How to Save Money Fast?

Complete money saving guide • Step-by-step explanations

Money Saving Fundamentals:

Show Savings CalculatorSaving money fast requires a strategic approach that combines immediate expense reduction with income optimization. The key is to identify quick wins in your budget, eliminate unnecessary spending, and implement systematic savings methods. Success comes from combining discipline with smart financial strategies.

Key fast-saving methods:

- Emergency Fund: Set aside 3-6 months of expenses

- Budget Tracking: Monitor income and expenses closely

- Expense Cuts: Reduce subscriptions, dining out, and luxury purchases

- Income Boost: Side jobs, selling items, freelancing

- Automated Savings: Set up automatic transfers

With proper planning and execution, you can significantly increase your savings in a short timeframe.

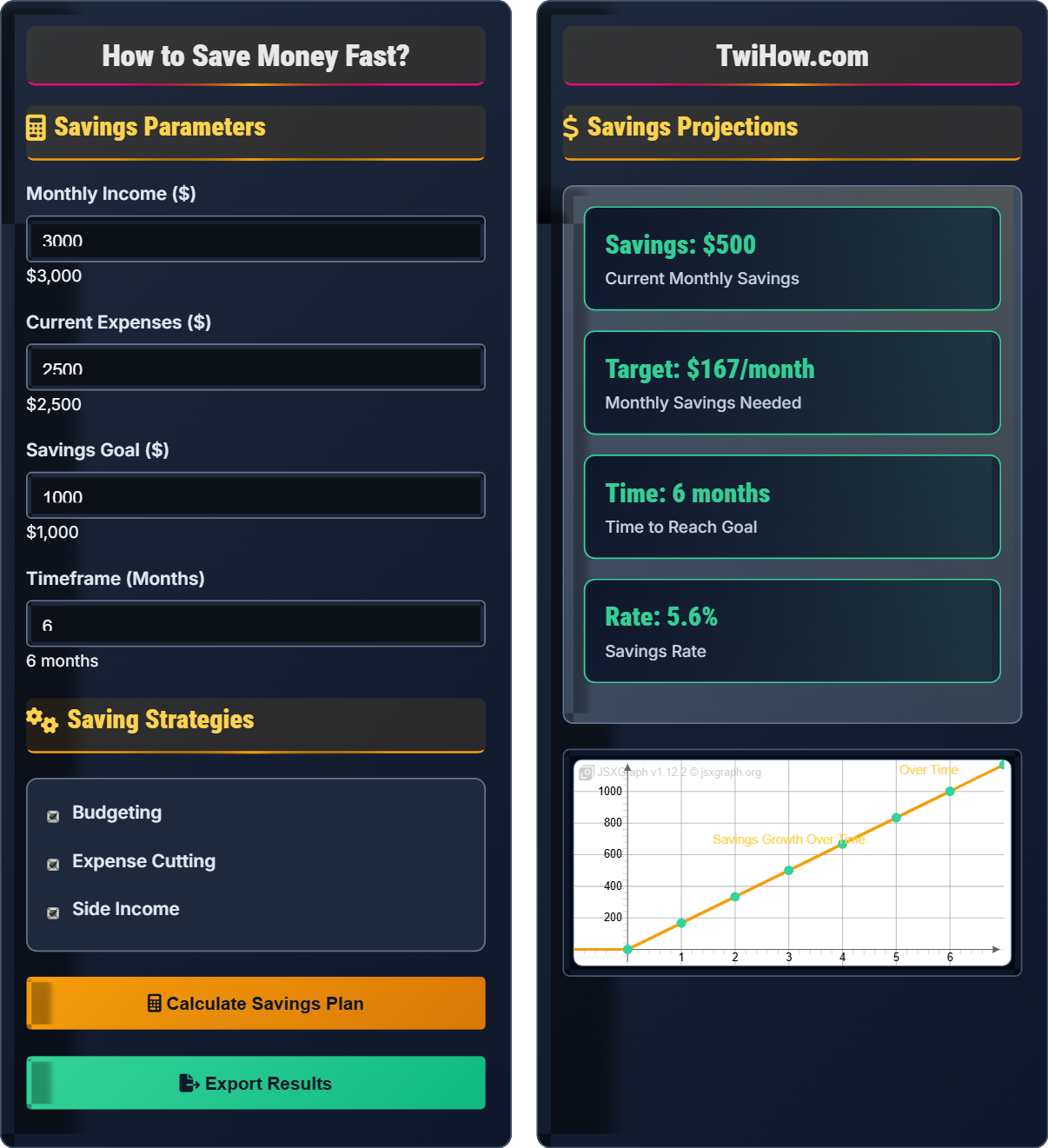

Savings Parameters

Saving Strategies

Savings Projections

| Category | Current | After Changes | Difference |

|---|---|---|---|

| Income | $3,000 | $3,200 | +$200 |

| Expenses | $2,500 | $2,200 | -$300 |

| Savings | $500 | $1,000 | +$500 |

| Savings Rate | 16.7% | 31.2% | +14.5% |

How to Save Money Fast

Saving money fast requires a systematic approach that focuses on increasing the gap between your income and expenses. The key is to identify immediate opportunities for expense reduction and income enhancement while establishing sustainable long-term habits.

Effective savings follow a simple mathematical principle:

Where:

- Income: Your total monthly earnings

- Expenses: Your total monthly expenditures

- Savings: The difference that goes into savings

- Goal: Maximize the difference through optimization

Your savings rate determines how quickly you'll reach your financial goals:

Where:

- Monthly Savings: Amount saved per month

- Monthly Income: Total monthly income

- Savings Rate: Percentage of income saved

A proven budgeting strategy for fast savings:

- 50% Needs: Housing, utilities, food, transportation

- 30% Wants: Entertainment, dining out, hobbies

- 20% Savings: Emergency fund, investments, debt repayment

Adjust these percentages based on your financial situation to accelerate savings.

Key areas for immediate savings impact:

- Subscription Audit: Cancel unused services

- Food Savings: Meal planning and bulk buying

- Utility Reduction: Energy conservation

