What is Passive Income?

Complete passive income guide • Step-by-step explanations

Passive Income Fundamentals:

Show Income CalculatorPassive income is money earned with minimal ongoing effort after initial setup. It allows you to generate revenue while sleeping, traveling, or focusing on other activities. The key is creating income streams that continue generating money with little to no daily involvement.

Key passive income methods:

- Dividend Stocks: Earnings from stock ownership

- Rental Properties: Income from real estate investments

- Digital Products: E-books, courses, software sales

- Peer-to-Peer Lending: Interest from lending to individuals

- Online Businesses: Affiliate marketing, advertising revenue

With proper planning and execution, passive income can provide financial freedom and security.

Income Parameters

Income Streams

Income Projections

| Year | Principal | Interest | Total Value |

|---|---|---|---|

| 1 | $10,000 | $700 | $10,700 |

| 2 | $10,000 | $1,449 | $11,449 |

| 3 | $10,000 | $2,250 | $12,250 |

| 4 | $10,000 | $3,108 | $13,108 |

| 5 | $10,000 | $4,026 | $14,026 |

What is Passive Income?

Passive income is money earned with minimal ongoing effort after initial setup. It allows you to generate revenue while sleeping, traveling, or focusing on other activities. The key is creating income streams that continue generating money with little to no daily involvement.

The most effective passive income methods include:

Where:

- Dividend Stocks: Earnings from stock ownership

- Rental Properties: Income from real estate investments

- Digital Products: E-books, courses, software sales

- Peer-to-Peer Lending: Interest from lending to individuals

- Online Businesses: Affiliate marketing, advertising revenue

Passive income grows through compound interest:

Where:

- A: Final amount

- P: Principal investment

- r: Annual interest rate

- n: Number of times compounded per year

- t: Time in years

Build passive income systematically:

- Assessment: Evaluate your financial situation and goals

- Research: Find profitable passive income opportunities

- Investment: Allocate funds to chosen methods

- Setup: Create systems for automatic income

- Monitoring: Track performance and optimize

- Reinvestment: Reinvest earnings for compounding effect

Success comes from consistent execution of this framework.

Key areas for passive income diversification:

- Multiple Investments: Don't rely on a single investment

- Different Asset Classes: Mix stocks, real estate, and digital

- Geographic Diversification: Spread across different markets

- Time Diversification: Vary investment timelines

- Rebalancing: Adjust allocations periodically

Passive Income Fundamentals

Compound interest, reinvestment, asset allocation, cash flow, dividend yield, rental yield.

\(A = P(1 + \frac{r}{n})^{nt}\)

Where A = final amount, P = principal, r = rate, n = compounding frequency, t = time.

- Start early to maximize compounding effect

- Reinvest earnings to accelerate growth

- Diversify investments to reduce risk

Strategies

Dividend stocks, rental properties, digital products, peer-to-peer lending, online businesses.

- Dividend investing

- Real estate investment

- Content creation

- Business ownership

- Initial investment requirements vary

- Time to generate income differs

- Risk levels differ significantly

Passive Income Learning Quiz

Which of the following is the BEST definition of passive income?

Passive income is money earned with minimal ongoing effort after initial setup. The key characteristic is that it continues to generate revenue with little to no daily involvement after the initial investment of time, money, or effort. This distinguishes it from active income, which requires continuous work.

The answer is B) Income earned with minimal ongoing effort after initial setup.

Think of passive income like planting a tree that bears fruit year after year. The initial work (planting, watering, nurturing) pays off as the tree continues to produce fruit with minimal ongoing care. Passive income follows the same principle - you make an initial investment (time, money, or effort) and then receive ongoing returns with minimal maintenance. This is different from active income where you trade time for money and stop earning when you stop working.

