What is an Emergency Fund?

Complete emergency fund guide • Step-by-step explanations

Emergency Fund Fundamentals:

Show Emergency Fund CalculatorAn emergency fund is a savings account specifically set aside to cover unexpected expenses like medical bills, job loss, or urgent home repairs. It provides financial security and peace of mind by acting as a buffer against life's unpredictable events. The fund should be easily accessible and separate from other savings accounts.

Key emergency fund guidelines:

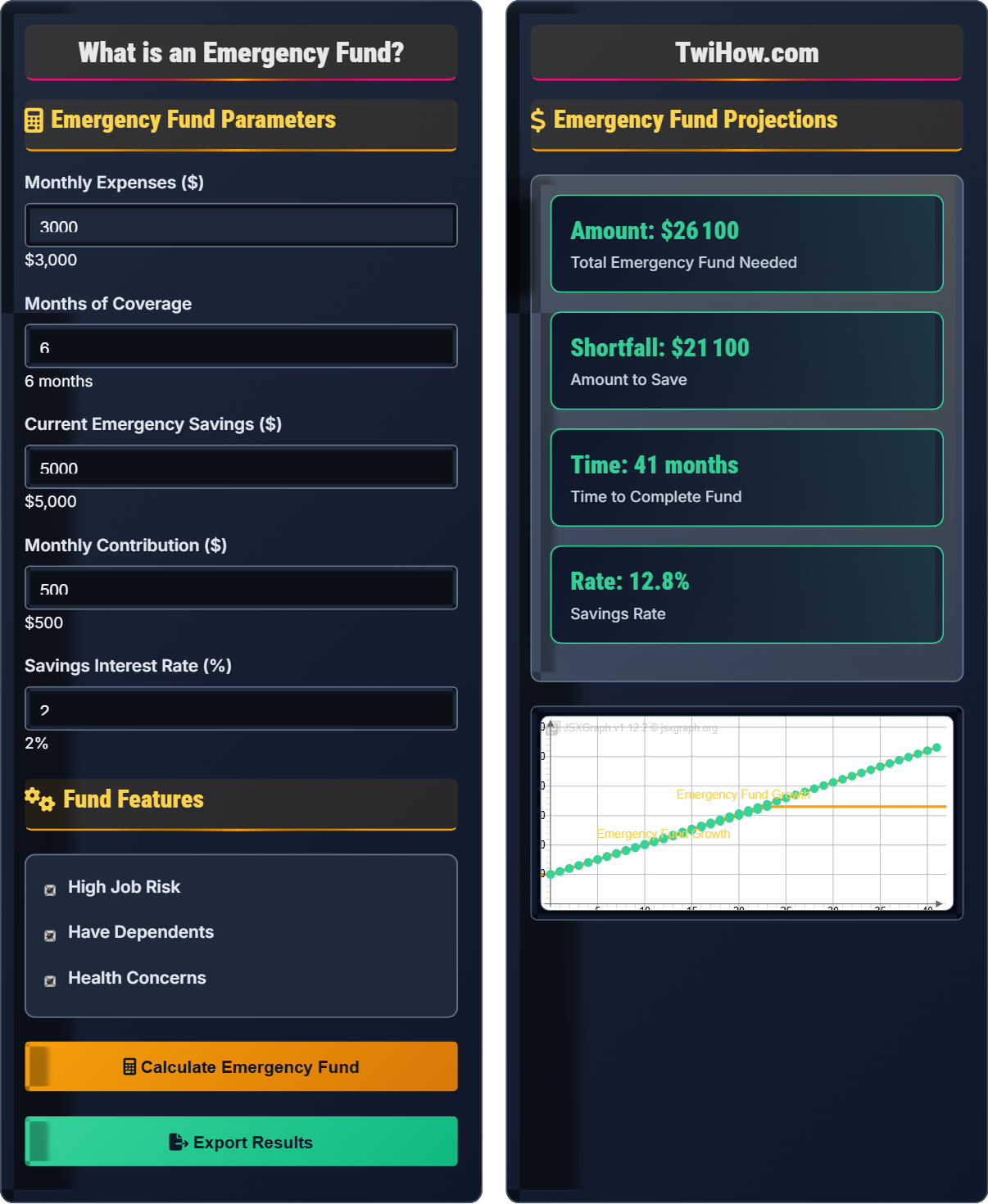

- Amount: 3-6 months of living expenses

- Accessibility: Liquid funds available within 24-48 hours

- Location: High-yield savings account or money market fund

- Usage: Reserved for genuine emergencies only

- Replenishment: Restore after use as soon as possible

Having an emergency fund prevents reliance on high-interest debt during financial hardships and provides stability during uncertain times.

Emergency Fund Parameters

Fund Features

Emergency Fund Projections

| Category | Monthly | 3-Month Fund | 6-Month Fund |

|---|---|---|---|

| Housing | $1,200 | $3,600 | $7,200 |

| Utilities | $300 | $900 | $1,800 |

| Food | $600 | $1,800 | $3,600 |

| Transportation | $400 | $1,200 | $2,400 |

| Insurance | $300 | $900 | $1,800 |

| Other | $200 | $600 | $1,200 |

Emergency Fund Fundamentals

An emergency fund is a dedicated savings account set aside to cover unexpected expenses that could otherwise disrupt your financial stability. It acts as a financial safety net for situations like job loss, medical emergencies, car repairs, or urgent home maintenance. The fund should be kept in a liquid, easily accessible account separate from other savings.

The basic formula for calculating your emergency fund target:

Where:

- Monthly Expenses: Total monthly living costs

- Months of Coverage: Typically 3-6 months

- Emergency Fund: Total amount needed for security

- Adjustment Factors: Job security, dependents, health

Calculate your emergency fund based on your personal circumstances:

Where Risk Multiplier is:

- 1.0 for stable employment

- 1.5 for moderate job insecurity

- 2.0 for high job risk or self-employment

- +0.5 for each dependent

- +0.5 for chronic health conditions

Use compound growth principles to build your emergency fund:

Where:

- A: Future value of fund

- P: Initial amount

- PMT: Monthly contributions

- r: Annual interest rate

- n: Compounding frequency

- t: Time in years

Proven approaches for building and maintaining your emergency fund:

- Start Small: Begin with $500-$1,000 and build gradually

- Use Windfalls: Deposit tax refunds, bonuses, and gifts

- Round-Up Method: Add spare change to savings

- Side Income: Direct additional income to emergency fund

- Automate: Set up automatic monthly transfers

- Separate Account: Keep fund separate from other savings

Emergency Fund Fundamentals

Emergency fund, financial security, liquid assets, risk management, financial planning, rainy day fund.

\(\text{Emergency Fund} = \text{Monthly Expenses} \times \text{Months of Coverage}\)

Where monthly expenses represent your essential living costs.

- Keep fund in easily accessible account

- Only use for genuine emergencies

- Rebuild immediately after use

Strategies

High-yield savings accounts, money market funds, automated transfers, expense tracking, windfall allocation.

- Automate monthly transfers

- Use tax refunds and bonuses

- Round up purchases

- Reduce unnecessary expenses

- Adjust fund size based on life circumstances

- Consider inflation in long-term planning

- Reassess periodically

Emergency Fund Learning Quiz

According to financial experts, what is the recommended amount for an emergency fund?

Financial experts recommend having 3-6 months of living expenses in an emergency fund. This provides a sufficient buffer to cover most unexpected situations like job loss, medical emergencies, or major repairs. The exact amount depends on your job security, family situation, and risk tolerance. Those with unstable employment or dependents should aim for the higher end of the range.

The answer is B) 3-6 months of expenses.

The 3-6 month rule is based on the average time it takes to find a new job after layoff, which is typically 3-6 months. It also covers the time needed to address major unexpected expenses. The range accounts for different risk profiles - someone with a stable government job might be fine with 3 months, while a freelancer should aim for 6 months. The key is having enough to weather most storms without resorting to high-interest debt.