- Shopping Strategy: Use coupons and compare prices

- Side Income: Freelancing, gig economy, selling items

Money Saving Fundamentals

Budgeting, expense tracking, emergency fund, compound interest, financial goals, debt management.

\(\text{Savings Rate} = \frac{\text{Monthly Savings}}{\text{Monthly Income}} \times 100\%\)

Where savings rate represents the percentage of income saved monthly.

- Pay yourself first by automating savings

- Track expenses to identify spending patterns

- Build an emergency fund before investing

Strategies

Budgeting, expense cutting, side income, automated savings, debt reduction, investment strategies.

- Track expenses

- Reduce subscriptions

- Meal prep

- Side hustles

- Balance saving with quality of life

- Consider tax implications

- Account for inflation

Money Saving Learning Quiz

According to financial experts, what is the recommended minimum savings rate for financial stability?

Financial experts generally recommend saving at least 20% of your income for financial stability. This follows the 50/30/20 rule where 50% goes to needs, 30% to wants, and 20% to savings and debt repayment. While any amount is better than nothing, 20% provides a solid foundation for building wealth and preparing for emergencies.

The answer is C) 20%.

The 20% savings rate is a benchmark that balances financial security with lifestyle. It's designed to be achievable for most people while still building meaningful wealth over time. The key insight is that even small adjustments to your spending habits can help you reach this target. For example, reducing dining out by $200/month or canceling unused subscriptions can make a significant difference in your ability to save.

Savings Rate: Percentage of income saved monthly

50/30/20 Rule: Budgeting guideline for income allocation

Emergency Fund: Savings for unexpected expenses

• Start with any amount if 20% is too high

• Automate savings to make it consistent

• Build emergency fund first

• Round up purchases to nearest dollar and save difference

• Use windfalls for savings boost

• Start with 5% and gradually increase

• Waiting to save until bills are paid

• Not having a specific savings goal

• Spending windfalls instead of saving them

Explain the importance of expense tracking and describe three effective methods for tracking expenses. How does this help in saving money faster?