Passive Income: Earnings from minimal ongoing effort

Active Income: Earnings requiring ongoing work

Compounding: Earnings on previous earnings

• Initial effort is required for passive income

• Minimal ongoing effort after setup

• Income continues even when not working

• Start with skills you already possess

• Reinvest earnings to accelerate growth

• Diversify across multiple streams

• Expecting completely passive income without any effort

• Not understanding the initial setup requirements

• Confusing passive income with no income

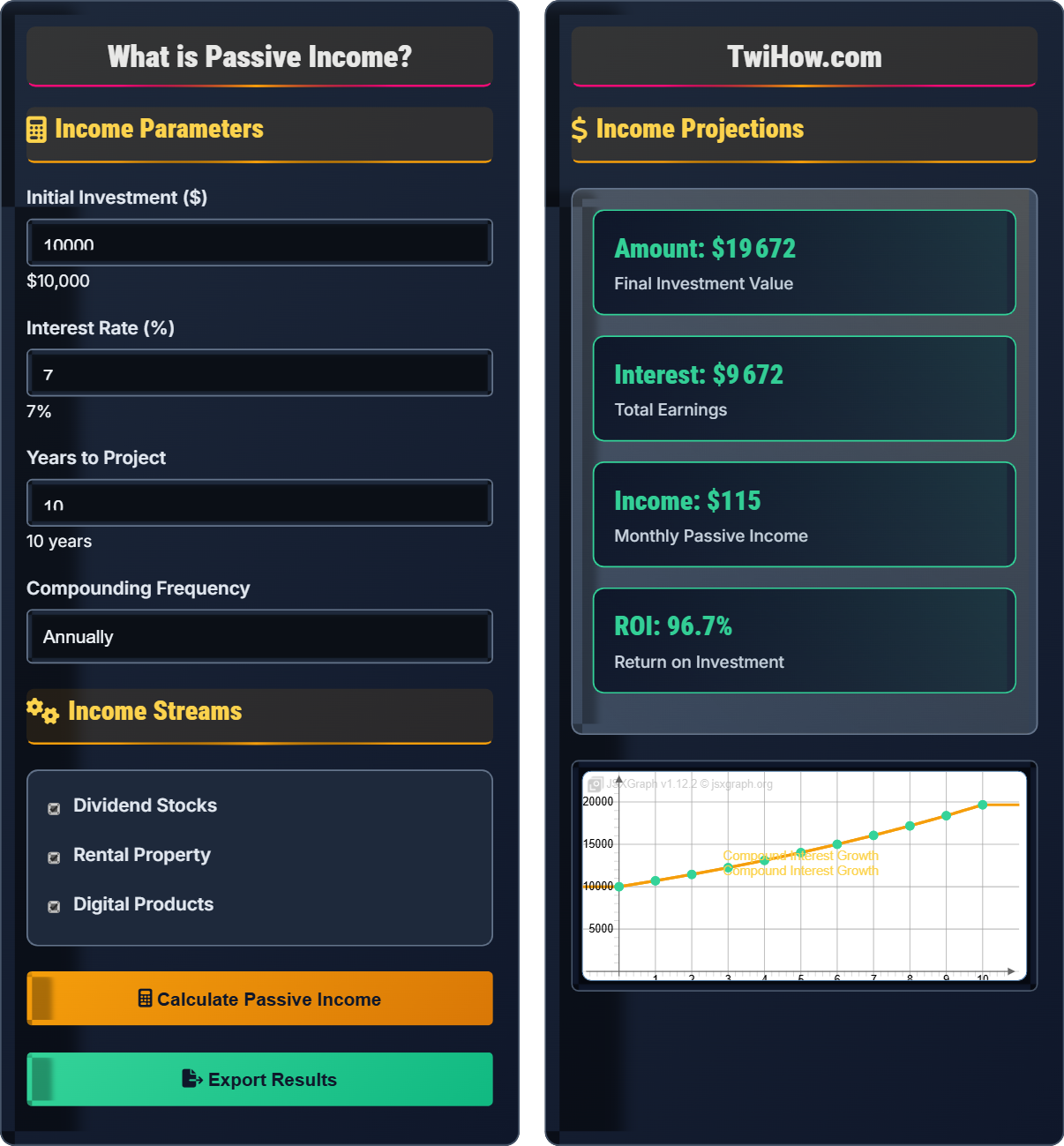

Explain the concept of compound interest and why it's crucial for building passive income. Calculate how much $10,000 invested at 7% annual interest would be worth after 10 years with annual compounding.