Emergency Fund: Savings for unexpected expenses

Liquid Assets: Easily accessible funds

Living Expenses: Essential monthly costs

• Keep fund in easily accessible account

• Only use for genuine emergencies

• Rebuild after use

• Start with $1,000 minimum

• Automate monthly contributions

• Use high-yield savings account

• Keeping fund in low-interest checking account

• Using fund for non-emergencies

• Not replenishing after use

What types of expenses should an emergency fund cover? Give specific examples and explain why these situations require immediate access to cash.

Qualified Emergency Expenses:

1. Job Loss: Covers living expenses during unemployment period. Requires immediate access because income stops suddenly.

2. Medical Emergencies: Unexpected hospitalization, surgeries, or treatments not covered by insurance. Healthcare bills demand immediate payment.

3. Major Home Repairs: HVAC failure, roof damage, plumbing issues that affect livability. These repairs cannot wait for future budget cycles.

4. Vehicle Breakdowns: Critical repairs needed for transportation to work. Without reliable transport, you could lose income.

5. Family Crisis: Supporting dependents during their emergencies. Immediate financial support is often necessary.

Why Immediate Access is Critical: Emergency expenses typically require payment within days or weeks. Credit cards provide temporary relief but accrue interest. Loans take time to approve. Having liquid cash prevents compounding financial stress during already difficult situations.

The key distinction is between emergencies and planned expenses. Buying a new phone because you dropped your old one is not an emergency - it was planned. But if your only car breaks down and you need it to get to work, that's an emergency. The fund is specifically for situations where you have no choice but to spend money immediately to prevent greater financial hardship. This is why the fund must be liquid - you can't wait for investments to mature when your roof is leaking.

Genuine Emergency: Unforeseen event requiring immediate expense

Liquidity: Ease of converting to cash

Financial Hardship: Situation causing monetary stress

• Emergencies are unforeseen and unavoidable

• Must require immediate payment

• Should threaten financial stability if unpaid

• Keep a small portion in cash at home

• Maintain separate account from regular savings

• Set up automatic transfers

• Using fund for planned expenses

• Investing fund in volatile assets

• Not replacing used funds

John has monthly expenses of $4,000 and works in a volatile industry with frequent layoffs. He has two children and takes care of elderly parents. Calculate his emergency fund target using the standard 6-month recommendation and adjusting for his risk factors. If he currently has $8,000 saved, how long will it take to build his complete fund if he saves $800 per month?

Base Emergency Fund:

Monthly expenses: $4,000

Standard 6-month fund: $4,000 × 6 = $24,000

Risk Adjustments:

Job volatility: 6-month fund × 1.5 = $36,000

Two dependents: +$4,000 (2 × $2,000)

Supporting elderly parents: +$2,000

Total adjusted fund: $36,000 + $4,000 + $2,000 = $42,000

Time to Complete Fund:

Current savings: $8,000

Amount needed: $42,000 - $8,000 = $34,000

Monthly contribution: $800

Time needed: $34,000 ÷ $800 = 42.5 months ≈ 3.5 years

John should aim for a $42,000 emergency fund and will need approximately 3.5 years to build it at his current savings rate.

This problem demonstrates how personal circumstances affect emergency fund recommendations. The standard 3-6 month rule is just a starting point. People with dependents, unstable employment, or health issues need larger cushions. The key insight is that risk factors multiply the base amount rather than just adding a fixed amount. John's job instability alone increases his needs by 50% before considering other factors.

Risk Adjustment: Modification based on personal circumstances

Monthly Expenses: Recurring essential costs

Dependents: People relying on your income

• Adjust fund size for personal risk factors

• Consider all financial obligations

• Reassess as circumstances change

• Reassess annually or after major life changes

• Increase contributions when possible

• Consider multiple emergency scenarios

• Using one-size-fits-all approach

• Not considering all financial obligations

• Forgetting to adjust for life changes

Compare different options for storing an emergency fund: high-yield savings account, money market account, certificates of deposit (CDs), and investment accounts. Which is the best choice and why?

