,125 per month (through expense reduction or income increase) to build her emergency fund in 8 months instead of 14 months.

This problem demonstrates the relationship between income, expenses, and savings goals. The key insight is that Sarah's current surplus of $1,500 per month is insufficient to meet her 8-month timeline goal. To achieve the faster timeline, she must either increase her income by $1,125/month or reduce her expenses by that amount. This shows how financial goals are interconnected - meeting one goal may require adjusting other aspects of your financial situation. The math helps quantify exactly how much change is needed.

Monthly Surplus: Income minus expenses

Emergency Fund: Savings for unexpected expenses

Financial Timeline: Period to achieve financial goals

• Emergency fund should cover 3-6 months of expenses

• Calculate based on expenses, not income

• Adjust timeline based on realistic surplus

• Start with smaller emergency fund (1-2 months)

• Gradually increase to full target

• Use windfalls to accelerate fund building

• Calculating emergency fund based on income instead of expenses

• Setting unrealistic timelines

• Not accounting for irregular expenses

You currently spend $4,000/month with $5,000/month income. Your largest expenses are: Rent ($1,500), Food ($800), Transportation ($600), Entertainment ($400), and Other ($700). Design a strategy to increase your monthly savings by $800. Which expenses would you target and by how much?

Current Situation:

Income: $5,000

Expenses: $4,000

Current savings: $1,000

Target savings: $1,800

Additional needed: $800

Strategy for $800 Additional Monthly Savings:

1. Food Reduction ($300): Reduce from $800 to $500 by meal planning, buying generic brands, and cooking at home more often.

2. Entertainment Reduction ($200): Cut from $400 to $200 by finding free activities, limiting dining out, and canceling unused subscriptions.

3. Transportation ($150): Reduce from $600 to $450 by carpooling, using public transport, or negotiating insurance rates.

4. Other Expenses ($150): Reduce from $700 to $550 by being more mindful of purchases and avoiding impulse buying.

Result: New expenses: $3,200, New savings: $1,800 (36% savings rate)

This strategy maintains quality of life while significantly increasing savings.

This problem demonstrates the importance of targeting the largest expense categories for maximum impact. Food and entertainment often offer the most flexibility without significantly affecting quality of life. The key is finding sustainable reductions that you can maintain long-term. The 50/30/20 rule suggests that 30% of income ($1,500) can go to wants, so Sarah has room to optimize her spending while staying within guidelines. The math shows that even modest reductions across multiple categories can create substantial savings.

Expense Optimization: Strategic reduction of spending

Budget Categories: Groupings for different expense types

Sustainable Reductions: Changes that can be maintained long-term

• Target largest expense categories first

• Make changes sustainable

• Maintain quality of life

• Track expenses to identify reduction opportunities

• Use the 50/30/20 rule as a baseline

• Implement changes gradually

• Cutting expenses too drastically to maintain

• Not considering the 50/30/20 rule

• Forgetting to account for irregular expenses

When should you start investing for retirement?

Experts generally recommend starting retirement investing as soon as possible due to the power of compound growth. If your employer offers a 401(k) match, contribute enough to get the full match first. Then, build an emergency fund while continuing to invest. For high-interest debt (above 6-7%), it may be beneficial to pay that down before investing, but for moderate interest debt, investing simultaneously can be advantageous.

The answer is C) As soon as possible, even while paying debt.

The key insight is that time is the most valuable factor in investing due to compound growth. Starting early allows your investments to grow exponentially over time. While it's important to have an emergency fund and manage high-interest debt, waiting to start investing until these are completed means missing out on years of potential growth. The optimal approach is often to start investing immediately (especially if there's an employer match), build an emergency fund, and then focus intensively on debt elimination. This way, you benefit from both investment growth and debt reduction.

Compound Growth: Earnings on previous earnings

Time Value of Money: Money available now is worth more than later

Employer Match: Company contribution to retirement account

• Time is the most valuable investment factor

• Balance investing with emergency fund building

• Start with small amounts to build the habit

• Use automatic contributions

• Choose low-cost index funds

• Waiting until debt is completely paid off

• Not taking advantage of employer matches

• Starting too late in life

FAQ

Q: How can I start managing my finances when I have a very low income?

A: Managing finances on a low income requires starting small and being consistent:

Track Expenses: Even if you only make $1,000/month, track where every dollar goes. Use a simple notebook or app.

Start Small: Begin by saving just $10-25/month. The habit is more important than the amount initially.

Focus on Essentials: Prioritize needs over wants and look for ways to reduce costs (generic brands, public transport).

Build Skills: Invest in education or training that can increase your earning potential.

Take Advantage of Programs: Use employer benefits like 401(k) matches, even if small.

Remember, financial management is about making the most of what you have, regardless of the amount.

Q: What's the difference between good debt and bad debt?

A: The distinction between good and bad debt is based on potential for appreciation and income generation:

Good Debt: Debt that potentially increases your net worth or generates income. Examples: mortgages (for appreciating property), student loans (for education that increases earning potential), business loans (for income-generating ventures).

Bad Debt: Debt for depreciating assets or consumption that doesn't provide long-term value. Examples: credit card debt, car loans, payday loans.

Key Factor: Whether the debt creates assets that grow in value or generate income. The same loan can be good or bad depending on its purpose and your financial situation.