Compound Interest: Compound interest is interest calculated on the initial principal and also on the accumulated interest of previous periods. It's often called "interest on interest" and can cause wealth to grow exponentially over time.

Formula: A = P(1 + r/n)^(nt)

Calculation:

A = 10,000(1 + 0.07/1)^(1×10)

A = 10,000(1.07)^10

A = 10,000 × 1.967151

A = $19,671.51

Importance for Passive Income: Compound interest is the foundation of passive income growth. As your investments earn returns, those returns are reinvested and generate their own returns, creating a snowball effect. The longer the time horizon, the more dramatic the compounding effect becomes, making it crucial for building substantial passive income streams over time.

Compound interest works like a snowball rolling downhill - it starts small but grows larger and faster as it picks up more snow. In year 1, your $10,000 earns $700 in interest. In year 2, you earn interest not just on the original $10,000 but also on the $700 earned in year 1. This effect accelerates over time, which is why starting early is so important. The magic happens when your investment earnings start generating their own earnings, creating a self-reinforcing cycle of growth.

Compound Interest: Interest on principal plus previous interest

Principal: Initial amount invested

Time Value of Money: Money available now is worth more than later

• Time is the most important factor in compounding

• Even small differences in rate matter over time

• Reinvestment is essential for compounding

• Start investing as early as possible

• Maximize contribution to retirement accounts

• Minimize fees that reduce compounding

• Underestimating the power of time

• Not reinvesting dividends

• Paying unnecessary fees

Sarah purchases a rental property for $200,000. She rents it out for $1,500/month. Annual expenses (property taxes, insurance, maintenance, etc.) total $8,000. Calculate her annual cash flow and determine the cash-on-cash return on her investment. If she financed the purchase with a 20% down payment, what would her cash-on-cash return be?

Scenario 1: All Cash Purchase

Annual rental income: $1,500 × 12 = $18,000

Annual expenses: $8,000

Annual cash flow: $18,000 - $8,000 = $10,000

Cash-on-cash return: ($10,000 ÷ $200,000) × 100% = 5%

Scenario 2: Financed Purchase (20% down)

Down payment: $200,000 × 0.20 = $40,000

Loan amount: $200,000 - $40,000 = $160,000

Assuming mortgage payments of $10,000 annually (approximate)

Total annual expenses: $8,000 + $10,000 = $18,000

Annual cash flow: $18,000 - $18,000 = $0

Cash-on-cash return: ($0 ÷ $40,000) × 100% = 0%

Note: With a more conservative mortgage payment assumption of $8,000/year, the cash flow would be $2,000 and return would be 5%.

This problem demonstrates the impact of financing on investment returns. When using leverage (borrowed money), the return on your actual investment can be amplified, but it also increases risk. The key insight is that cash-on-cash return measures your return relative to the actual cash you invested, not the total property value. Financing allows you to control a larger asset with less cash, but you must account for all costs including mortgage payments.

Cash Flow: Income minus expenses

Cash-on-Cash Return: Annual cash flow divided by cash investedLeverage: Using borrowed money to increase investment

• Account for all expenses in calculations

• Consider vacancy rates and maintenance

• Leverage can amplify returns or losses

• Always budget for unexpected repairs

• Consider local rental market conditions

• Factor in property appreciation potential

• Forgetting to include all expenses

• Not accounting for vacancy periods

• Overestimating appreciation

You want to build a diversified passive income portfolio. Design a strategy that allocates $50,000 across different passive income methods. Include expected returns, risks, and time horizons for each investment. What would be your projected annual passive income?