Importance of Expense Tracking: Expense tracking reveals spending patterns you may not be aware of and identifies areas where you can cut costs. Many people underestimate their spending, especially on small, frequent purchases that add up over time.

Three Effective Methods:

1. Mobile Apps: Use apps like Mint, YNAB, or PocketGuard to automatically track transactions and categorize expenses. These apps connect to your bank accounts and provide real-time spending insights.

2. Manual Tracking: Keep receipts and record expenses in a notebook or spreadsheet. This method increases awareness of each purchase and forces you to think about spending.

3. Envelope Method: Allocate cash for different expense categories each month. When the cash is gone, you stop spending in that category. This creates a hard spending limit.

How It Helps Save Money: Tracking expenses makes you more conscious of spending, reveals unnecessary subscriptions or purchases, and helps identify the biggest areas of potential savings. Awareness is the first step to changing spending behavior.

Think of expense tracking like a diet diary - you're more likely to eat healthier when you write down what you eat. Similarly, tracking expenses makes you more mindful of each purchase. The psychological effect is powerful: when you know you'll record a purchase, you're more likely to question whether it's necessary. This awareness alone can reduce spending by 10-15% without changing your budget at all.

Expense Tracking: Recording and monitoring all expenditures

Spending Awareness: Consciousness of money spent

Budget Categories: Groupings for different expense types

• Track expenses for at least one month

• Categorize expenses consistently

• Review regularly for patterns

• Track expenses immediately after purchase

• Use the 24-hour rule for non-essential purchases

• Set up alerts for budget limits

• Only tracking for a few days then stopping

• Not reviewing the tracked data

• Forgetting small purchases

Sarah has a monthly income of $4,000 and monthly expenses of $3,200. She wants to build a 6-month emergency fund. Calculate how long it will take her to build this fund if she saves her entire monthly surplus. If she wants to build the fund in 8 months instead, how much additional income or expense reduction would she need?

Current Situation:

Monthly surplus: $4,000 - $3,200 = $800

Emergency fund needed: $3,200 × 6 months = $19,200

Time to build fund: $19,200 ÷ $800 = 24 months

To Build Fund in 8 Months:

Required monthly savings: $19,200 ÷ 8 = $2,400

Additional monthly needed: $2,400 - $800 = $1,600

This could come from: $1,600 additional income, $1,600 expense reduction, or a combination.

Alternative Strategy: If Sarah can't immediately increase her surplus to $2,400, she could start with her current $800 and gradually increase it through side income or expense reductions over time.

This problem demonstrates the power of mathematical planning in finance. Emergency funds provide financial security, but building them quickly requires either significant surplus or accelerated strategies. The key insight is that reducing the time frame dramatically increases monthly requirements. This is why starting with whatever you can afford and gradually increasing contributions is often more sustainable than trying to make dramatic changes immediately.

Emergency Fund: Savings for unexpected expenses

Monthly Surplus: Income minus expensesFinancial Security: Buffer against unexpected events

• Emergency fund should cover 3-6 months of expenses

• Keep emergency fund in liquid accounts

• Don't invest emergency fund in volatile assets

• Start with a smaller emergency fund (1-2 months)

• Increase contributions gradually

• Use high-yield savings accounts

• Not having an emergency fund

• Investing emergency fund in risky assets

• Using emergency fund for non-emergencies

You currently spend $3,000/month on expenses with $4,000/month income. Your largest expenses are: Rent ($1,200), Dining Out ($400), Subscriptions ($200), Shopping ($300), and Other ($900). Design a strategy to increase your monthly savings by $500 through expense reduction. Which expenses would you target and by how much?