High-Yield Savings Account:

Pros: Highly liquid, FDIC insured, easy access, modest interest

Cons: Lower returns than investments

Money Market Account:

Pros: Higher interest than savings, still liquid, FDIC insured

Cons: May have transaction limits, minimum balance requirements

Certificates of Deposit (CDs):

Pros: Higher interest rates, FDIC insured

Cons: Penalties for early withdrawal, not immediately accessible

Investment Accounts:

Pros: Potential for higher returns

Cons: Volatile, not FDIC insured, not immediately accessible

Best Choice: High-yield savings account. It provides the perfect balance of accessibility, safety, and modest returns. The fund must be immediately available when needed, so liquidity is paramount. Investment accounts are inappropriate because they could lose value precisely when you need the money most.

The key principle is that emergency funds prioritize liquidity and safety over returns. This is counterintuitive to investment principles, but appropriate for this specific purpose. The goal is to preserve capital and provide immediate access, not to grow wealth. This is why the emergency fund is separate from investment accounts - they serve different purposes with different risk tolerances. The "safety" of investments during good times becomes "danger" during emergencies when you might need to sell at a loss.

Liquidity: Ease of converting to cash

FDIC Insurance: Government protection up to $250,000

Penalty: Fee for early withdrawal

• Prioritize liquidity over returns

• Keep fund separate from investments

• Ensure FDIC insurance coverage

• Compare APY rates among banks

• Look for accounts with no minimum balance

• Consider online banks for higher rates

• Investing emergency fund in volatile assets

• Using checking account with no interest

• Not considering FDIC limits

What should you do after using your emergency fund?

After using your emergency fund, you should immediately begin rebuilding it. The fund is meant to be a permanent financial safety net, not a one-time resource. Rebuilding should be prioritized as quickly as possible while maintaining other financial obligations. The fund needs to be restored to provide protection against future emergencies.

The answer is C) Rebuild the fund as soon as possible.

Many people think of their emergency fund as a "one-time use" resource, but it's actually a permanent part of your financial infrastructure. Just as you wouldn't remove your home's smoke detectors after a fire, you shouldn't leave yourself without an emergency fund after using it. The key is to rebuild gradually while maintaining other financial priorities. This might mean temporarily reducing other savings goals until the emergency fund is restored.

Financial Safety Net: Permanent protection against emergencies

Replenishment: Restoring fund to target amount

Permanent Protection: Ongoing financial security

• Emergency fund is permanent, not temporary

• Rebuild immediately after use

• Maintain fund as part of financial plan

• Set up automatic transfers for rebuilding

• Prioritize rebuilding in budget

• Consider temporary budget adjustments

• Thinking fund is disposable after use

• Not prioritizing replenishment

• Using fund as regular savings account

FAQ

Q: How do I start building an emergency fund when I have no money left after paying bills?

A: Even with tight budgets, you can start building an emergency fund:

Start Small: Begin with just $5-10 per week. Even small amounts build the saving habit.

Find Extra Money: Cancel unused subscriptions, sell items you don't need, or pick up occasional side work.

Automate: Set up automatic transfers to make saving effortless.

Emergency Fund First: Once you have $1,000, focus on other financial goals while continuing to build the fund.

Track Expenses: Identify areas where you can cut costs to free up money for savings.

The key is starting somewhere - even $25 per month builds to $300 per year.

Q: Should I build an emergency fund or pay off debt first?

A: The approach depends on your debt situation:

High-Interest Debt (10%+): Focus on paying down high-interest debt first, but maintain a small emergency fund of $1,000-$2,000 for true emergencies.

Low-Interest Debt (Under 6%): Build your emergency fund to 3-6 months of expenses first, then aggressively pay down debt.

Emergency Fund Benefits: Prevents going deeper into debt during unexpected expenses. Without an emergency fund, a $500 car repair could result in $1,000 in credit card debt.

Hybrid Approach: Build a small emergency fund while making minimum payments, then accelerate debt payoff while continuing to build the fund.