Portfolio Allocation:

1. Dividend Stocks ($15,000 - 30%)

Expected Return: 3-4% dividend yield

Annual Income: $450-$600

Risks: Market volatility, dividend cuts

Time Horizon: 5+ years

2. REITs ($10,000 - 20%)

Expected Return: 4-6% yield

Annual Income: $400-$600

Risks: Interest rate sensitivity, market risk

Time Horizon: 3+ years

3. Peer-to-Peer Lending ($8,000 - 16%)

Expected Return: 6-8% after defaults

Annual Income: $480-$640

Risks: Default risk, platform risk

Time Horizon: 2+ years

4. Digital Product Creation ($7,000 - 14%)

Expected Return: Variable, $500-$1,000/month after setup

Annual Income: $6,000-$12,000

Risks: Market demand, competition

Time Horizon: 1-2 years to establish

5. High-Yield Savings ($10,000 - 20%)

Expected Return: 2-3%

Annual Income: $200-$300

Risks: Inflation risk

Time Horizon: Immediate

Projected Annual Income: $7,530-$14,140

Diversification is crucial for building a stable passive income portfolio. By spreading investments across different asset classes and methods, you reduce overall risk while maintaining growth potential. The key is balancing immediate income needs with long-term growth. Some investments provide immediate returns (savings accounts), while others require time to establish (digital products). The goal is to create a balanced portfolio that provides both stability and growth over time.

REIT: Real Estate Investment Trust

Diversification: Spreading investments across categories

Asset Allocation: Distribution of investments

• Diversify across asset classes

• Match investments to time horizons

• Balance risk and return

• Start with low-risk investments

• Gradually increase allocation to higher-risk options

• Regularly review and rebalance portfolio

• Concentrating all investments in one area

• Not considering liquidity needs

• Overlooking fees and taxes

Which of the following represents the most important principle for building sustainable passive income?

Diversifying across multiple income streams and asset classes is the most important principle for building sustainable passive income. This strategy reduces risk by not depending on a single source of income. If one stream underperforms or fails, others can continue generating income, providing stability and resilience to your overall financial picture.

The answer is B) Diversifying across multiple income streams and asset classes.

This principle is similar to not putting all your eggs in one basket. In the financial world, markets fluctuate, companies fail, and economic conditions change. By diversifying your passive income sources, you create a safety net that protects you from these uncertainties. For example, if you only rely on dividend stocks and the stock market crashes, your income would be severely impacted. But if you also have rental income, digital product sales, and savings interest, you'd maintain income stability.

Diversification: Spreading investments across different methods

Risk Management: Strategies to minimize potential losses

Income Stability: Consistent revenue over time

• Don't rely on a single income source

• Spread risk across multiple methods

• Balance risk and return appropriately

• Start with one method and gradually add others

• Track performance of each income stream

• Rebalance based on changing circumstances

• Concentrating all efforts in one area

• Not tracking income by source

• Ignoring correlation between investments

FAQ

Q: Is passive income really possible or is it just a myth?

A: Passive income is absolutely real and achievable! Millions of people worldwide earn passive income through various methods. The key is understanding that "passive" doesn't mean "effortless" - there's usually significant work upfront to set up the income stream, but once established, it requires minimal ongoing effort.

Examples of Real Passive Income: Dividends from stock ownership, rent from real estate, royalties from books or music, affiliate commissions from content, and interest from lending.

Success requires research, planning, and patience, but it's definitely possible to build substantial passive income over time.

Q: How much money do I need to start generating passive income?

A: The amount needed varies greatly depending on the method:

Low Cost Methods: Digital products ($100-500), affiliate marketing ($200-1,000), high-yield savings ($25-1,000)

Moderate Cost: Dividend investing ($1,000-10,000), P2P lending ($1,000-5,000)

High Cost: Rental properties ($50,000+), business investments ($10,000+)

You can start with as little as $25 in a high-yield savings account and gradually build up to larger investments. The key is starting somewhere and consistently adding to your investments over time.