Current Situation:

Monthly income: $4,000

Monthly expenses: $3,000

Current savings: $1,000

Target savings: $1,500

Additional savings needed: $500

Strategy for $500 Additional Monthly Savings:

1. Dining Out Reduction ($150): Cut from $400 to $250 by cooking more meals at home and limiting restaurant visits to special occasions.

2. Subscription Audit ($100): Cancel unused subscriptions and reduce from $200 to $100 by keeping only essential services.

3. Shopping Reduction ($100): Cut from $300 to $200 by shopping with lists, avoiding impulse purchases, and buying generic brands.

4. Other Expenses ($150): Reduce miscellaneous spending from $900 to $750 by being more mindful of smaller purchases.

Result: New expenses: $2,500, New savings: $1,500 (37.5% savings rate)

This strategy maintains quality of life while significantly increasing savings.

This problem demonstrates the importance of targeting the largest expenses for maximum impact. Dining out and shopping are often the easiest categories to reduce without significantly impacting quality of life. The key is making sustainable changes that you can maintain long-term. Small changes in multiple categories are often more effective than drastic cuts in one area that you can't maintain.

Budget Optimization: Improving budget efficiency

Expense Categories: Groupings of similar expenses

Disposable Income: Income after essential expenses

• Focus on largest expense categories first

• Maintain quality of life while saving

• Make changes sustainable long-term

• Use the 50/30/20 rule as a baseline

• Set up automatic savings transfers

• Track progress weekly

• Cutting expenses too drastically to maintain

• Not accounting for occasional expenses

• Forgetting to adjust budget for life changes

Which of the following is the most effective strategy for generating fast additional income?

Taking on a part-time job or freelance work is the most effective strategy for generating fast additional income. This approach provides immediate, consistent income that can be directed toward savings. While selling unused items provides quick cash, it's a one-time opportunity. Starting a business takes time to generate income. Stock investing carries risk and may not provide immediate returns.

The answer is C) Taking on a part-time job or freelance work.

The key to fast savings is finding income streams that provide consistent, immediate returns. Part-time work and freelancing offer this because they convert your time directly into money, which can then be saved. The strategy works best when you can find work that utilizes your existing skills, minimizing the learning curve and maximizing your earning potential. This approach also builds valuable skills and professional networks.

Side Income: Additional earnings outside primary job

Freelancing: Independent contractor work

Part-time Work: Employment less than full-time hours

• Choose side work that doesn't exhaust you

• Direct additional income to savings immediately

• Consider tax implications of additional income

• Use skills you already have

• Consider gig economy opportunities

• Negotiate freelance rates upfront

• Taking on side work that affects primary job

• Spending additional income instead of saving

• Not accounting for taxes on additional income

FAQ

Q: How can I save money when I barely have enough to cover my expenses?

A: Even with tight budgets, small changes can make a difference:

Immediate Actions: Start by tracking where your money goes for one week. Often, small daily expenses add up significantly. Look for free alternatives to paid services (libraries instead of book purchases, free community events instead of expensive entertainment).

Micro-Savings: Save loose change, round up purchases to the nearest dollar, or commit to bringing lunch from home once a week.

Income Enhancement: Consider selling unused items, taking on small freelance tasks, or participating in the gig economy (food delivery, rideshare).

Remember, even $5-10 saved per week builds to hundreds over a year.

Q: What's the fastest way to build an emergency fund?

A: The fastest approach combines multiple strategies:

Immediate Steps: Sell unused items, cancel unnecessary subscriptions, and redirect all windfalls (tax refunds, bonuses, gifts) directly to savings.

Expense Reduction: Implement the 50/30/20 rule and aggressively cut the "wants" category while finding ways to reduce "needs" (negotiate bills, find cheaper housing options).

Income Enhancement: Take on part-time work, freelance, or participate in the gig economy. Consider higher-paying temporary positions.

Automation: Set up automatic transfers to a high-yield savings account to make saving effortless.

With aggressive implementation, you can build a 3-month emergency fund in 6-12 months instead of 2-3 years.